ETF/No Load Fund Tracker Newsletter For Friday, April 26, 2013

ETF/No Load Fund Tracker StatSheet

————————————————————-

THE LINK TO OUR CURRENT ETF/MUTUAL FUND STATSHEET IS:

https://theetfbully.com/2013/04/weekly-statsheet-for-the-etfno-load-fund-tracker-newsletter-updated-through-04252013/

————————————————————

Market Commentary

Friday, April 26, 2013

UNINSPIRING GDP GROWTH DRAGS DOWN THE BULL

The major averages entered the weekend on a mixed note following a lackluster result on 1Q US GDP growth and a slew of below average earnings releases. The Standard & Poor’s 500 Index ended its winning streak today slipped 3 points (0.2%) to 1,582. The Nasdaq Composite dropped 11 points (0.3%) to 3,279. The Dow Jones Industrial Average in the other hand closed higher by 13 points at 14,713 thanks to Chevron and Boeing. Volume dropped off sharply on both major exchanges in the stock market today compared to Thursday’s pace.

Real GDP rose at a 2.5% annual rate in Q1, below the consensus estimate of 3.2%. The increase was driven by strong personal consumption expenditures (PCE) and inventory rebuilding, but was weighed down by negative net exports, reduced government spending, and a sharp deceleration in nonresidential fixed investment. Housing construction continues to strengthen and is expected to continue to contribute to GDP growth in the coming quarters.

Imports rebounded at a 5.4% annual rate, the most since Q3 2010, while exports rose 2.9%. As a result, net trade subtracted 0.50 percentage points from growth. The government sector fell at a 4.1% annual rate, subtracting 0.80 percentage points from growth. With the sequester taking impact in March, the drag is expected to increase going forward.

Additionally, according to Bloomberg, the gain in consumer spending is viewed as unsustainable, as disposable income adjusted for inflation fell at a 5.3% annualized rate in Q1. With consumer spending accounting for roughly 70% of GDP, this figure really raises concerns. Following the GDP release, treasuries appreciated despite the upward revision to domestic consumer sentiment.

In earnings news, Amazon.com and Dow member Chevron Corp posted mixed 1Q results and Starbucks matched analysts’ expectations, while the housing recovery lifted profits at homebuilder D.R. Horton.

Of the 271 companies in the S&P 500 that have reported earnings to date for the first quarter, 69 percent have beaten sharply reduced analyst expectations – above the 63 percent average since 1994 and slightly over the 67 percent beat rate over the past four quarters.

For the week, the Dow gained 1.1 percent, the S&P 500 added 1.7 percent and the Nasdaq rose 2.3 percent. Another week with mixed economic results – disappointing existing homes sales were met with stronger-than-expected new home sales, jobless claims fell more than expected while durable goods orders missed forecasts.

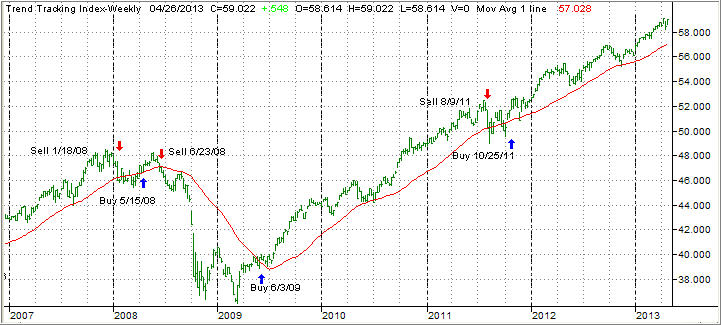

However, stocks managed to end higher thanks to the never ending fact that bad news is good news, as it assures continued money printing by the Fed even as fiscal policy continues to weigh on businesses. Economic growth in Q2 is expected to suffer due to fiscal tightening, before hopefully regaining traction later this year. How will the market be affected? Since we don’t know how things will play out, we will follow the major trends as represented by my Trend Tracking Indexes (TTIs).

Both rallied sharply this week, which means the bull is alive and well.

Here’s how we closed these out the last five trading days:

Domestic TTI: +3.52% (last week +2.80%)

International TTI: +7.35% (last week +5.54%)

Have a great week.

Ulli…

————————————————————-

READER Q & A FOR THE WEEK

All Reader Q & A’s are listed at our web site!

Check it out at:

http://www.successful-investment.com/q&a.php

A note from reader Ed:

Q: Ulli: What are your thoughts on the PRPFX Fund with gold having dropped so fast??

A: Ed: I don’t own it, since it is hovering below its long-term trend line. There are far better opportunities in low volatility ETFs.

———————————————————-

WOULD YOU LIKE TO HAVE YOUR INVESTMENTS PROFESSIONALLY MANAGED?

Do you have the time to follow our investment plans yourself? If you are a busy professional who would like to have his portfolio managed using our methodology, please contact me directly or get more details at:

https://theetfbully.com/personal-investment-management/

———————————————————

Back issues of the ETF/No Load Fund Tracker are available on the web at:

https://theetfbully.com/newsletter-archives/

The latest inflation number has been quite low at an annual pace of 1.2 percent, but it’s a lagging indicator and will probably keep the Fed on hold for longer, meaning bond proxies and income orientation that has worked well thus far will continue to do so in future, said David Rosenberg, chief economist and strategist at Gluskin Sheff & Associates.

The latest inflation number has been quite low at an annual pace of 1.2 percent, but it’s a lagging indicator and will probably keep the Fed on hold for longer, meaning bond proxies and income orientation that has worked well thus far will continue to do so in future, said David Rosenberg, chief economist and strategist at Gluskin Sheff & Associates.