- Moving the markets

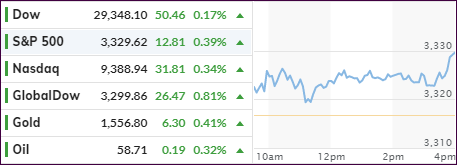

As this chart shows, news about the coronavirus played havoc with market direction over the past 3 days, with optimism causing rallies and pessimism pulling equities back down.

The overall impact was relatively minor so far, given the relentless march higher over the past few months. An early drop caught some support, and a slow but steady climb out of that early hole helped the major indexes to close moderately in the green, with the Dow falling just short.

Still, China continues to struggle to get a handle on the viral outbreak that has so far killed 17 people and infected 650 in several countries, according to MarketWatch. Helping the markets recover was a statement from WHO (World Health Organization) that they will not yet declare the coronavirus outbreak to be a global health emergency.

A good old-fashioned short squeeze kicked in, after the early market drop, and made its contribution to the recovery of the indexes back towards the unchanged line. As the Nasdaq touched new record highs, bond yields went the other way causing a divergence, one of the many we’ve seen over the last year, with none of them having affected equities negatively.

For right now, the major trend remains firmly in place.

Read More

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}