- Moving the markets

It was another trading day during which uncertainty ruled. The major indexes survived an early sell-off and bounced back only to be slammed back down below their respective unchanged lines.

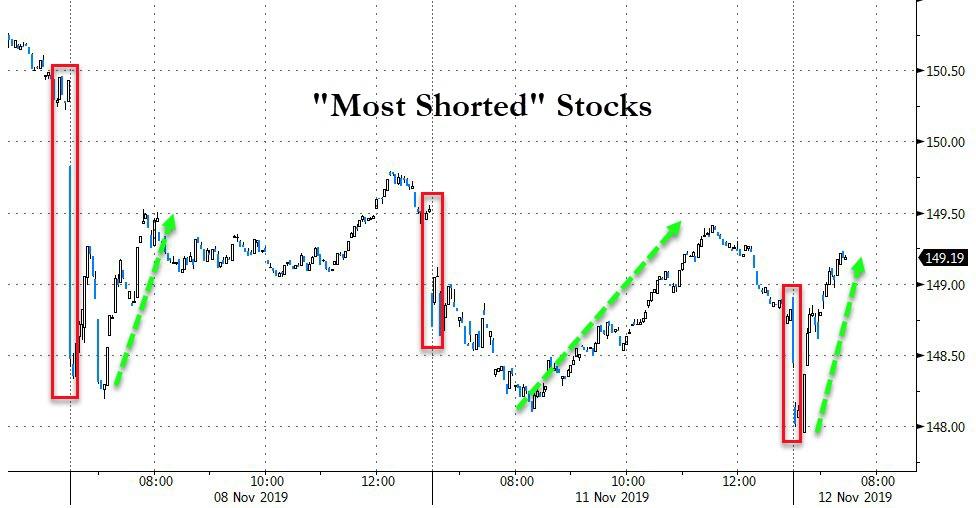

Give credit to the mid-day slam to a US-China trade problem, caused by reports that that a snag was hit over farm purchases. Then China barked by “resisting US requests for tech-transfer curbs and any enforcement mechanism.” Needless to say, the markets were not amused and down we went, while at the same time the latest short squeeze appeared to have run out of ammunition.

In the end, however, the indexes managed a comeback into the green with the weakling being the Nasdaq, which bumped against its unchanged line but failed to conquer it.

However, I consider one development today an important one, namely that the recent bond sell-off, during which the widely followed 10-year yield spiked dramatically, thereby taking the starch out of low volatility ETFs like SPLV, appeared to have reversed. After pushing towards the 2% level, the yield pulled back and closed at 1.88%, which allowed SPLV finally to have a good day by gaining +0.78% vs. the meager +0.05% the S&P 500 (SPY) generated.

While the 5-week old rally continues to roll on, today’s gains were small, but they were gains, nonetheless. I keep harping on the importance of liquidity as being “the driver” for further advances. Well, the Fed has pumped some $280 billion into the system over the past 7 weeks, which all but guarantees the momentum necessary to support the bullish theme.

Never mind that the October budget deficit surged 34% to $134 billion, which was its worst in five years. There is nothing but red ink in our future, but who cares about such minor details, if it stokes the liquidity engine.

Read More

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}