- Moving the Markets

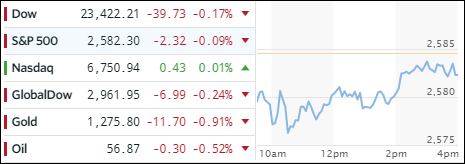

The major indexes sagged as uncertainty about the tax reform tug-of-war continued to take center stage. Not helping matters was a dive in crude oil along with weakness from heavyweights Apple (AAPL) and Boeing (BA).

But the stock that really took a spanking was GE (-5.89% for the day) after cutting its dividend by 50% yesterday. If you think that was bad, GE has now lost -43.4% YTD in a year were bulls ruled and the Dow climbed +18.5%. So much for putting too much credence into the payment of dividends!

Despite red numbers in the major indexes, we saw some green ones in ETF space. Aerospace & Defense (ITA) resisted the southerly trend along with, ironically, the Dividend ETF (SCHD) with modest gains of +0.15% and +0.12% respectively. On the downside, Emerging Markets (SCHE) led with -0.69% followed by Transportations (IYT) with -0.28%.

Interest rates retreated with the 10-year yield dropping 2 basis points to 2.38%, which allowed the 20-year bond (TLT) to recapture some of its recent losses by rallying +0.68%. The High yield bond ETF (HYG) was not so lucky and lost another -0.43%, which brought the price down to levels last seen in August.

Not to be outdone, the US Dollar (UUP) did a swan dive, gapped down -0.69% and is now honing in on a break of its 200-day M/A to the downside.