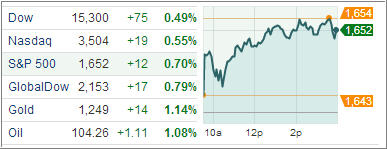

U.S. equity indexes ended this volatile session on a mixed note, after the release of the minutes from the Federal Reserve’s June policy meeting created uncertainty over when and if the central bank will start to trim the stimulus.

Attention shifted to focus on the speech by Chairman Ben Bernanke to begin after the closing bell. The Chairman says the U.S. economy still needs help from the Fed’ low interest rate policies, and because unemployment remains high and inflation is below the Fed’s target, the policies are still necessary. However, just like the Fed’s minutes, Bernanke failed to signal any changes in the bond-buying program during his remarks.

On the markets, energy and financials displayed weakness throughout the day before settling near their lows. The energy sector shed 0.6% despite the continued rise in crude oil, which added 2.4% to $106.04 per barrel. The energy component has rallied steadily since late June, and reports of a well leak off the coast of Louisiana contributed to today’s strength.