- Moving the markets

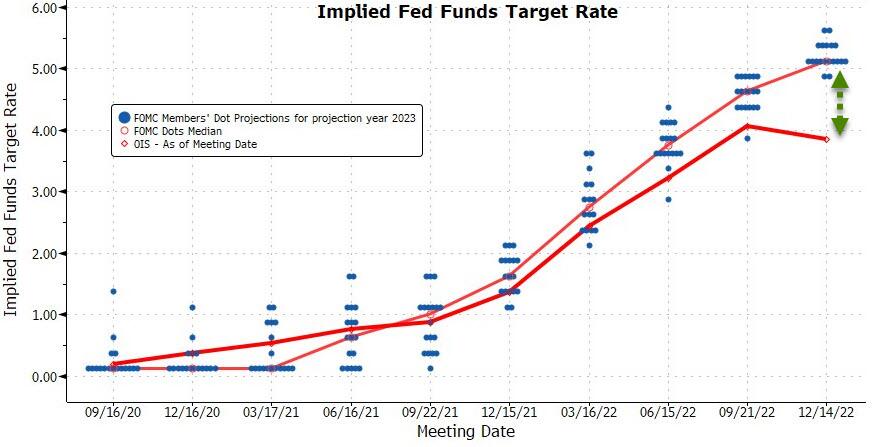

Even though the Fed hiked rates as expected, a “morning after” hangover set in, as today’s poor retail sales confirmed current recessionary tendencies. Sales dropped -0.6% in November, which was twice the expectations of a -0.3% decline.

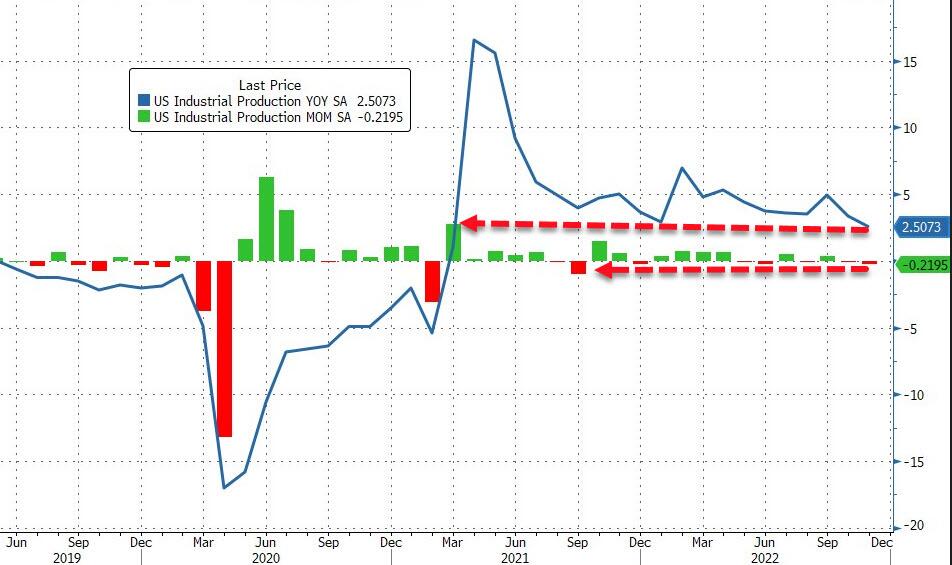

US Industrial Production did not help matters, because it fell 0.2% MoM (0% expected) and dropped to its weakest since September 2021, according to ZeroHedge.

Regarding the Fed’s stance on interest rates, analyst Peter Schiff summarized it best:

Now, that doesn’t mean the Fed shouldn’t be raising rates. They should be. They should have raised them a lot more than they have. The problem is they never should have cut them. That was the mistake — it was cutting rates. Raising them back up is really just an acknowledgment of that mistake. But what happens is when the Fed raises rates, it uncovers all of the problems that it created when it reduced rates. Because when it slashed interest rates to zero, it inflated a bubble economy, and it inflated it with inflation. Quantitative easing was inflation.

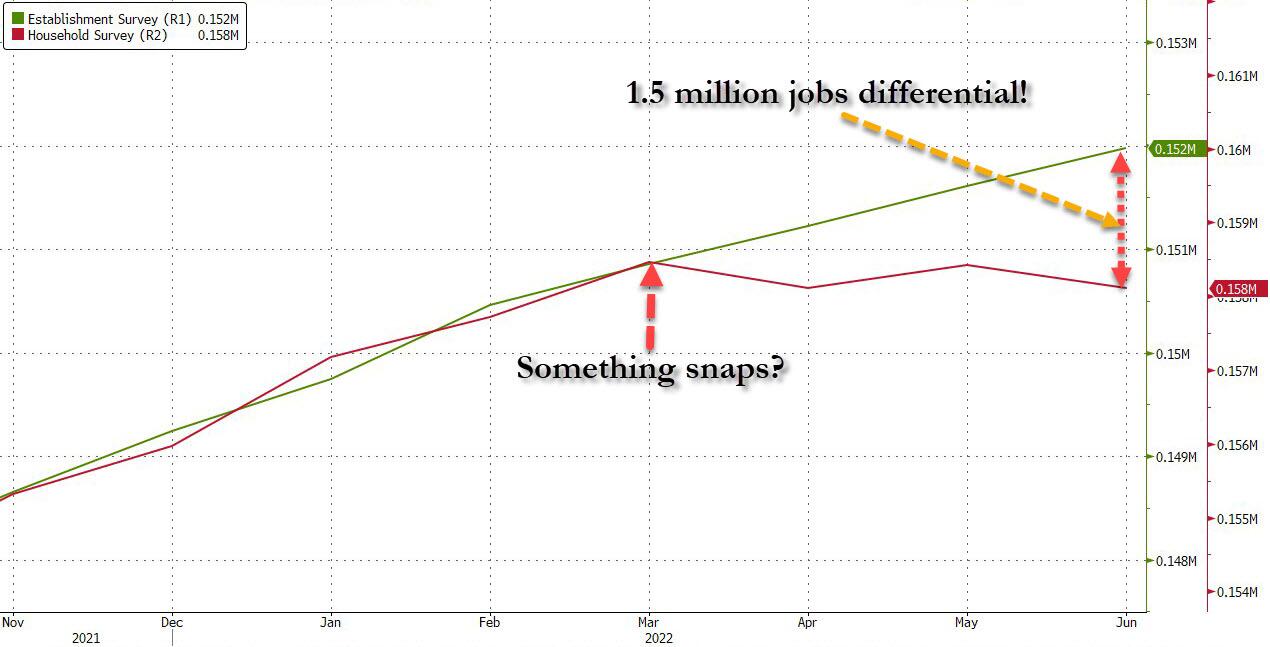

Then we learned that the Philadelphia Fed admitted that US Jobs were “overstated” by at least 1.1 million, a shocking story that you may want to read in detail, if this topic interests you.

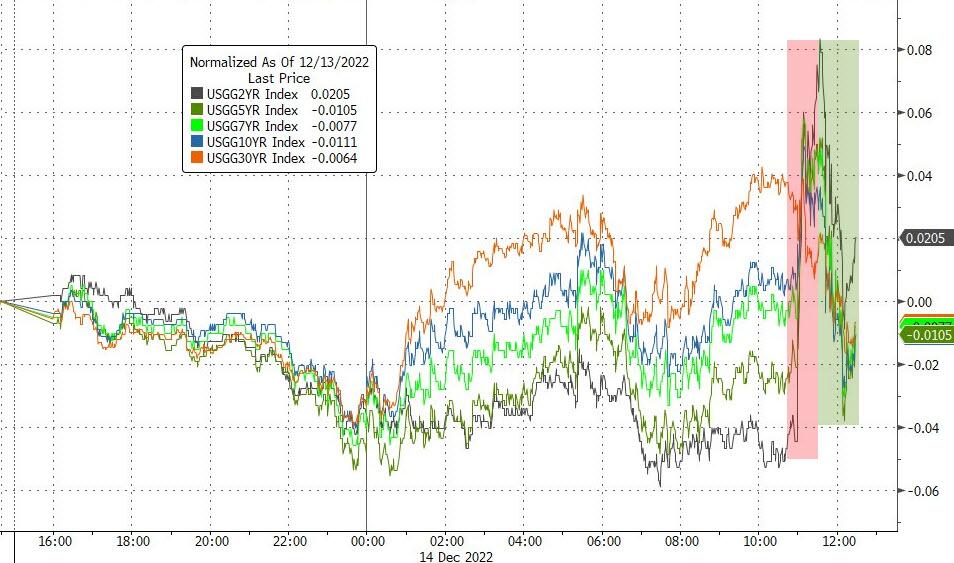

As a result, the major indexes were spanked and yet again, there was no place to hide. Our Trend Tracking Indexes (TTIs) were slammed as well but remained a tad above their respective trend lines.

We’re now facing the possibility that our recent “Buy” signal may turn out to have been a head fake, but it’s too early to tell. Tomorrow’s $4 trillion options expirations session may shed more light on where the major trend is headed into the end of the year.

Read More

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}