- Moving the markets

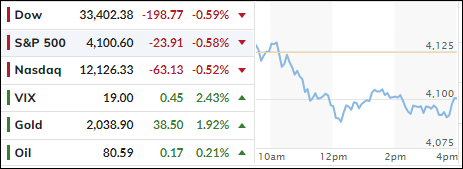

The markets pulled back right after the opening, in part due to uncertainty about yesterday’s spike in oil prices and how it might affect the global economic environment.

Not helping matters were a host of econ data showing that a slowdown had indeed arrived, as the Labor market appears to have fractured with job openings and new hires showing deteriorating numbers; their lowest since May 2021.

{kind=link}

{kind=link}

At the same time, US Factory Orders slipped to 2.7%, a number we have not seen since February 2021. The Citi economic Surprise Index shifted into reverse and, at least for the moment, the adage “bad news is good news” bit the dust.

{kind=link}

{kind=link}

Apparently, similar weakness was also found in other countries’ s backyards, as the Central Bank of Australia joined the Canadian one in “pausing” on rate hikes.

Hmm, does that mean the Fed will follow suit?

While that is not clear yet, the fallout made itself felt across a variety of markets. The major indexes only corrected moderately, as “most shorted” stocks collapsed. In other words, the squeeze play had run out of ammunition.

{kind=link}

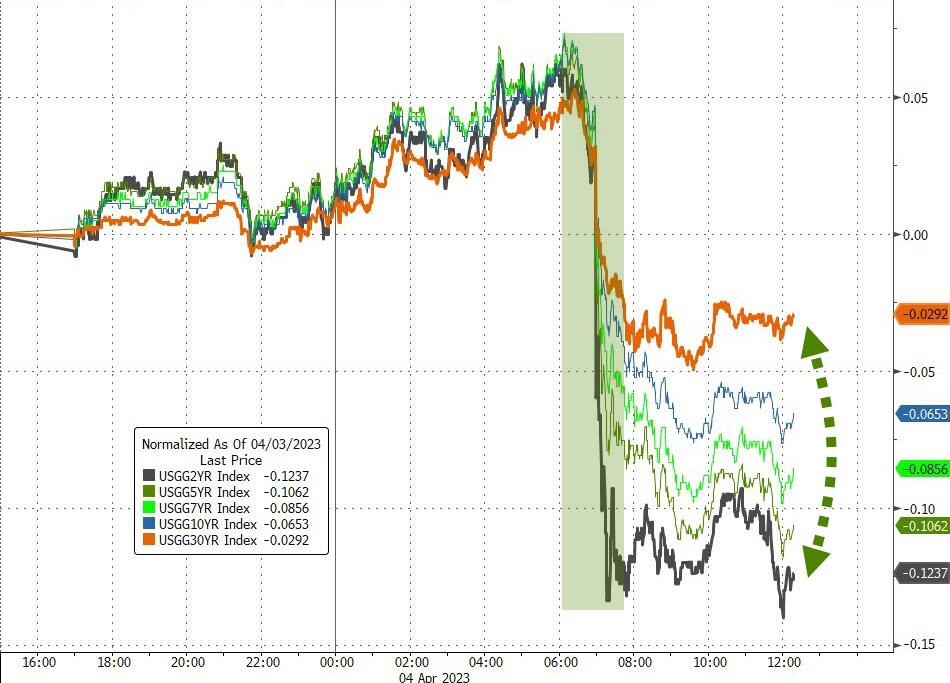

With these overwhelming weak data points, it came as no surprise that bond yields tumbled, as the 2-year “lost” its 4% level. The US Dollar succumbed to dovish news and pulled back to its 2-month lows.

{kind=link}

{kind=link}

{kind=link}

Benefiting from this unsure environment was Gold, as the precious metal stormed higher by almost 2% and closed solidly above its much fought-over $2k level at $2,039.

{kind=link}

Right now, we are witnessing the worst of both worlds, namely higher inflation, due to a reduction in oil production, while a deteriorating economy warrants a bailout via lower interest rates.

That makes me ponder: Will the Fed continue its hawkish policy to save the dollar, or will they fold by pausing or lowering rates to save the economy?

Hmm…

2. “Buy” Cycle Suggestions

For the current Buy cycle, which started on 12/1/2022, I suggested you reference my then current StatSheet for ETF selections. However, if you came on board later, you may want to look at the most recent version, which is published and posted every Thursday at 6:30 pm PST.

I also recommend you consider your risk tolerance when making your selections by dropping down more towards the middle of the M-Index rankings, should you tend to be more risk adverse. Likewise, a partial initial exposure to the markets, say 33% to start with, will reduce your risk in case of a sudden directional turnaround.

We are living in times of great uncertainty, with economic fundamentals steadily deteriorating, which will eventually affect earnings negatively and, by association, stock prices.

In my advisor’s practice, we are therefore looking for limited exposure in value, some growth and dividend ETFs. Of course, gold has been a core holding for a long time.

With all investments, I recommend the use of a trailing sell stop in the range of 8-12% to limit your downside risk.

3. Trend Tracking Indexes (TTIs)

Our TTIs pulled back but remain in bullish territory with the International one still showing better upside momentum.

This is how we closed 04/04/2023:

Domestic TTI: +1.33% above its M/A (prior close +2.35%)—Buy signal effective 12/1/2022.

International TTI: +7.60% above its M/A (prior close +7.77%)—Buy signal effective 12/1/2022.

All linked charts above are courtesy of Bloomberg via ZeroHedge.

Contact Ulli