- Moving the markets

Right after the opening bell, equities hit the skids with the Dow dropping some 300 points before finding some footing. Causing this upheaval was the European Central Bank’s (ECB) Draghi, who unveiled a massive monetary easing program and an extended NIRP (Negative Interest Rates) period.

While that should have been a positive for equity markets, it wasn’t! Stocks stumbled, which was a reaction the market has rarely ever seen before considering that a Central Bank announced a surprisingly dovish move, even though it was in the face of a ‘substantial’ downward revision to EU growth from +1.7% to +1.1%.

So, what does that mean? Some analysts think this adverse reaction is a clear sign suggesting that Central Banks are losing control over markets by attempting to push stocks too far. The fallout was worldwide with U.S. equities following the bearish trend.

The ECBs surprise policy move sent shivers through global markets. It remains to be seen whether this is just an outlier, or a sign of things to come, but worries about a slowing global economy just reached a new high.

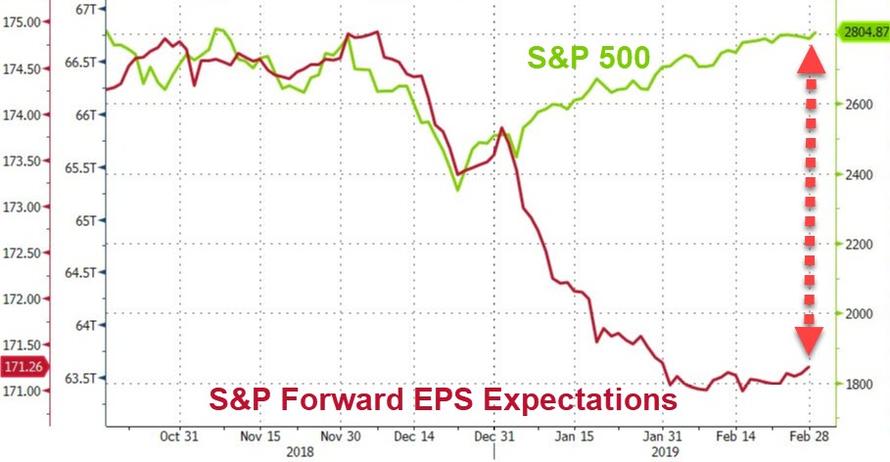

Since all countries are inter-connected to varying degrees, the U.S. will not be able to decouple and will experience some slowdown as well. Judging by the recent weakness in econ data points, we already have seen this process in motion; the financial markets, however, have so far been oblivious to it.

Domestically, the S&P 500 dropped below its 200-day M/A, managed to crawl back above it but ended up succumbing to bearish forces by closing slightly below it. Remember, for many Wall Street traders, this line represents the divider between bullish and bearish territory and therefore is currently seen as a critical support level which, once clearly broken, could signal the end of this current bullish phase.

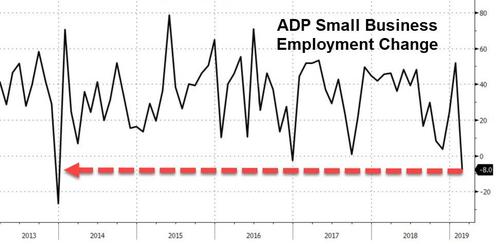

Finally, ZH just couldn’t help themselves but pose the question: “It can’t be this easy, right?”

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}