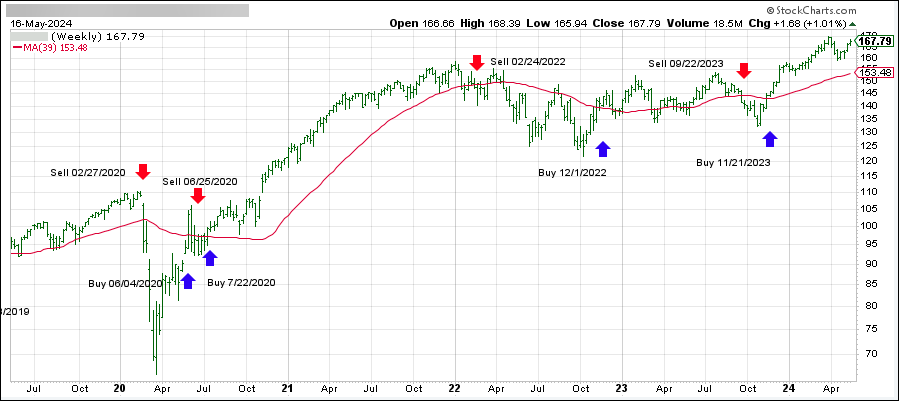

ETF Tracker StatSheet

You can view the latest version here.

FED’S DILEMMA: CAUGHT BETWEEN ROCK AND HARD PLACE

- Moving the markets

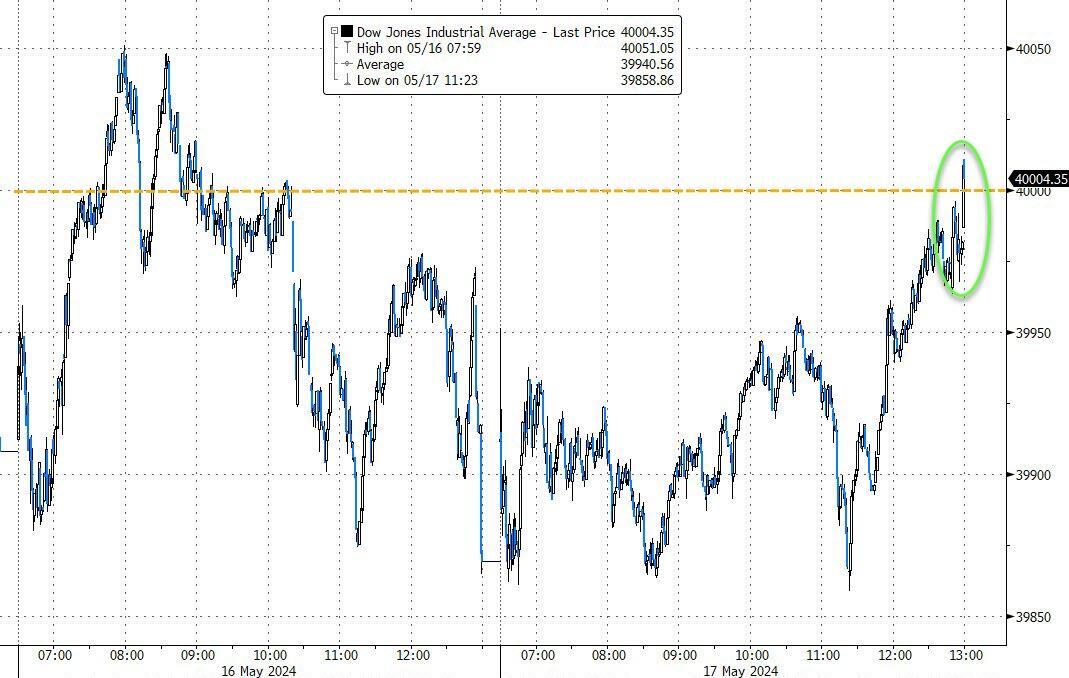

The Dow meandered near the flat line today, after the index briefly topped the key 40,000 level for the first time in the previous session. A last hour drive by the algos pushed 2 of the 3 majors back into the green to end Thursday’s run on a positive note, with the Dow closing above 40k for the first time.

This week’s rally has helped thrust the three indexes into positive territory for the second quarter despite a sluggish start. The S&P 500 and Nasdaq are now each up more than 11% in 2024, while the Dow has climbed more than 5% on the year. Yet, gold remains the top performer with a gain of almost 17%.

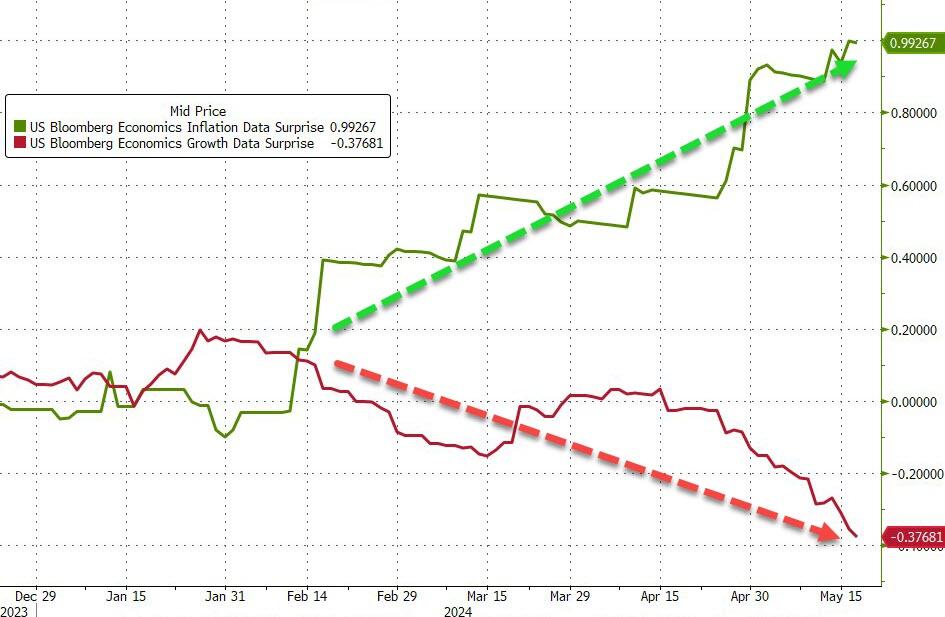

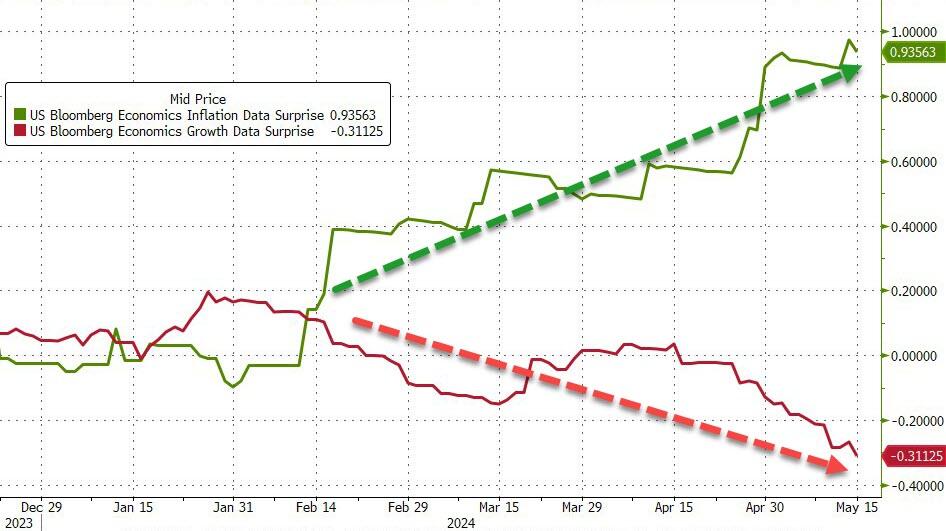

Traders still insist that positive economic growth and weakening inflation will continue to be the driver for higher prices, but reality is that we have moved into a stagflation environment, with accelerating inflation and slower growth now being the dominant forces.

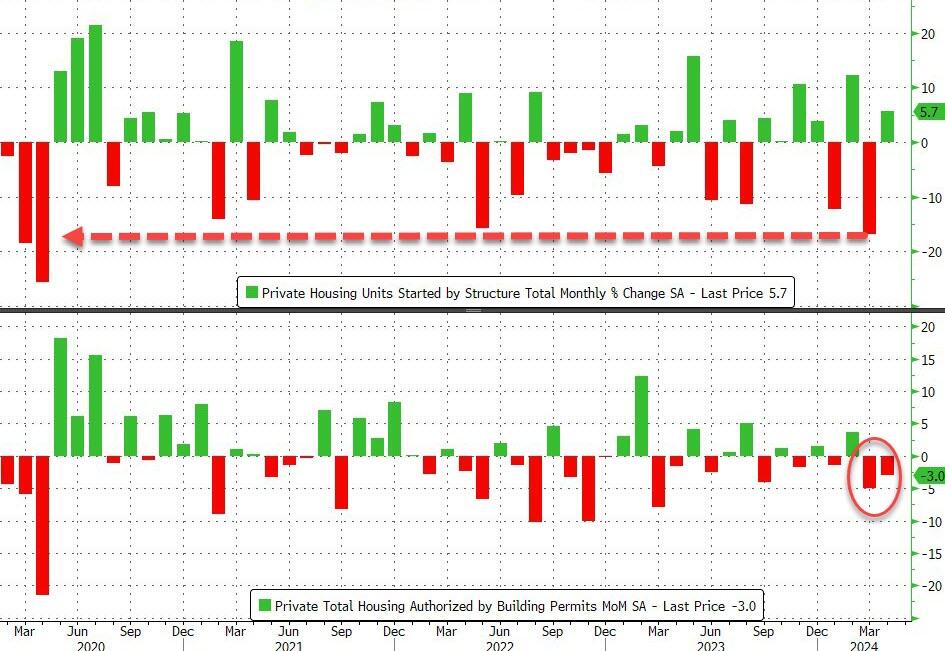

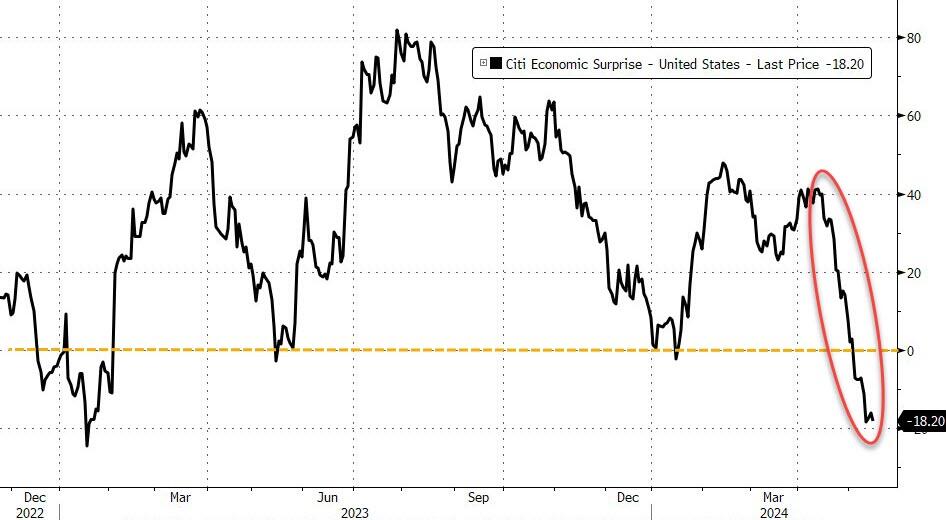

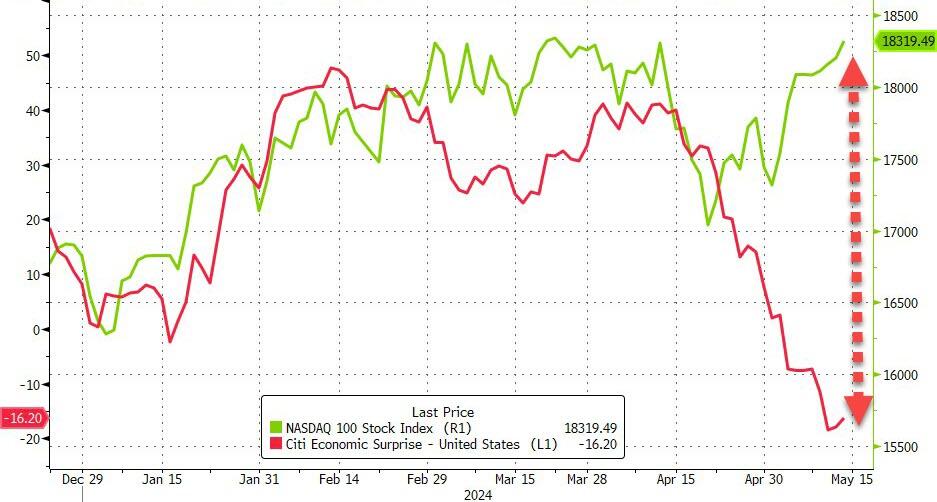

The US Macro Surprise index declined for the sixth straight week to its weakest since January 2023, as Zero Hedge pointed out. While that is bad news, Wall Street considers it good news, as risky stocks have risen in the face of a slowing economic environment, with the spread increasing almost daily. Go figure…

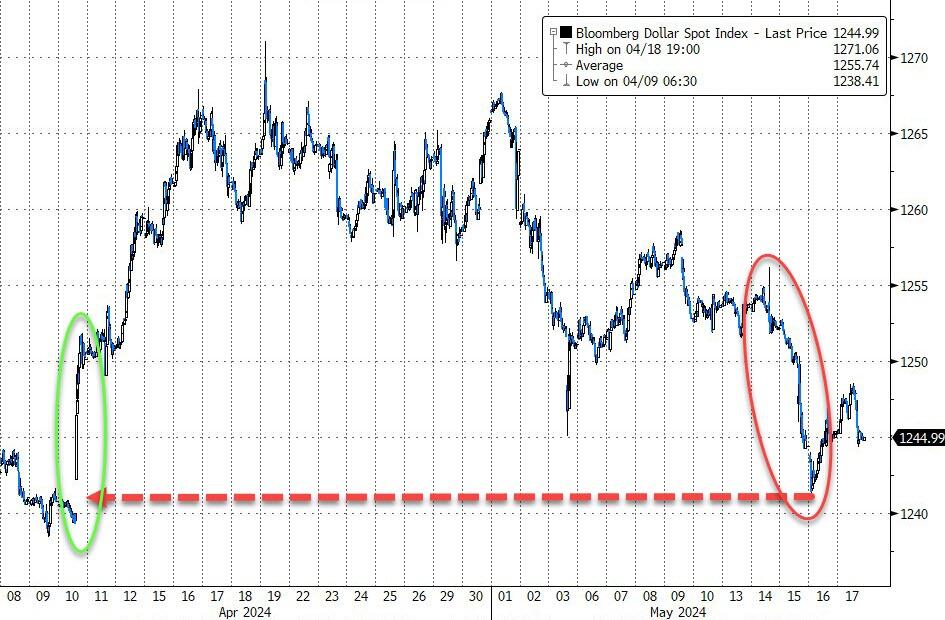

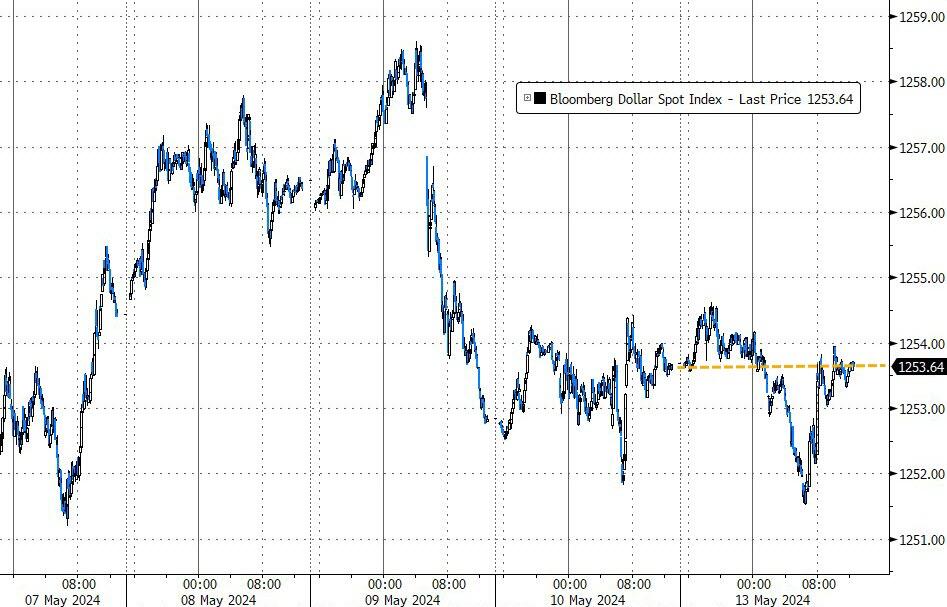

Monday’s short squeeze faded as the week went on, Bond yields slipped despite increasing rates over the past couple of days, and the dollar lost momentum. Gold surged to a new record closing high.

Bitcoin had a big week and raced back above its $67k level, and even oil prices jumped and nibbled at the $80 resistance level. Silver dramatically outperformed gold, as it topped its $30 price for the first time in many years.

And again, as traders are hanging on to the dream of lower rates, this chart makes it very clear that inflation remains a serious threat, and if it is to be conquered, interest rates need to move higher and not lower.

I think the Fed now realizes what it means to be caught between a rock and a hard place.

Read More

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}