- Moving the markets

Even though the Fed did exactly what was expected, namely hiking rates by only 0.25% to the 4.75%-5% target range and confirmed that Quantitative Tightening (QY) will continue as had been assumed, the markets reacted violently.

Trying to spew some words of reassurance, Powell added:

The U.S. banking system is sound and resilient. Recent developments are likely to result in tighter credit conditions for households and businesses and to weigh on economic activity, hiring, and inflation. The extent of these effects is uncertain.

Yet, he also added a hint of hawkishness by changing his reference about inflation from “has eased somewhat” to “remains elevated.” And “rate cuts are not in our base case.”

With traders dissecting his every word, uncertainty reigned after the release with the markets at first aimlessly bobbing and weaving, as the S&P chart above shows. However, in the end, chaos set in with traders and algos pushing the “sell” buttons and sending the major indexes plummeting into the close.

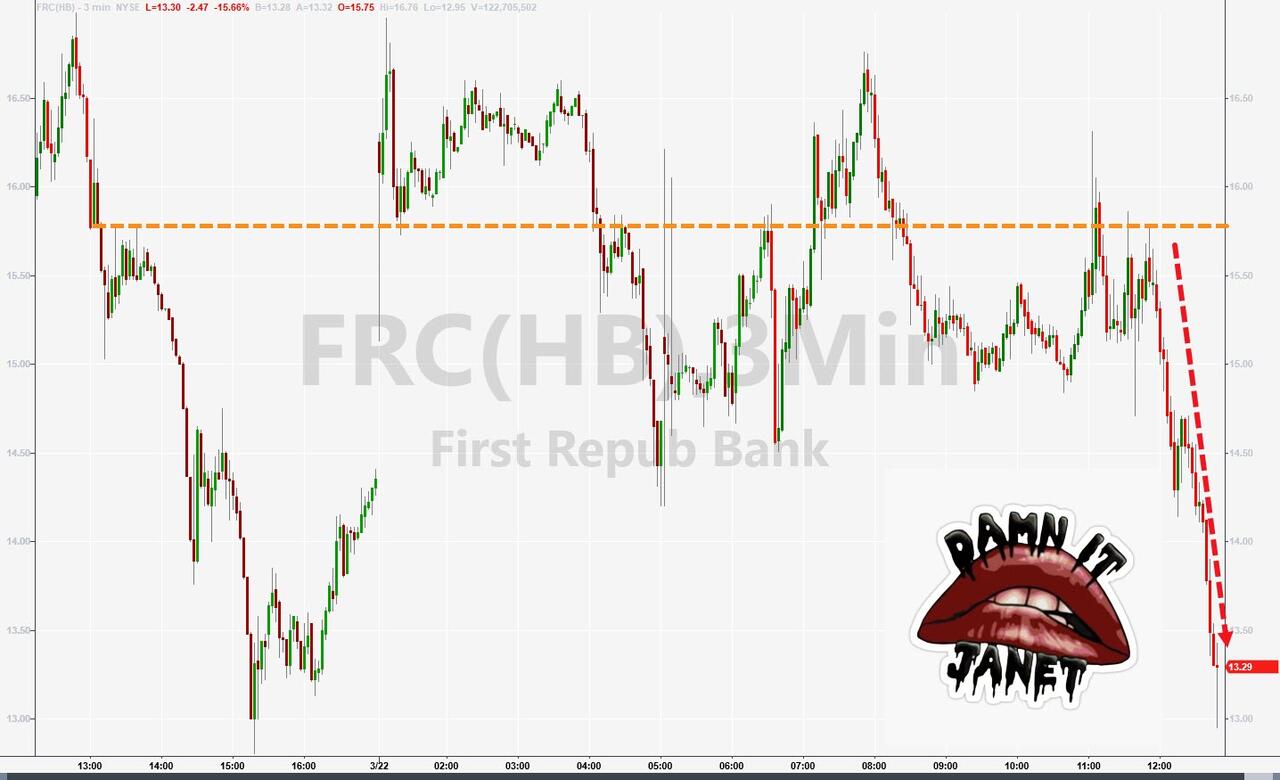

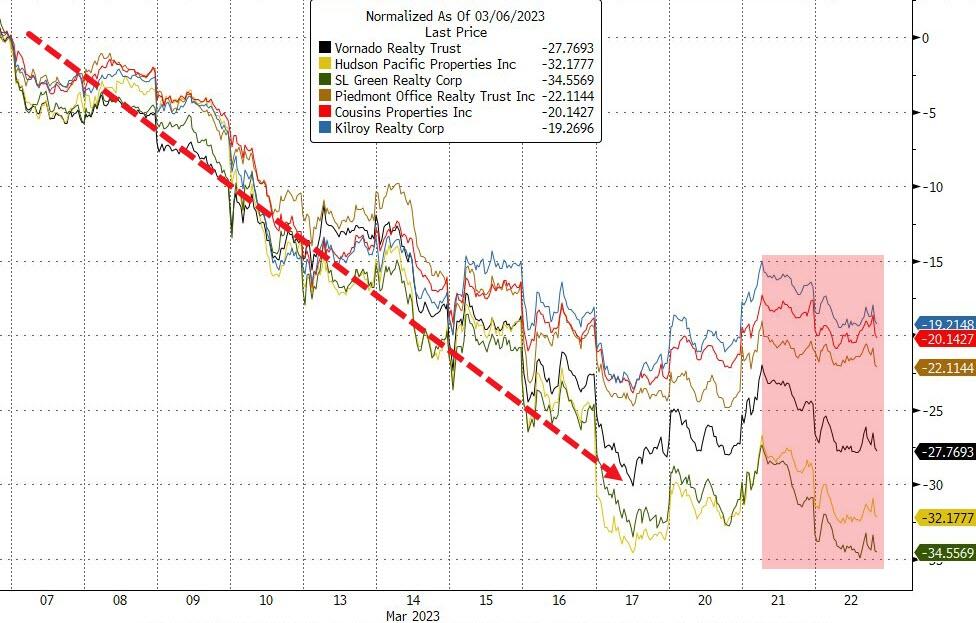

Regional banks took a hit, as ZeroHedge pointed out, with First Republic Bank getting hammered, while REITS lost their recent upward momentum again.

{kind=link}

{kind=link}

{kind=link}

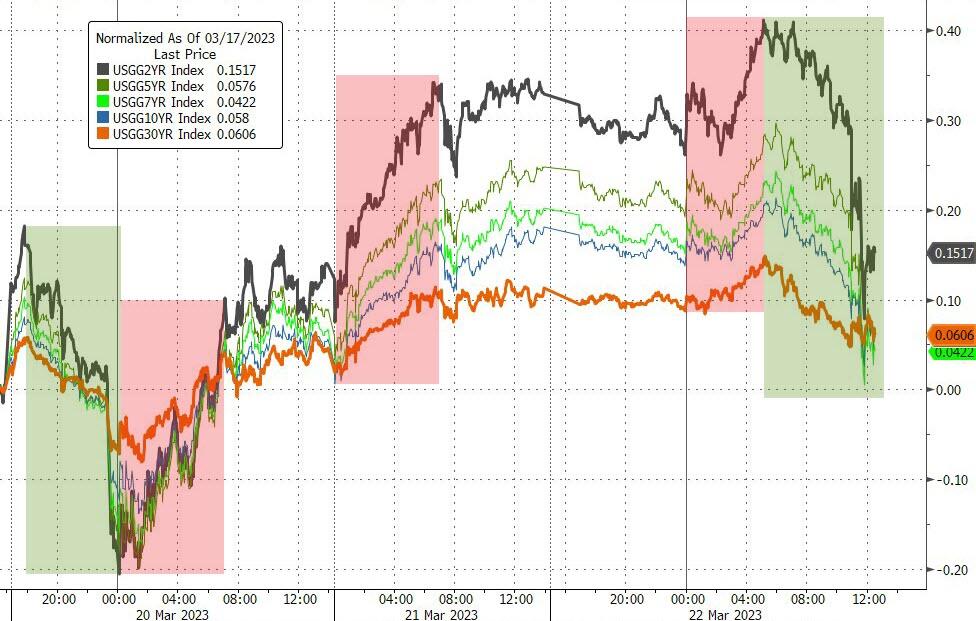

Bond yields dropped, after an early rise, with the 2-year thriving and then diving back below its 4% level. The US Dollar dumped to 6-week lows, which gave Gold the opportunity to shine, and the precious metal delivered by rallying +1.82%.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Will the bulls grab the baton tomorrow and view this sell off as a buying opportunity, or will the bears rule? We’ll find out over the next few days.

2. “Buy” Cycle Suggestions

For the current Buy cycle, which started on 12/1/2022, I suggested you reference my then current StatSheet for ETF selections. However, if you came on board later, you may want to look at the most recent version, which is published and posted every Thursday at 6:30 pm PST.

I also recommend for you to consider your risk tolerance when making your selections by dropping down more towards the middle of the M-Index rankings, should you tend to be more risk adverse. Likewise, a partial initial exposure to the markets, say 33% to start with, will reduce your risk in case of a sudden directional turnaround.

We are living in times of great uncertainty, with economic fundamentals steadily deteriorating, which will eventually affect earnings negatively and, by association, stock prices. I can see this current Buy signal to be short lived, say to the end of the year, and would not be surprised if it ends at some point in January.

In my advisor practice, we are therefore looking for limited exposure in value, some growth and dividend ETFs. Of course, gold has been a core holding for a long time.

With all investments, I recommend the use of a trailing sell stop in the range of 8-12% to limit your downside risk.

3. Trend Tracking Indexes (TTIs)

Our TTIs sold off with the International one showing more resilience. If more bearish momentum materializes, we will see our Domestic TTI move into “Sell” mode.

This is how we closed 03/22/2023:

Domestic TTI: -2.81% below its M/A (prior close -0.57%)—Buy signal effective 12/1/2022.

International TTI: +3.95% above its M/A (prior close +4.13%)—Buy signal effective 12/1/2022.

All linked charts above are courtesy of Bloomberg via ZeroHedge.

Contact Ulli