- Moving the market

This morning, the Dow and S&P 500 surged into record territory following President Trump’s announcement of his Treasury secretary nominee, Scott Bessent.

Traders reacted positively to the news, cheering the nomination of the hedge fund manager, who recently suggested that any tariffs proposed by Trump should be implemented gradually.

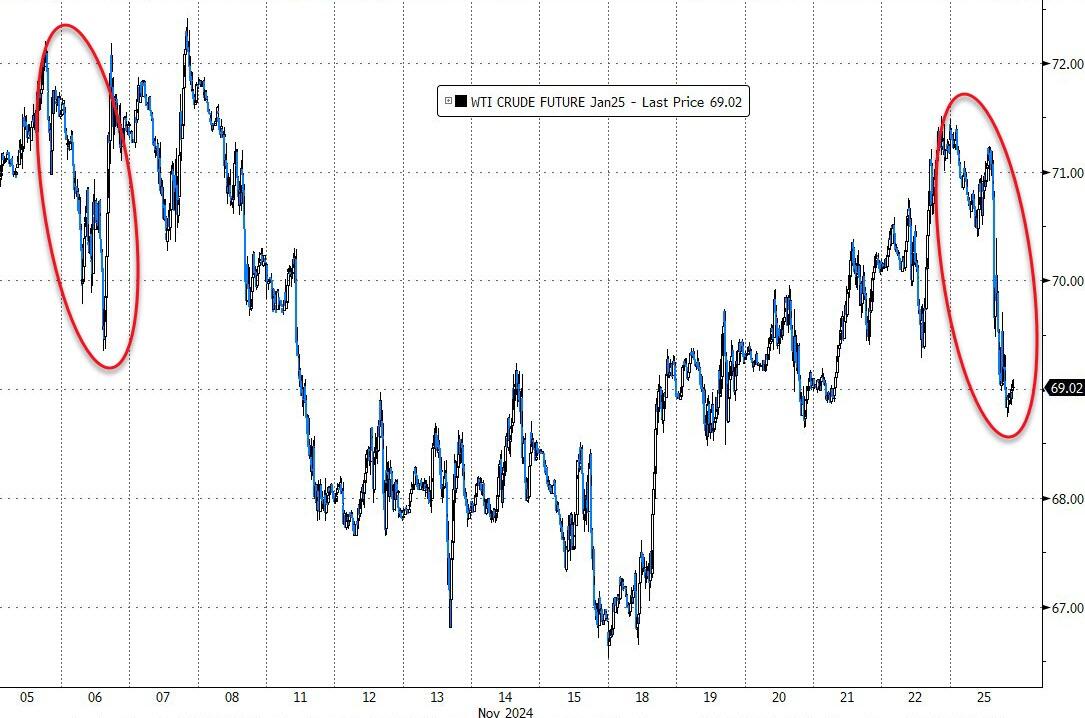

Despite the potential peace deal between Israel and Lebanon, the markets experienced significant volatility.

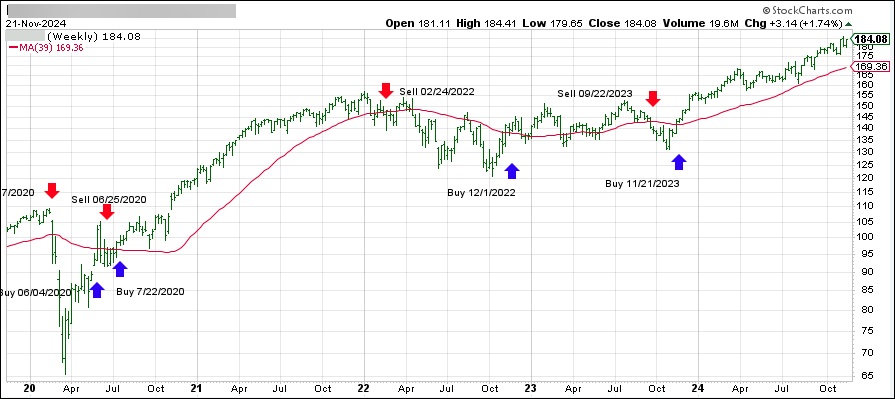

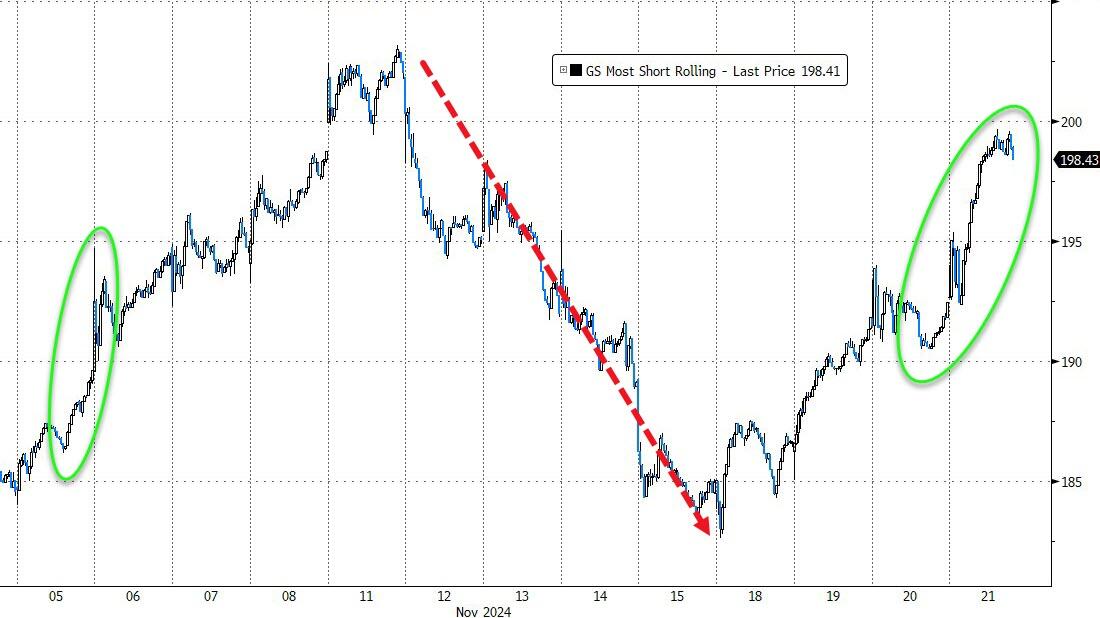

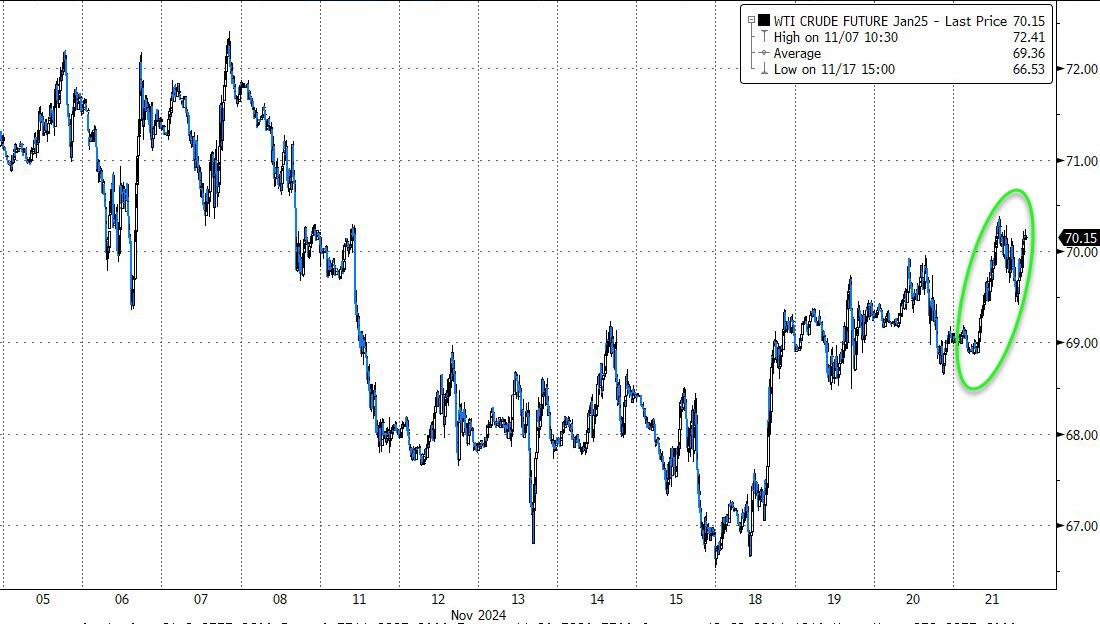

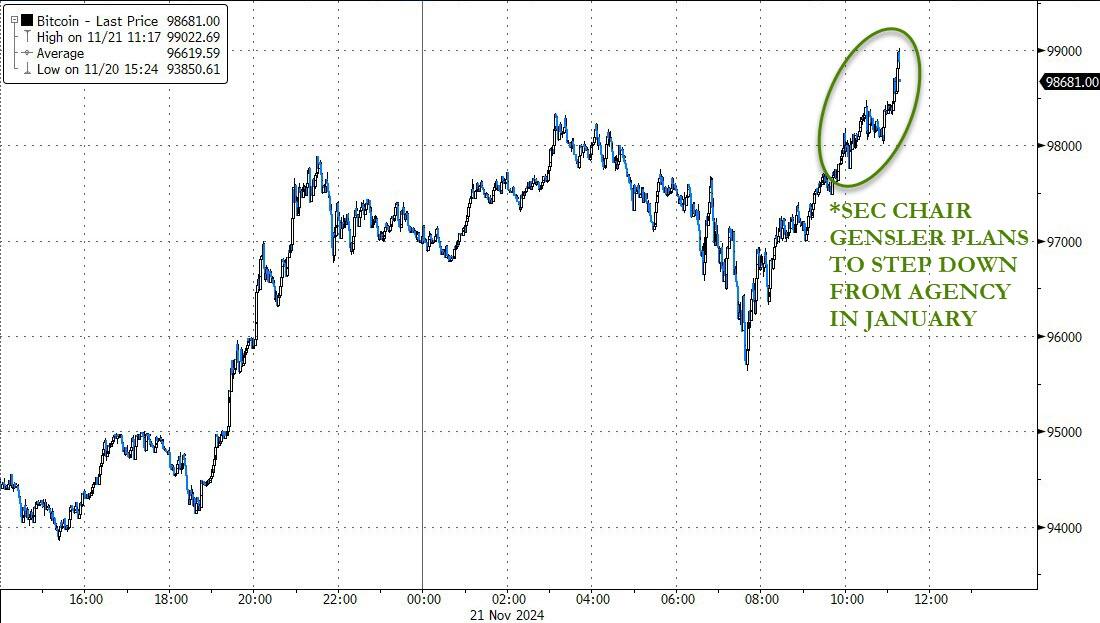

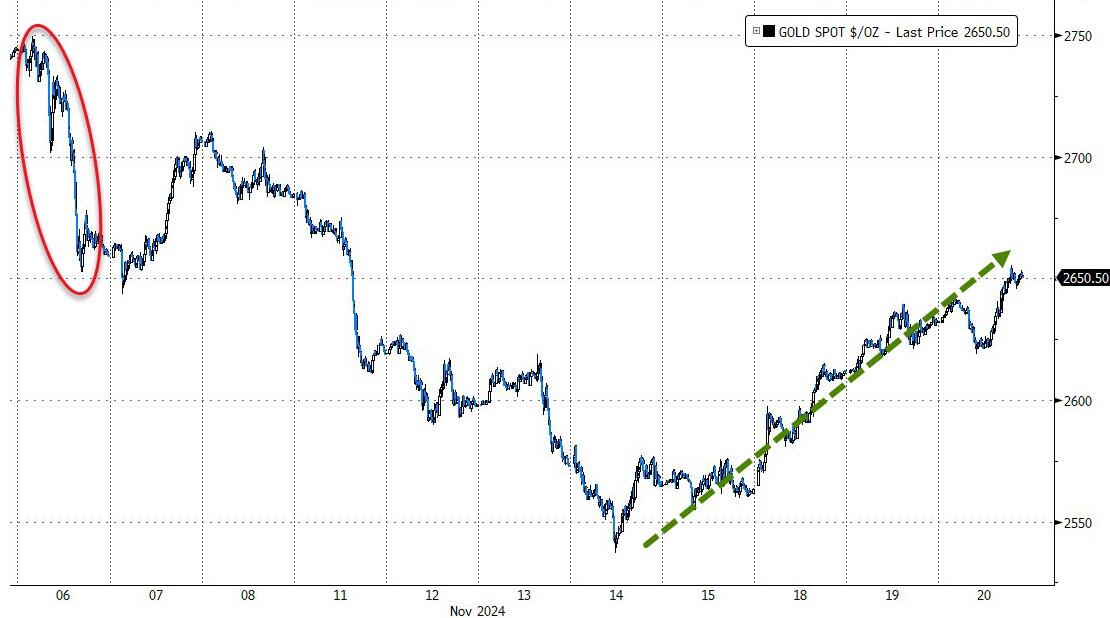

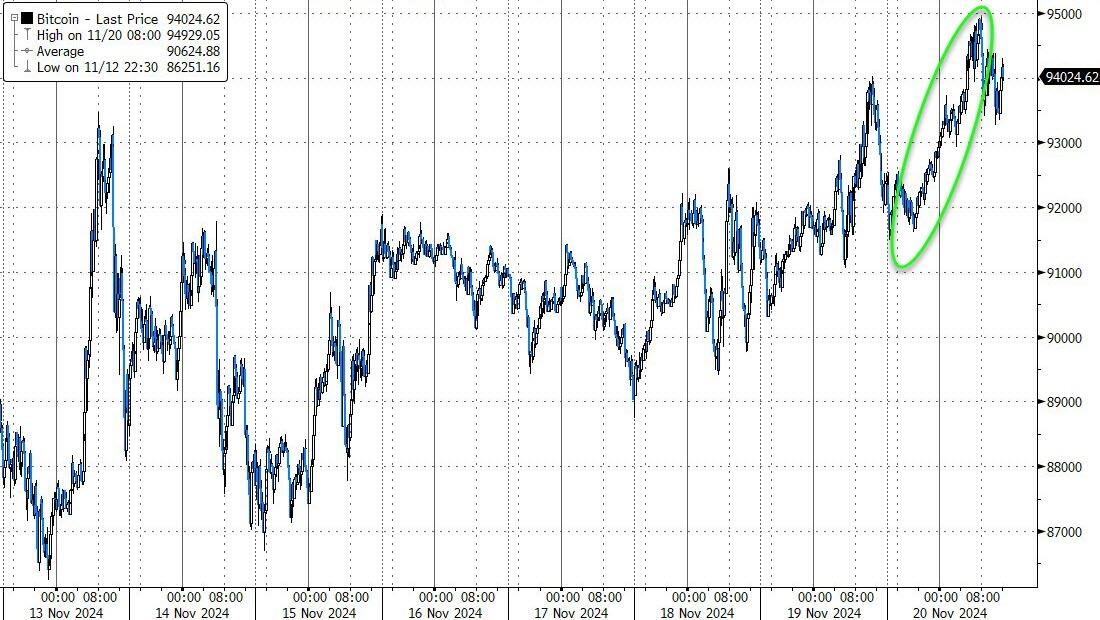

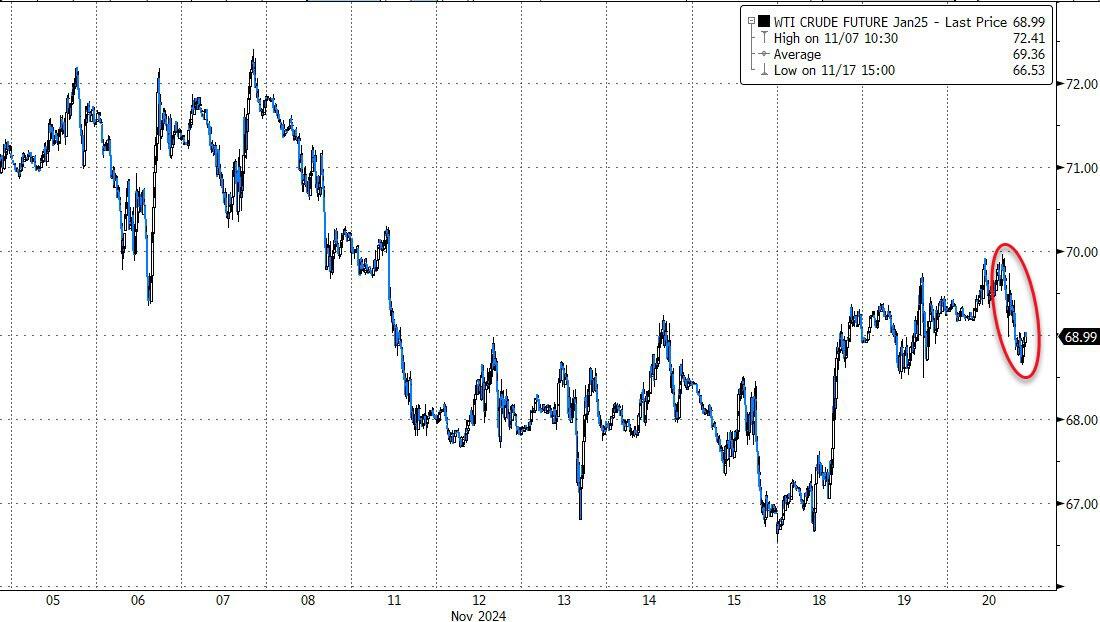

Crude oil, Bitcoin, and gold all declined, while stocks rallied, led by Small Caps, which benefited from a continued short squeeze. However, the Mega Cap basket slipped again, with one trader humorously describing it as a “source of funds for buying other stuff.”

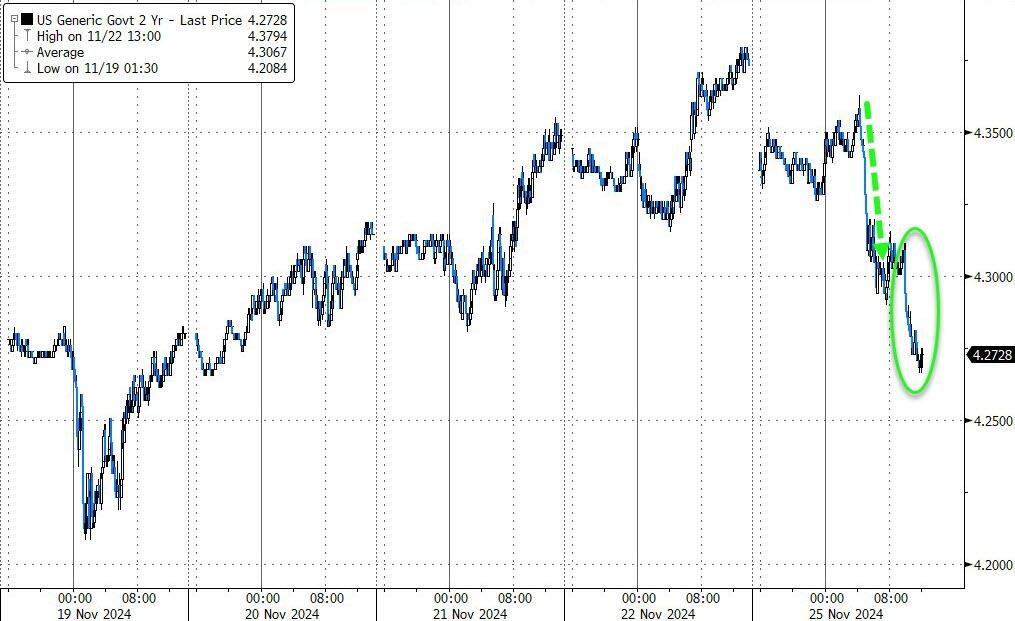

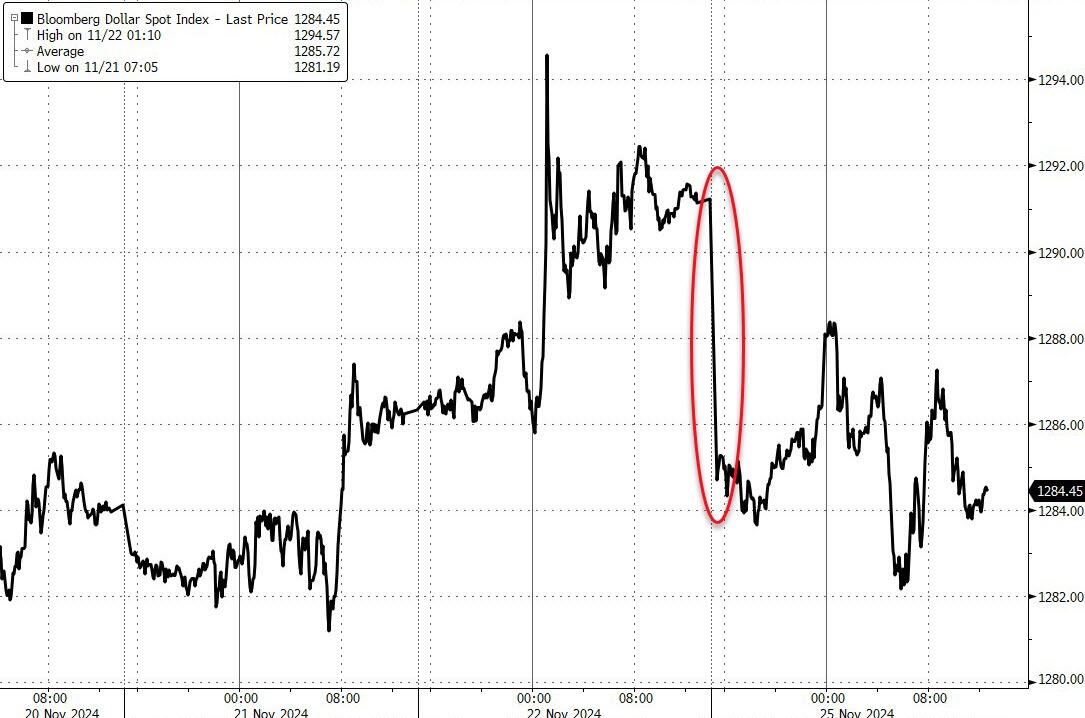

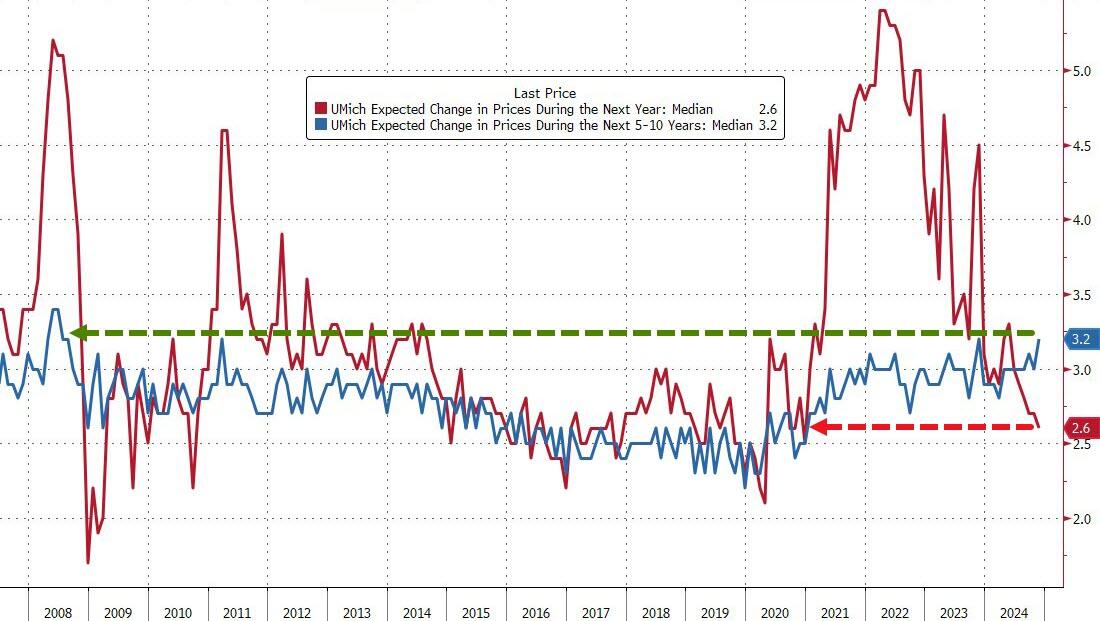

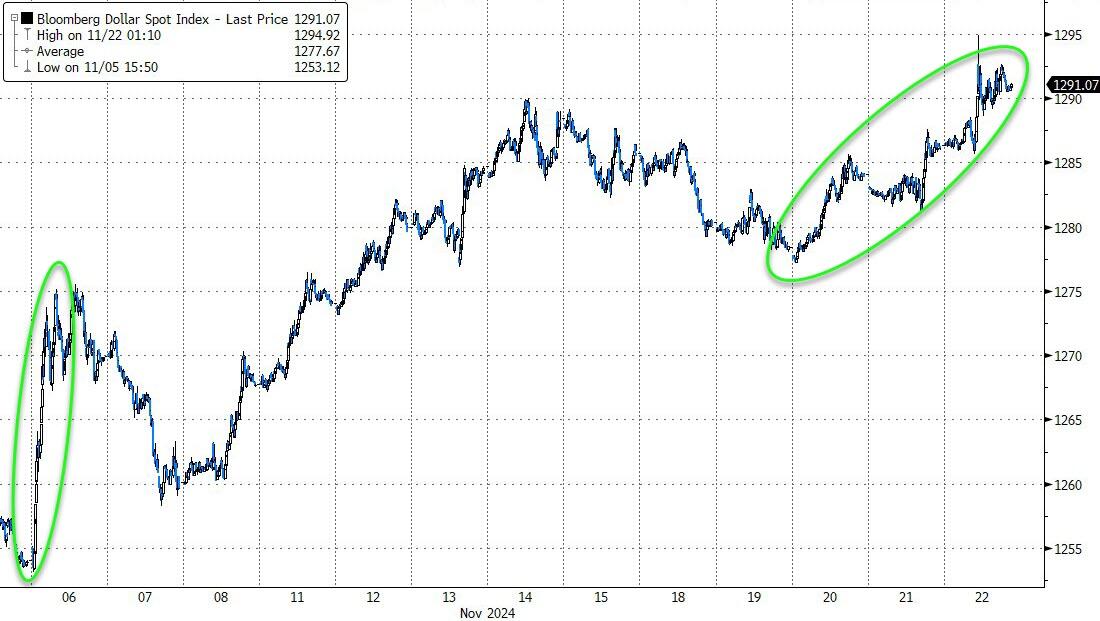

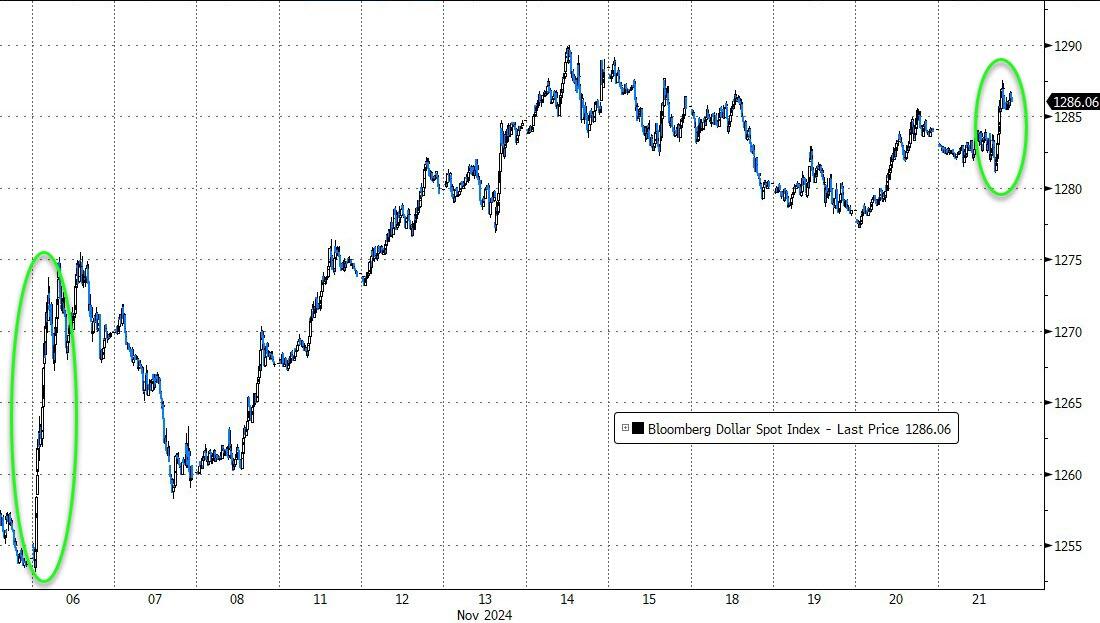

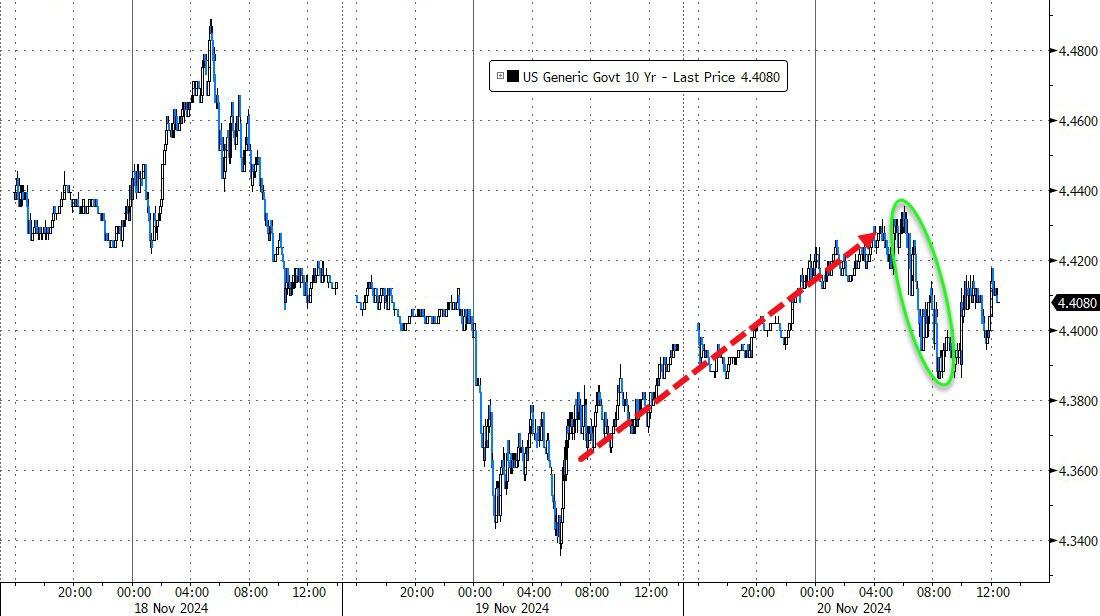

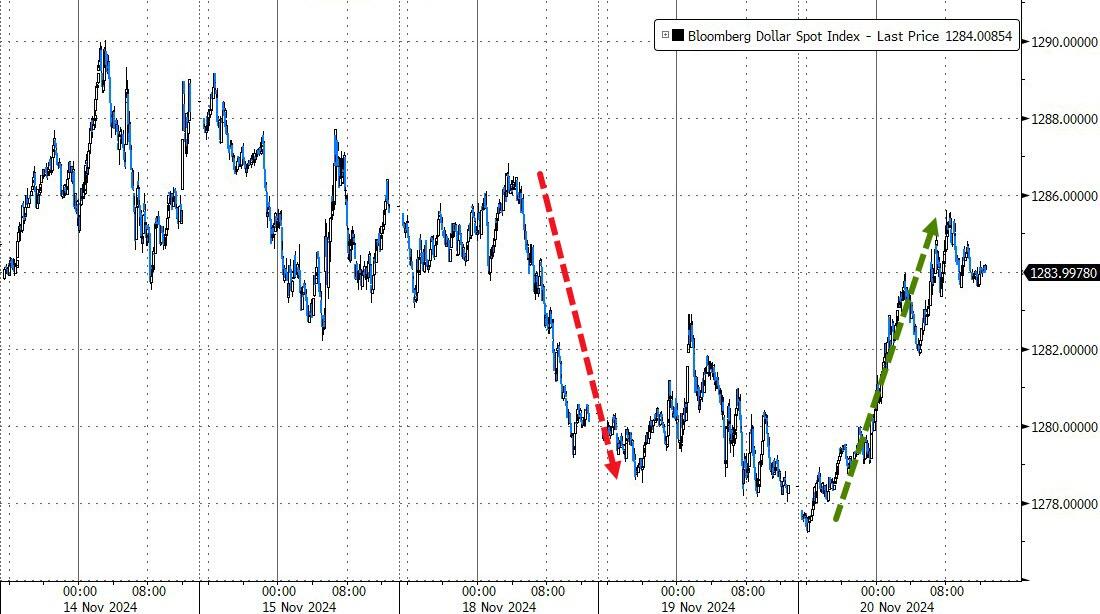

Lower bond yields provided support for the major indexes, with the 2-year yield plunging significantly. The dollar followed gold lower after its recent relentless rise.

The options market indicated a strong bullish sentiment, with 65% of all options traded being calls, reaching a level of optimism not seen since December 2021.

Read More

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}