- Moving the markets

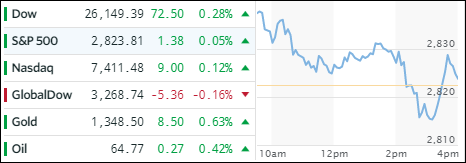

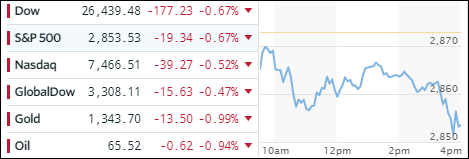

It was another roller coaster ride with the indexes vacillating around their unchanged lines. A nice mid-day rally fizzled out and accelerated to the downside in the last hour when dip buyers stepped in to limit the damage. Volatility picked up due to rising interest rates and inflation along with uncertainty ahead of tomorrow’s jobs report.

The mixed picture carried over to ETF land where winners and losers were just about evenly matched. Bucking the bearish trend were Financials (XLF +0.94%), Aerospace & Defense (ITA +0.57%) and International SmallCaps (SCHC +0.42%). On the other end of the spectrum, we saw Emerging Markets (SCHE -1.41%), Semiconductors (SMH -0.61%) and Transportations (IYT -0.56%) closing in the red.

The bond arena saw a bloodbath today with the yield on 10-year jumping 6 basis points to 2.78%, a level last seen in April 2014, while the 30-year climbed above the 3% level to end the session at 3.01%. As a result, bond prices plunged with the widely held 20-year (TLT) losing -1.45%, which it had last visited in May last year.

If you are wondering how the US dollar (UUP) fared in this environment, it should come as no surprise that it got spanked as well (-0.52%), or monkey hammered as some analysts referred to it. But, but, as President Trump recently confirmed, we have a strong dollar policy. Go figure…