- Moving the markets

The bulls and bears engaged in another gathering of tug-of-war with the major indexes vacillating around their respective unchanged lines and, in the end, closing with no clear direction apparent.

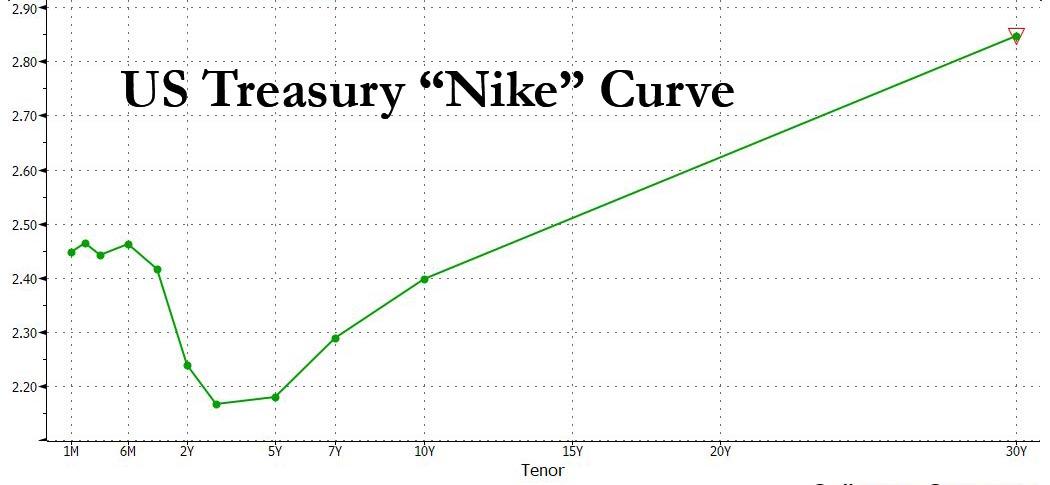

The fallout from last Friday was obvious, as global weakness carried into today, but enough bullish momentum turned this into an uneventful session. Not helping were continued concerns about the inversion of the yield curve where short term bonds are now sporting a higher yield than longer term ones.

As a result, the focus today was more on bonds than the equity gyrations. Note that the 10-year bond yield plunged to its lowest level since 2017 but managed a modest rebound of 3 basis points to close at 2.406% after touching the 2.39% level.

As ZH pointed out, more concerning was the ongoing slide in the 3 month-10-year bond spread, the Fed’s favorite recession indicator, which briefly plunged as much as 7 basis points before recovering to drop just 3 basis points.

If you are not familiar with it, this simply means that if you invest your money in a 3-month-bond you get more interest vs. having your funds tied up in a 10-year one. This chart demonstrates this insane oddity.

At day’s end, ZH pondered these critical questions:

Will Asia continue its selling, as the US bond market now screams global recession, and will the S&P finally breakdown as it breaches the next support level of 2,777 and if so, will it retest the December lows over 400 points lower, as so many bears have recently predicted?

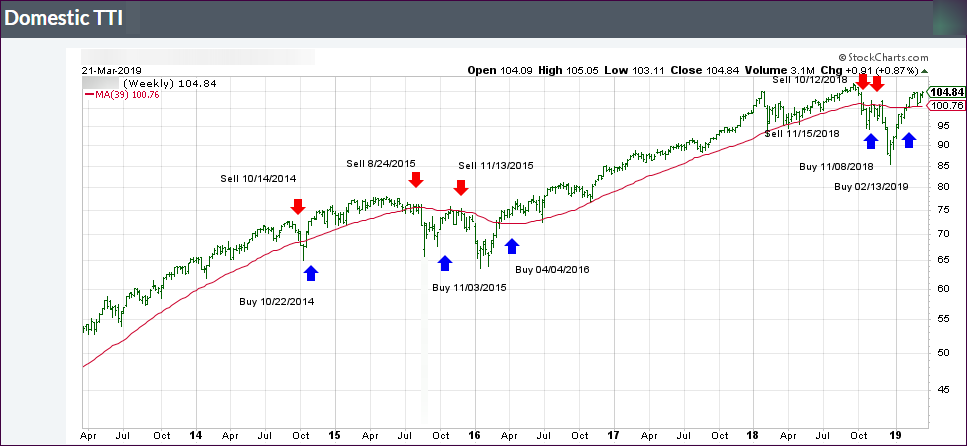

Since no one has the answer, we must be prepared to deal with this type of scenario. Our Trend Tracking Indexes (TTIs) will lead the way and give us the signal when it’s time to head for the safety of the sidelines.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}