- Moving the markets

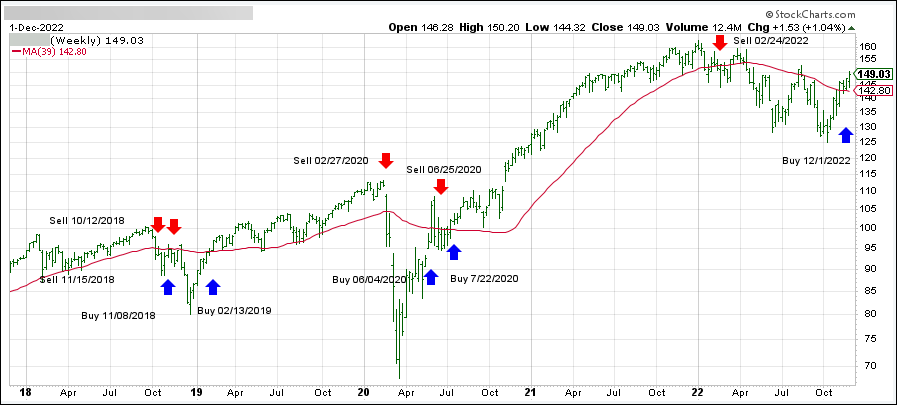

After last week’s rebound, that resulted in the S&P 500 finally breaking through its 200-day M/A, which has served as a glass ceiling since April, none of that feel good bullish sentiment was present today.

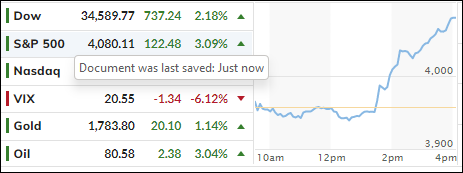

From the opening bell, the major indexes headed south caused by sudden fears that the Fed may not only not pivot but continue its hawkish policies, even as the economy slides further into recession territory.

That took the starch out of any remaining bullish momentum, as the broad market tumbled, including heavyweights like Tesla, Microsoft, and Amazon, with the retreat being broad based and leaving no place to hide.

Rising bond yields supported the equity bears, with the 10-year gaining 7 bps to close at 3.6%. The S&P “lost” its 200-day M/A again, which it had just reclaimed, bringing up the question whether conquering this resistance level was simply a head fake.

Fed whisperer Nick Timiraos appeared to walk back some of the market’s post-Powell exuberance, as ZeroHedge called it, in this morning’s WSJ article, as the “higher rates for longer” narrative was pushed, which caused terminal Fed rate expectations to surge.

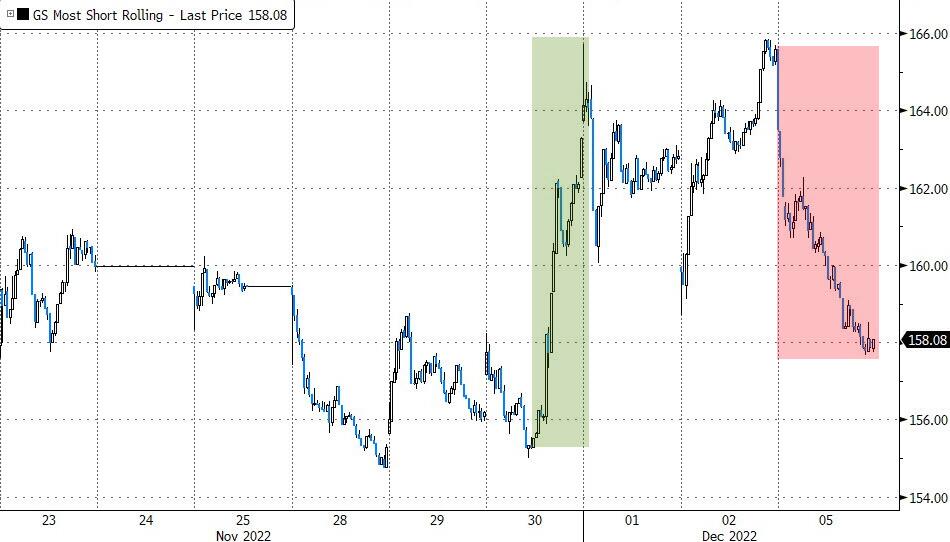

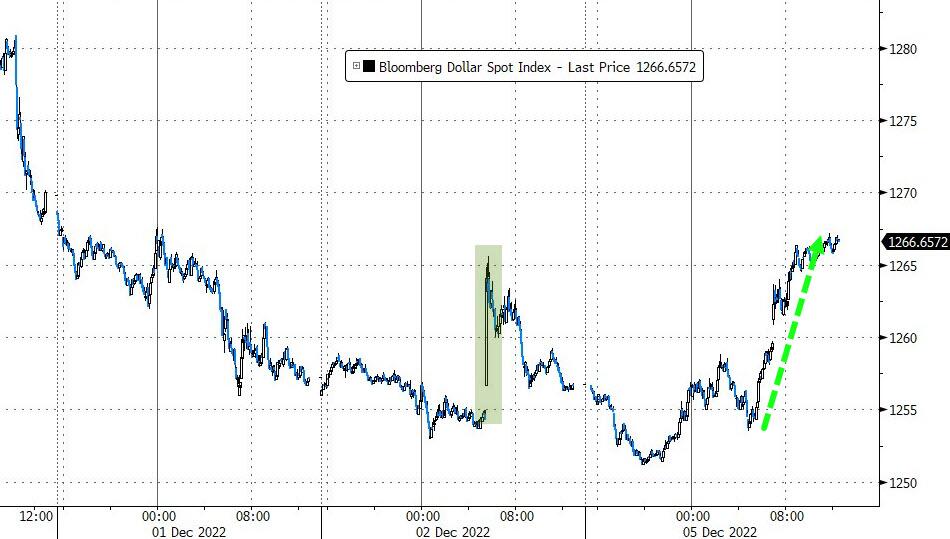

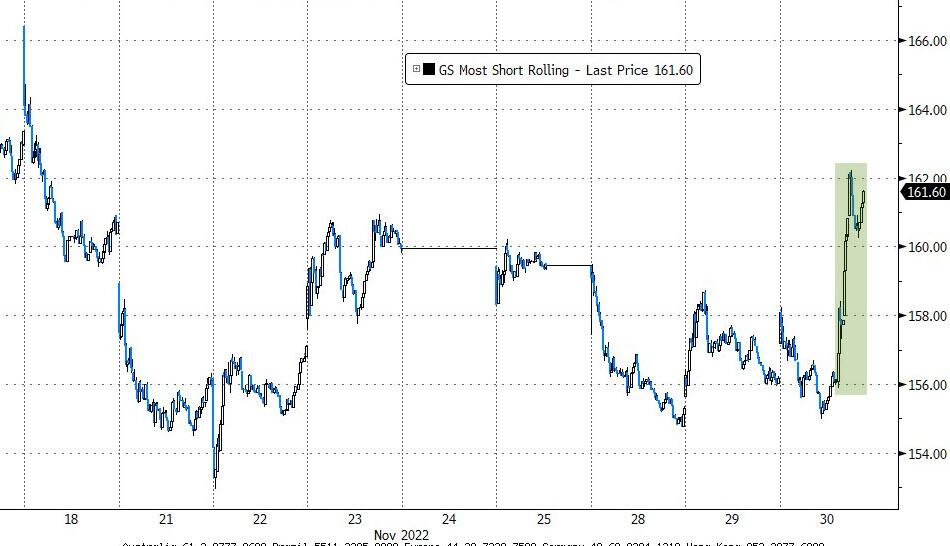

The stand-by and usually reliable bullish ammo failed today, because the most shorted stocks tanked as well, with no bailout squeeze attempt in sight. The US Dollar rebounded, and Gold dropped back below $1,800.

After a temporary bullish diversion, will the S&P 500 now sync up again with the 2008-2009 analog?

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}