The ETF/No Load Fund Tracker

Monthly Review—March 31, 2014

US Equities Log Mixed Results In March; Europe Rallies To A Seven-Month High

US stock indexes logged in a mixed performance in March with the benchmark S&P 500 ending both the month and the first quarter of 2014 with modest gains despite geopolitical uncertainties and the continued reduction in Federal Reserve asset purchases.

The S&P 500 closed at 1,872.34, up 0.7 percent for the month. This was the fifth straight quarterly rise for the benchmark index and at 1.3 percent, the smallest three-month advance since the fourth quarter of 2012.

The Dow Jones Industrial Average finished at 16,457.66, marking a gain of 0.8 percent for March. The blue-chip index, however, shed 0.7 percent for the quarter.

The NASDAQ Composite index ended at 4,308.11, down 2.5 percent for the month. That was the index’s worst performance since October 2012.

The tech-heavy index, however, managed to notch a 0.5 percent gain for the quarter.

The US economy showed signs of revival in March, shrugging off the winter chills that had slowed down recovery considerably in the first two months of the year.

The labor market continued to heal with hiring by the US private sector picking up in March. Data released by Automatic Data Processing Inc showed US companies increased payrolls by 191,000 last month. The payroll processor also revised its February reading to 178,000 from an earlier estimate of 139,000.

US non-manufacturing and service sector growth gained pace in March, according to data released by the Institute for Supply Management. The non-manufacturing index rose to 53.1% in March from 51.6% in the previous month, slightly falling short of the 53.3% reading economists had called for.

Readings above 50% signal expansion – the higher the reading, the faster the expansion.

Personal income rose for a second consecutive month in February. At 0.3 percent, February’s income growth matched January’s pace and exceeded the 0.2 percent clip forecast by economists.

Personal spending grew 0.3 percent from a downwardly revised 0.2 percent in January, matching expectations. The Commerce Department revised fourth-quarter GDP growth upwards to 2.6 percent from an initial reading of 2.4 percent.

On the downside, the US trade deficit in February rose to a five-month high mainly due to falling exports and rising imports. The Trade gap widened to a seasonally-adjusted $42.3 billion from $39.3 billion in January.

Data released by the Labor Department showed new jobless claims rose by 16,000 to a seasonally-adjusted 326,000 in the week ending March 29. Most economists surveyed projected an increase of 10,000 claims.

At a press conference on March 19, Federal Reserve Chairwoman Janet Yellen caught the markets by surprise when she said the central bank could raise interest rates in about six months after ending its bond purchase program. That would mean policy tightening as early as the first half of 2015.

However, speaking at a community development conference in Chicago on March 31, Yellen said the US economy would require loose monetary policies for “some time” as the “scars” from the 2008 market collapse are yet to heal, indicating the Fed will remain accommodative for a long, long time.

Across the pond, European stocks tracked US equities in March. The pan-European Stoxx Europe 600 index finished March at 334.31, up 1.8 percent for the quarter.

European Central Bank President Mario Draghi has assured investors repeatedly that the central bank will act if disinflation risks started to affect the region’s price stability. However, ECB Governing Council member and German Bundesbank Chief Jens Weidmann said last Saturday the central bank should not overreact to a temporary fall in prices. The ECB has little control over a one-off drop in energy and food prices that caused the recent weakness in prices, Weidmann argued, giving the impression the central bank don’t believe circumstances warrant policy action at this stage.

In the end, it’s been a good news bad news type of month, which had the major indexes vacillating in both directions.

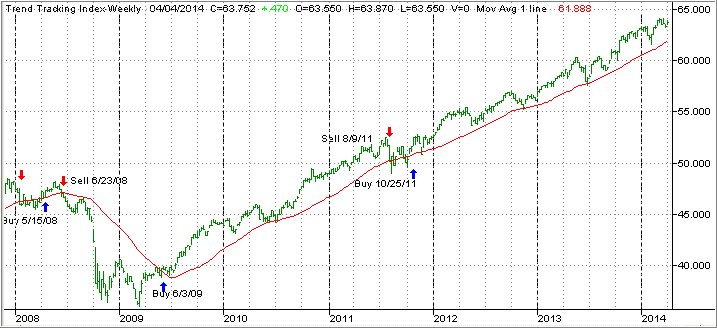

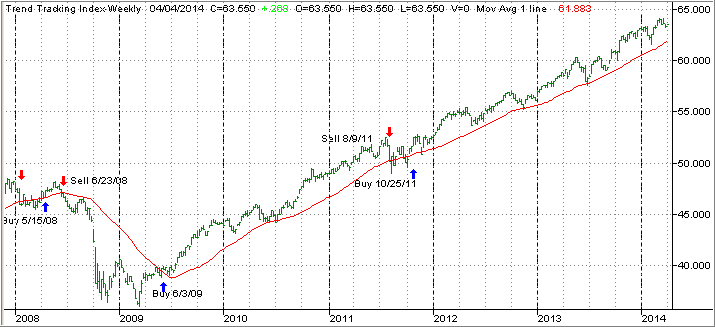

Our main directional indicator, the Domestic Trend Tracking Index (TTI), pulled back from its February highs and settled lower but still stays above its long term trend line:

The index itself (green line) now hovers above the trend line (red) by +2.91% (last month +4.34%).

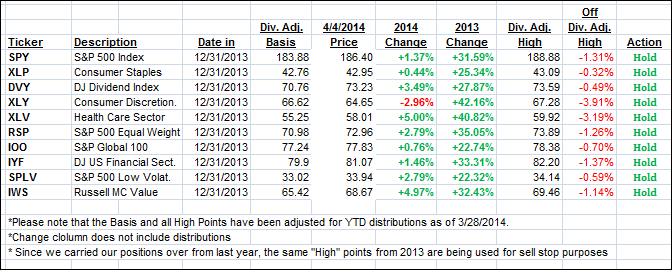

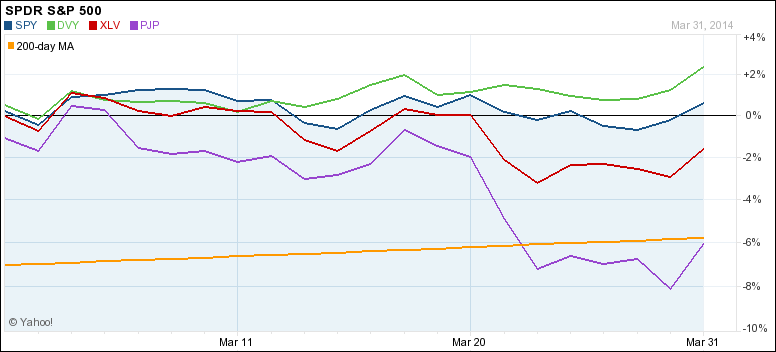

That means we will hold on our current ETFs subject to their trailing stops. Last month’s pullback caused one casualty in that our small holding in pharmaceuticals (PJP) triggered its sell stop and was liquidated.

You can see the sometimes violent up and down moves in this monthly chart, which reflects our current main holdings:

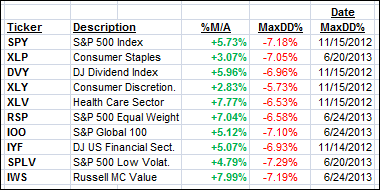

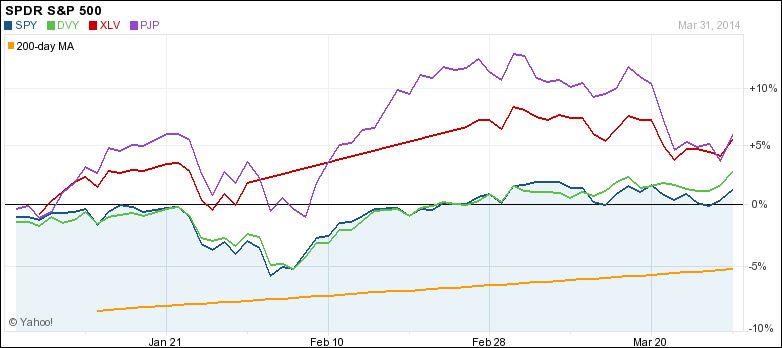

As I commented last month, pharmaceuticals (PJP) and healthcare (XLV) had been on a strong upswing, which came to an end in March with especially PJP hitting the skids. XLV gave back a little but is still our leader on an YTD basis as the Quarterly chart demonstrates:

Healthcare has been less volatile than the pharmaceuticals and has rewarded us with some nice returns over the longer run. I will hold on to it, unless its sell stop gets triggered.

The markets seem to have somewhat normalized after strong gains in February, which pretty much made up for the losses in January. It’s interesting to note that, despite the sell offs in 2014, some of our core holdings in SPY, DVY and XLV have held steady and have given us continued market exposure as sell off were followed by rallies with some indexes (SPY) making new lifetime highs.

That’s what’s important; to be exposed with our core holdings to steady and slower moving indexes, which keep us invested until a serious trend reversal occurs. That idea will be my continued motto as we ease into the second quarter of 2014.

The March US nonfarm payrolls number was slightly disappointing as economists had forecast a higher reading although revised estimates for February came in better than expected.

The March US nonfarm payrolls number was slightly disappointing as economists had forecast a higher reading although revised estimates for February came in better than expected.