- Moving the markets

Today was a repeat of what we’ve seen a lot of lately. An early rally reversed mid-day, headed south below the unchanged line, but a last-minute bullish push shoved the major indexes back into the green, but only by a tiny margin.

The walls of worry remain a deterioration in global growth and the upcoming results tomorrow of the Fed’s two-day meeting on interest rates. Will the Fed cave and become dovish or stay the course set on a hawkish path?

A more dovish view could ignite the bulls—at least on a temporary basis and create the much-desired Santa Claus rally. What exactly is it? Trader’s Almanac defines it as follows:

The Santa Claus rally is a “short, sweet, respectable rally within the last five days of the year and the first two in January” with an average gain of 1.3%. It warns, however, that “Santa’s failure to show tends to precede bear markets”.

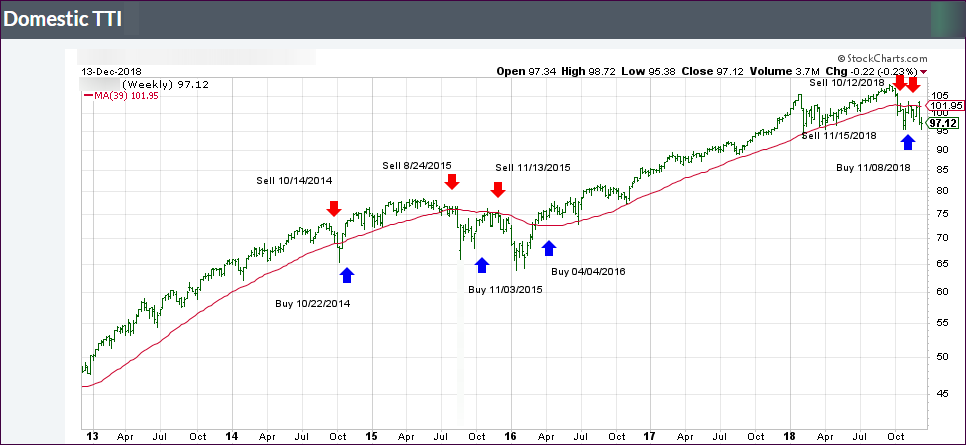

If that were to happen, the average gain would not be enough for the markets to climb out of their bearish range, at least the way I define it as per my Trend Tracking Indexes (TTI). It would merely represent a bounce in an ongoing bear market.

So far, and that is hard to believe, December has extended its worst performance since, get this, 1931! With global markets showing weakness wherever you look, today it was Crude Oil that got spanked at the tune of -7.34% with a hard landing at $46.22/barrel. Oil prices have now collapsed 40% from recent highs, and the Fed is scheduled to hike rates?

Hmm…

It promises to be an interesting day tomorrow.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}