- Moving the Markets

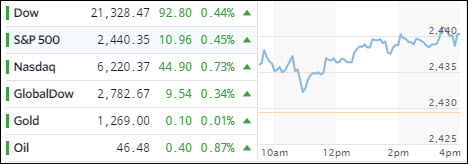

The pullback of the last 2 days ended, at least for the time being, with the Nasdaq and S&P 500 moving into record territory, while the Dow touched an all-time high on an intra-day basis as the Fed started its two-day meeting on interest rates. Even the Russell 2000 hit a record high at a moment in time when its 2017 EPS expectations hit 2017 lows. Makes perfect sense to me…

The result of the FOMC conference will be announced tomorrow with market observers holding a nearly unanimous view that interest rates will be hiked by +0.25%. That means traders are comfortable and are assuming that the Fed will balance things in a way so that a tighter monetary policy does not have a negative effect on growth. Hmm, given that economic data points have collapsed that will be quite a magic act for the Fed to perform.

Interest rates vacillated but ended the day unchanged with the 10-year T-Bond maintaining its 2.21% yield. The US dollar slipped for the second day in a row with UUP closing down -0.12%.