ETF/No Load Fund Tracker Newsletter For Friday, October 11, 2013

ETF/No Load Fund Tracker StatSheet

————————————————————-

THE LINK TO OUR CURRENT ETF/MUTUAL FUND STATSHEET IS:

https://theetfbully.com/2013/10/weekly-statsheet-for-the-etfno-load-fund-tracker-newsletter-updated-through-10102013/

————————————————————

Market Commentary

Friday, October 11, 2013

TRADERS ENTERING THE WEEKEND ON HIGH HOPES

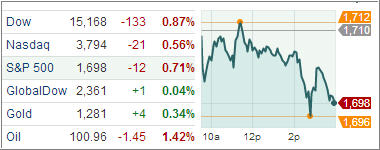

Domestic equity markets were able to extend their recent gains today, continuing a major rally in the previous session amid growing optimism that a solution to the budget and debt ceiling concerns may be delivered soon as negotiations continue on Capitol Hill.

The Dow Jones Industrial Average closed 111 points higher (0.7%) at 15,237, the S&P 500 Index gained 11 points (0.6%) to 1,703, and the Nasdaq Composite increased 31 points (0.8%) to 3,792. Elsewhere, treasuries were nearly unchanged on the heels of a larger-than-forecasted decline in U.S. consumer sentiment. Bond markets will be closed on Monday in observance of Columbus Day. Meanwhile, gold and crude oil prices were lower, while the U.S. dollar was flat.

In earnings news, Dow member JPMorgan Chase topped analysts’ expectations after excluding a large legal expense, while Wells Fargo exceeded analysts’ bottom line projections, but its revenues were bogged down by lower mortgage-related activity. The financial sector (+0.6%) ended in-line with the S&P.

Stocks climbed amid morning reports indicating a new proposal had been put forth by Republicans that would end the government shutdown and avoid a Treasury default. However, a subsequent White House meeting failed to produce a concrete agreement. In the end, the two sides did not appear to be much closer to a solution as the shutdown is set to enter its third week.

Even though the deadlock has yet to be resolved, equities cheered the mere presence of some form of discussion. All ten sectors registered gains with energy (+1.0%) ending in the lead. The sector posted a solid gain even as crude oil fell 1.0%.

Meanwhile, the other commodity-related sector-materials–underperformed as miners weighed. The Market Vectors Gold Miners ETF fell 2.1% while gold futures tumbled 2.1%. Elsewhere among cyclical sectors, discretionary shares (+0.8%) finished ahead of the broader market with homebuilders contributing to the strength. The iShares Dow Jones US Home Construction ETF advanced 1.7% as all major builders rallied. After a shaky start, stocks finished in the positive to close the week.

The Dow rose 1.1 percent, the S&P 500 rose 0.7 percent while the Nasdaq fell 0.4 percent as some of the strongest gainers in the tech sector sold off during week as investors were taking profits. Earnings season will be in full swing next week but fiscal issues will remain a main focus for traders, and the U.S. government shutdown could continue to complicate the economic calendar.

With the 2-day rally overcoming the early sell-off, our Trend Tracking Indexes (TTIs) edged slightly higher and closed as follows:

Domestic TTI: +3.01% (last week +3.02%)

International TTI: +6.41% (last week +6.14%)

Have a great week.

Ulli…

————————————————————-

READER Q & A FOR THE WEEK

All Reader Q & A’s are listed at our web site!

Check it out at:

http://www.successful-investment.com/q&a.php

A note from reader Bill:

Q: Ulli: On 9-6-13, FOCPX dropped 8.8% about $6.66 per share. I called a Fidelity rep and he said because Apple fell 9-10% and FBIOX also declared and paid a Capital Gain and Dividend of around $1.189 per share, but it’s sort of floundering around not moving and actually down three days in a row for the last three days.

I guess my question is, are people getting out because of that drop and should I get out also?

I understand when a lot of people get out of a fund they have to sell off and that makes the fund drop.

A: Bill: Here’s how I look at it:

FOCPX made a high of 80.84 on 8/5/13, which would be the number to use for your trailing sell stop. Say, 7.5% of that high would put a sell signal at a break below 74.78, which happened only briefly before this fund recovered. I could not verify the distribution of $1.19.

If that is in fact correct, you need to reduce the high price by that amount, which would make the new high $79.65. Now you calculate the sell stop point of 7.5%, which brings it down to $73.68, which has not been reached yet.

That’s the process I go through to determine if a stop has been triggered. If it has, I will execute the next day, unless there is a huge rebound in the making.

Hope that clarifies your thinking.

———————————————————-

WOULD YOU LIKE TO HAVE YOUR INVESTMENTS PROFESSIONALLY MANAGED?

Do you have the time to follow our investment plans yourself? If you are a busy professional who would like to have his portfolio managed using our methodology, please contact me directly or get more details at:

https://theetfbully.com/personal-investment-management/

———————————————————

Back issues of the ETF/No Load Fund Tracker are available on the web at:

https://theetfbully.com/newsletter-archives/