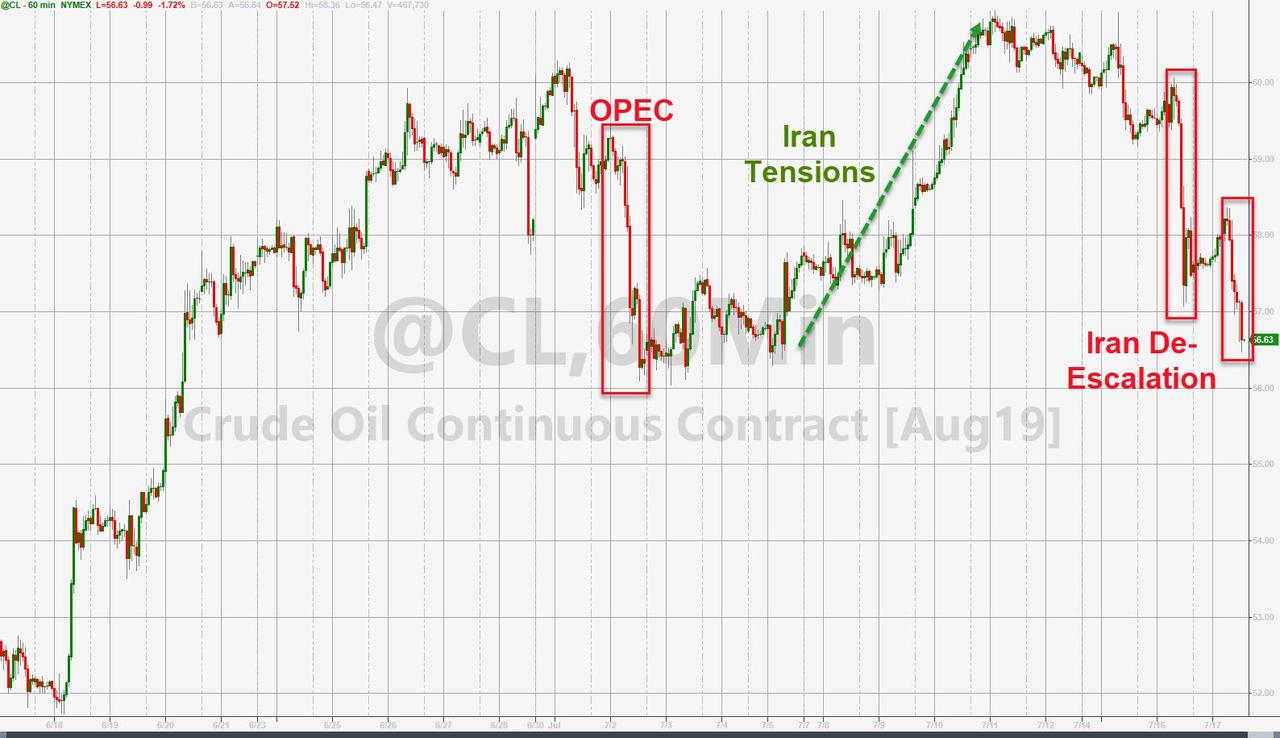

- Moving the markets

Yesterday, the markets closed on a sour note by scoring their lows for session in the final seconds of trading. That usually does not bode well for the next day’s opening, and today was no exception.

The major indexes slipped early on but managed to rebound by mid-day with fresh upward momentum pushing equities into the green, caused by the Fed’s Williams opining that:

“interest rates should be cut as insurance against an economic downturn,”

And

“when you have only so much stimulus at your disposal, it pays to act quickly to lower rates at the first sign of economic distress.”

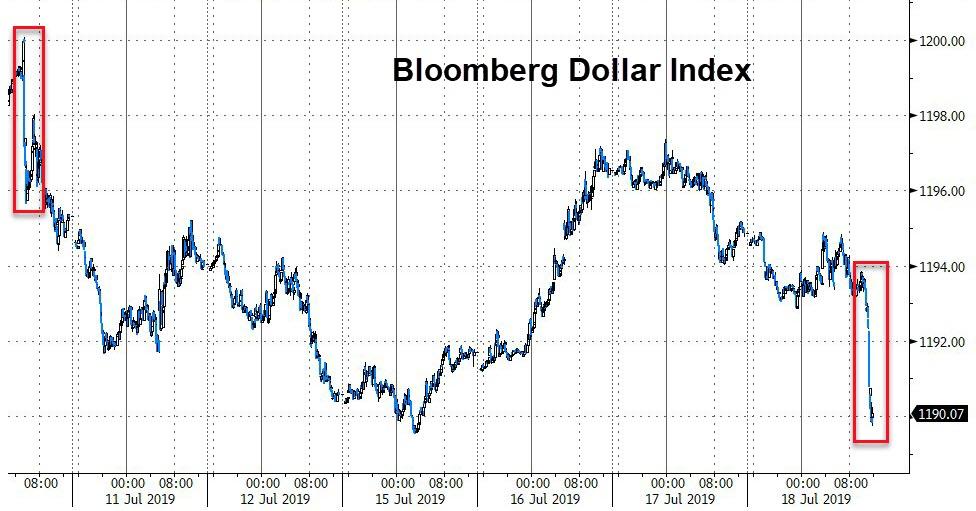

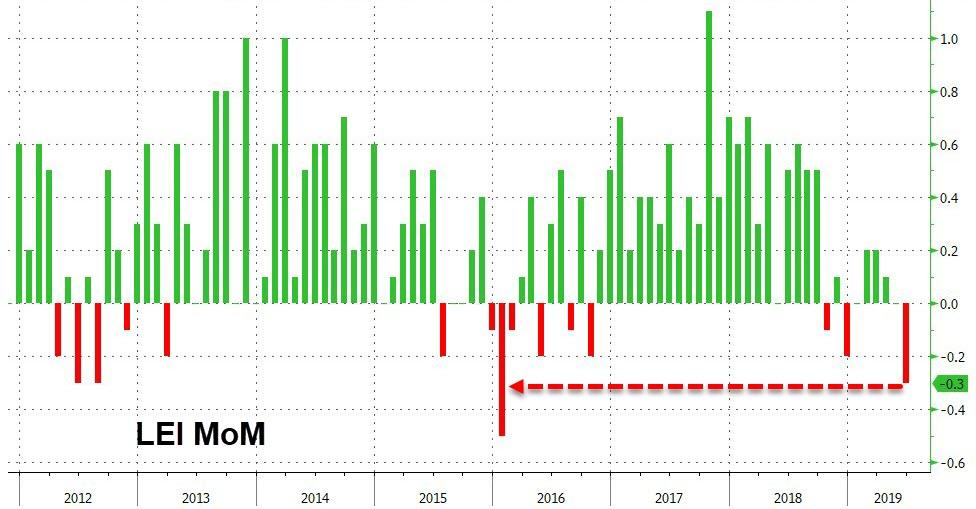

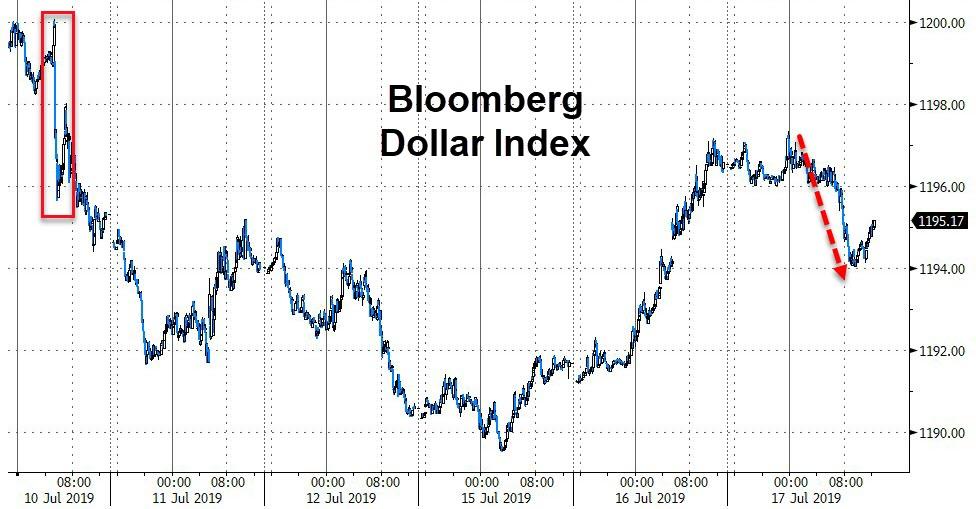

That pretty much saved the day for stocks but took the starch out of the US dollar, as the latest Leading Indicators headline did not help matters. They slumped the most in over 40 months by tumbling -0.3% in June, which was their biggest MoM drop since early 2016.

Then the WSJ reported that trade-deal negotiations between the U.S. and China had hit a snag (what else is new?) raising doubts about whether the warring parties can ever reconcile their differences.

On the earnings front, things were mixed at best with Netflix being the loser of the day by surrendering almost -11%. This was due to a bad miss on expectations for new paying subscribers.

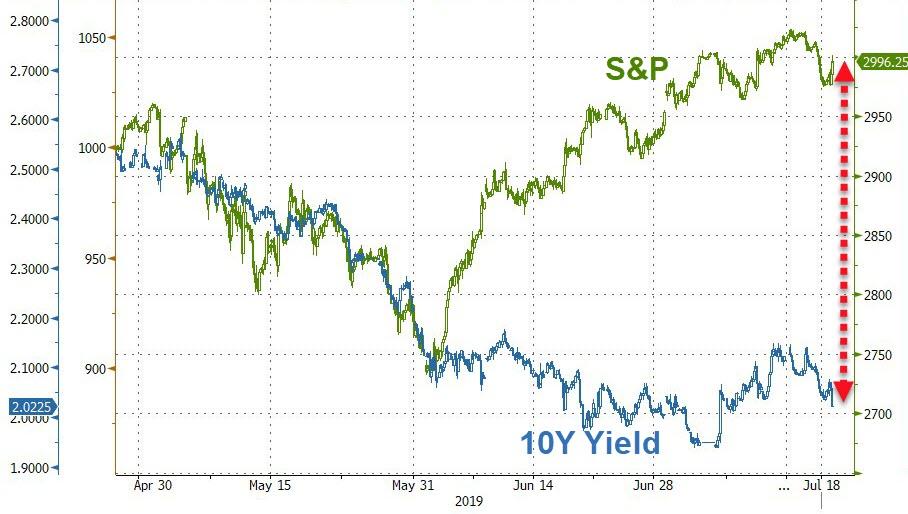

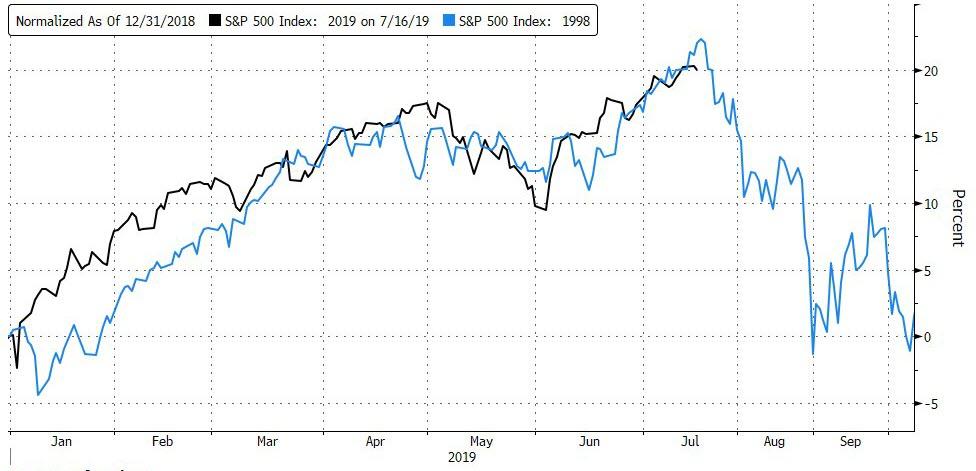

In the end, the S&P 500 failed to reclaim its recently lost 3k marker, while the Dow barely held on to a green close. The decoupling between the S&P 500 and the 10-year yield continues uncompromisingly, the latter of which has been now trending back towards the 2% level.

Read More

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}