ETF/No Load Fund Tracker Newsletter For Friday, July 26, 2013

ETF/No Load Fund Tracker StatSheet

————————————————————-

THE LINK TO OUR CURRENT ETF/MUTUAL FUND STATSHEET IS:

https://theetfbully.com/2013/07/weekly-statsheet-for-the-etfno-load-fund-tracker-newsletter-updated-through-07252013/

————————————————————

Market Commentary

Friday, July 26, 2013

DOWN EARLY, BUT UP LATE

Despite starting the day sharply lower, the U.S. equity markets eked out gains to close the Friday session marginally higher. Stocks started the day to the downside in the wake of a 3% decline in the Japanese equity sell-off, as did a series of mixed earnings reports that featured notable misses from Amazon.com and Expedia.

Major averages hit their lows shortly after a headline crossed saying the IMF felt the interest rate volatility in the U.S. could have an adverse global effect and that economic risks remain tilted to the downside. The Dow Jones Industrial Average closed 3 points higher at 15,559, the S&P 500 Index gained 1 point (0.1%) to 1,692, and the Nasdaq Composite added 8 points (0.2%) to 3,613.

In economic news, consumer confidence unexpectedly increased in July to the highest level in six years as Americans’ views of their finances improved, according to the Thomson Reuters/University of Michigan final index of U.S. consumer sentiment. The measure advanced 1.2 points from mid-month to 85.1 in July; economists expected a slight uptick to 84.1. The improvement suggests stronger GDP growth in 2H while inflation expectations eased slightly.

Overseas, consumer prices in Japan excluding food rose 0.4 percent in June, more than economists estimated and the biggest jump since 2008, damping speculation the country will need to expand stimulus. In China, the government directed more than 1,400 companies in industries from steelmaking to papermaking to cut excess capacity by year-end.

In earnings news, Amazon.com reported a 2Q net loss of $0.02 per share, compared to the $0.05 per share profit that analysts had expected, as revenues rose 22% year-over-year (y/y) to $15.7 billion, roughly in line with the Street’s forecasts.

Elsewhere, Expedia recorded 2Q EPS ex-items of $0.64, well below the $0.79 that the Street was projecting, as revenues rose 16% y/y to $1.2 billion, compared to the $1.3 billion that analysts had expected.

The recovery off the lows wasn’t necessarily fueled by a single sector that was undeniably strong. Five of the 10 S&P 500 industry sector indexes advanced, with the health sector (+0.7%) leading the gains while the materials sector (-0.4%) brought up the rear. With just three trading days left in the month, the S&P 500 is set to post its best month since October 2011. The Nasdaq’s advance makes July so far the best month in a year and a half.

For the week, the S&P 500 finished essentially flat – down just 0.03 pct – the first week in five that it did not manage a gain. But the benchmark index is up 5.3 percent so far in July. The Dow rose 0.1 percent for the week, extending its string of weekly gains.

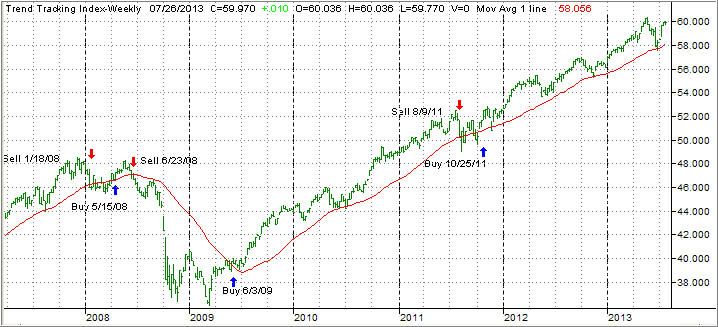

Our Trend Tracking Indexes (TTIs) closed the week as follows:

Domestic TTI: +3.32% (last week +3.47%)

International TTI: +6.66% (last week +6.76%)

Have a great week.

Ulli…

————————————————————-

READER Q & A FOR THE WEEK

All Reader Q & A’s are listed at our web site!

Check it out at:

http://www.successful-investment.com/q&a.php

A note from reader Jeff:

Q: Ulli: I noticed you repurchased VNQ on July 10th at $69.91 after the sell stop was triggered from the high of $78.15. I thought you mentioned you would not re-enter a position you were stopped out of until it went back of above its high ($78.15). Please let me know if I’m misinterpreting your methodology.

A: Jeff: Yes; that is correct. However, there are 2 re-entry points. If VNQ breaks below its long-term trend line, then a crossing back above it would be the signal to buy back in. If, however, it does not break below its trend line, then the breaking of the previous high of 78.15 would be the re-entry point.

I have elaborated on this in my latest e-book as well.

———————————————————-

WOULD YOU LIKE TO HAVE YOUR INVESTMENTS PROFESSIONALLY MANAGED?

Do you have the time to follow our investment plans yourself? If you are a busy professional who would like to have his portfolio managed using our methodology, please contact me directly or get more details at:

https://theetfbully.com/personal-investment-management/

———————————————————

Back issues of the ETF/No Load Fund Tracker are available on the web at:

https://theetfbully.com/newsletter-archives/