ETF Tracker StatSheet

https://theetfbully.com/2017/10/weekly-statsheet-etf-tracker-newsletter-updated-10122017/

ENDING THE DAY AND THE WEEK WITH A GAIN

- Moving the Markets

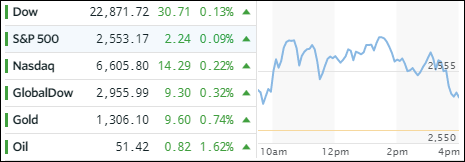

The trading range for the major indexes turned out to be a narrow one not just for the day but for the week as well. Nevertheless, we closed slightly up with the Nasdaq logging its 57th all-time high. While weekly gains were modest, they stretched across all asset classes including stocks, bonds (Treasuries and Corporate), gold and crude oil.

In ETF space, we saw more winners than losers. Leading the charge to the upside today were Emerging Markets (SCHE) with +0.94% followed by Semiconductors (SMH) with +0.68% and International SmallCaps (SCHC) with +0.55%. On the downside, Transportations (IYT) gave back -1.04% of their recent gains as did Aerospace & Defense (ITA), which slid -0.45%.

Interest rates continued their slide with the 10-year yield slipping 5 basis points to end the day at 2.28%. That helped the 20-year bond (TLT) price to jump +0.72%. After several attempts, gold finally succeeded in conquering its $1,300 milestone again by gaining +0.74%. The US dollar traded in a tight range and remained unchanged for the session but fell for the week.