ETF Tracker StatSheet

You can view the latest version here.

MARKETS RALLY ON DEBT DEAL PROGRESS, BUT BEWARE OF FED, INFLATION AND BANKING BUGS

[Chart courtesy of MarketWatch.com]

- Moving the markets

The markets were in a cheerful mood for the second day in a row, as hopes rose for a debt ceiling deal that would prevent a default. The S&P 500 recovered from its early-week slump and gained 0.4%.

McCarthy said that negotiators made some headway last night and were close to agreeing on a two-year debt limit increase, but he didn’t spill the beans on the details. The Debt Ceiling Fear-o-Meter dropped a few notches as a result.

{kind=link}

However, some analysts warned that the Fed might spoil the party by keeping its foot on the brake until the end of summer and then slamming on the gas next year with bigger rate cuts. Remember when they said inflation was just a passing phase?

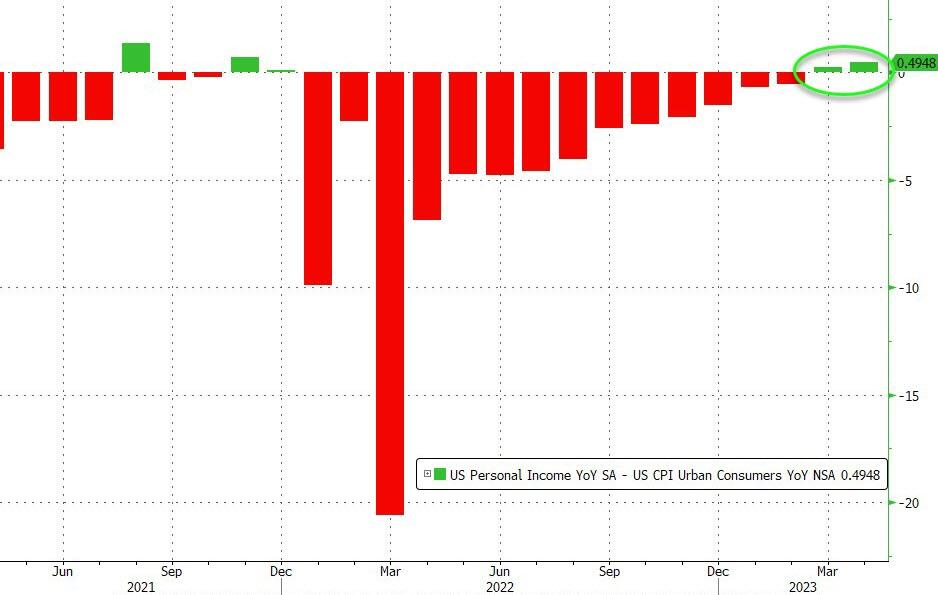

The Fed’s favorite inflation gauge, the PCE Deflator, didn’t help their case either. It came in hotter than expected and pushed the annual inflation rate higher. The only silver lining was that real income, adjusted for CPI, edged up slightly in April. But don’t get too excited, it might change later.

{kind=link}

{kind=link}

US economic data beat expectations this week, as ZeroHedge noted, probably because some inflation indicators showed signs of cooling off.

{kind=link}

The Nasdaq enjoyed the tech stock rally, especially Nvidia, and left Small Caps in the dust. It outperformed them by a factor of eight. The last time this happened, it didn’t end well.

{kind=link}

Regional banks bounced back earlier in the week but lost steam by the close, ahead of tonight’s crucial deposit data. This could reveal the next banking bug that needs to be squashed.

{kind=link}

Bond yields climbed higher today, after falling all week, and broke up with tech stocks. They used to move together, but now they’re going their separate ways. How long can this last?

{kind=link}

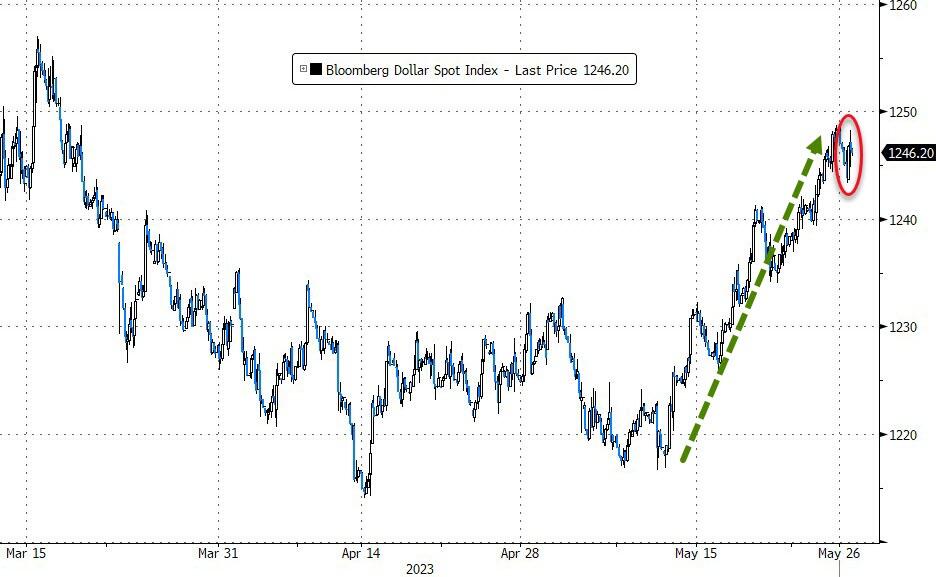

The US Dollar had a good week and rose for the third time in a row, but it faced some resistance towards the end. Gold had a bad week and dipped lower, but it managed to end on a positive note today.

{kind=link}

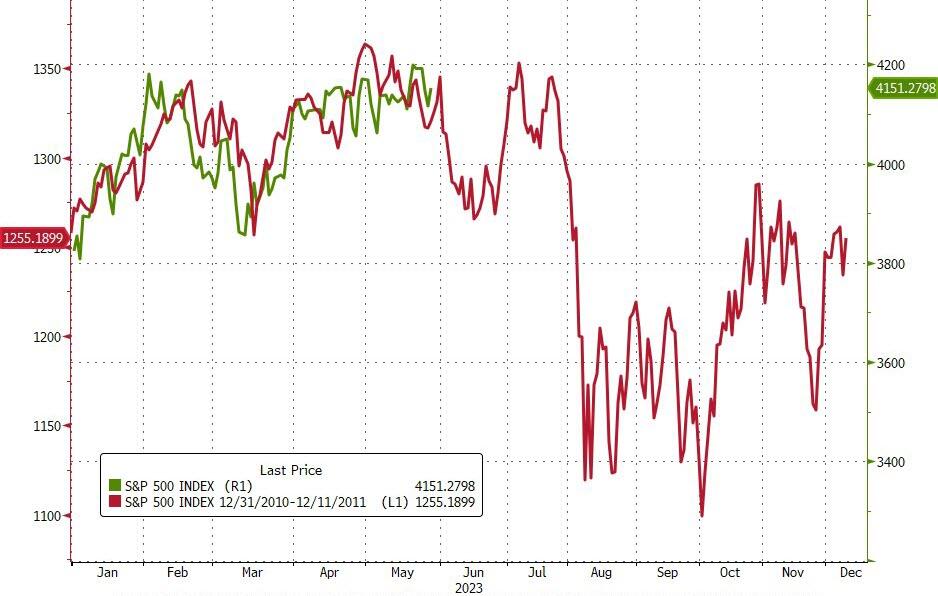

This reminds me of the summer of 2011, when a debt ceiling deal was hanging by a thread. Let’s hope history doesn’t repeat itself.

{kind=link}

- “Buy” Cycle Suggestions

For the current Buy cycle, which started on 12/1/2022, I suggested you reference my then current StatSheet for ETF selections. However, if you came on board later, you may want to look at the most recent version, which is published and posted every Thursday at 6:30 pm PST.

I also recommend you consider your risk tolerance when making your selections by dropping down more towards the middle of the M-Index rankings, should you tend to be more risk adverse. Likewise, a partial initial exposure to the markets, say 33% to start with, will reduce your risk in case of a sudden directional turnaround.

We are living in times of great uncertainty, with economic fundamentals steadily deteriorating, which will eventually affect earnings negatively and, by association, stock prices.

In my advisor’s practice, we are therefore looking for limited exposure in value, some growth and dividend ETFs. Of course, gold has been a core holding for a long time.

With all investments, I recommend the use of a trailing sell stop in the range of 8-12% to limit your downside risk.

- Trend Tracking Indexes (TTIs)

Our TTIs improved, as hope for a debt ceiling deal ignited bullish spirits. However, it was not enough firepower to propel the Domestic TTI back above its trendline. This simply means we are still stuck in the neutral zone, as the comeback rally was narrow based with most stocks not participating.

This is how we closed 05/26/2023:

Domestic TTI: -0.44% below its M/A (prior close -1.28%)—Buy signal effective 12/1/2022.

International TTI: +4.29% above its M/A (prior close +3.59%)—Buy signal effective 12/1/2022.

All linked charts above are courtesy of Bloomberg via ZeroHedge.

———————————————————-

WOULD YOU LIKE TO HAVE YOUR INVESTMENTS PROFESSIONALLY MANAGED?

Do you have the time to follow our investment plans yourself? If you are a busy professional who would like to have his portfolio managed using our methodology, please contact me directly to get more details.

Contact Ulli