Do you want to know which ETFs are hot and which ones are not? Then you need my High-Volume ETF Cutline report. It tells you how close or far each of the 311 ETFs I follow is from its long-term trend line (39-week SMA). These are the ETFs that trade more than $5 million a day, so they are not some obscure funds that nobody cares about.

The report is split into two parts: The winners that are above their trend line (%M/A), and the losers that are below it. The yellow line is the line of shame that separates them. You can see how many ETFs are in each group and how they have changed since the last report (183 vs. 221 current).

MARKETS SHRUG OFF $4.2 TRILLION OPTIONS EXPIRY AND INFLATION DATA, BUT BEWARE OF AI BUBBLE

[Chart courtesy of MarketWatch.com]

Moving the markets

Today was a huge day for options traders, with $4.2 trillion worth of contracts expiring. But the markets didn’t seem too fazed by the massive turnover. They shrugged off some minor losses and held on to most of the gains they made this week. The S&P 500 rose by a respectable 2.7%. Gold and silver also bounced back from a rough start and rallied strongly in the last two days.

The markets got a boost from the CPI data, which matched expectations and eased some inflation fears. They also cheered the Fed’s decision to keep the rates unchanged, ignoring the warnings that the stimulus might taper sooner than later. The markets assumed that Powell was just bluffing and kept pushing higher.

But not everyone is convinced that this rally is sustainable or healthy. Some analysts warn that a recession is looming and that a bull market can’t last in such conditions. They also point out that the rally is driven by a narrow group of stocks in the artificial intelligence sector (AI), which reminds them of last year’s bubble that burst spectacularly.

One of them is BofA’s Michael Hartnett, who thinks that the S&P has more downside than upside potential between now and Labor Day. He thinks that the current situation is like a mix of 2000 and 2008, when a big rally was followed by a big crash. Only time will tell if he’s right.

On the bright side, consumer inflation expectations dropped sharply in June, which suggests that people are less worried about rising prices. But that doesn’t mean that everything is fine with the economy. It could also mean that people are pessimistic about their income and spending prospects.

Personally, I don’t put much stock in that indicator because I prefer to look at the actual prices I must pay for things. And those tell me a different story. They tell me that inflation is still alive and kicking.

Out of the 1,800+ ETFs out there, I only pick the ones that trade over $5 million per day (HV ETFs), so you don’t get stuck with a lemon that nobody wants to buy or sell.

Trend Tracking Indexes (TTIs)

These are the main indicators that tell you when to buy or sell Domestic and International ETFs (section 1 and 2). They do that by comparing their position to their long-term M/A (Moving Average). If they cross above, and stay there, it’s a green light to buy. If they fall below, and keep going, it’s a red light to sell. And to make sure you don’t lose your shirt if things go south, I also use a 12% trailing stop loss on all positions in these categories.

All other investment areas don’t have a TTI and should be traded based on the position of each ETF relative to its own trend line (%M/A). That’s why I call them “Selective Buy.” In other words, if an ETF goes above its own trend line, you can buy it. But don’t forget to use a trailing sell stop of 12%, or less if you’re feeling nervous.

If some of these words sound like Greek to you, please check out the Glossary of Terms and new subscriber information in section 9.

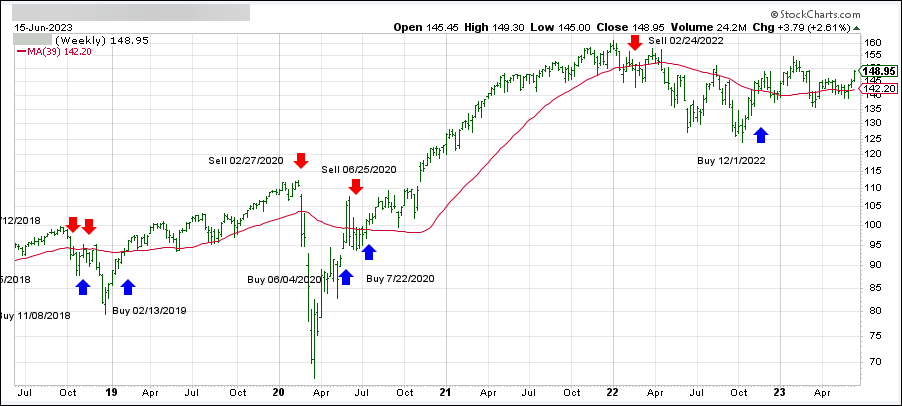

DOMESTIC EQUITY ETFs: BUY— since 12/01/2022

Click on chart to enlarge

This is our main compass, the Domestic Trend Tracking Index (TTI-green line in the above chart). It has now broken above its long-term trend line (red) by +4.98% and remains in “Buy” mode.

The stock market had a surprising comeback today, despite the gloomy outlook from the Fed and the ECB. Both central banks signaled more interest rate hikes this year, which usually dampens investors’ mood.

But traders seem to think that Powell is bluffing and won’t tighten the monetary policy too much. They are betting on a bullish market, ignoring the economic reality.

The futures markets were down last night, but the mood changed at the opening bell. The major indexes rallied all day and closed with solid gains. The economic data was mixed: jobless claims were higher than expected, but retail sales rose slightly. A short squeeze helped to boost market sentiment as well.

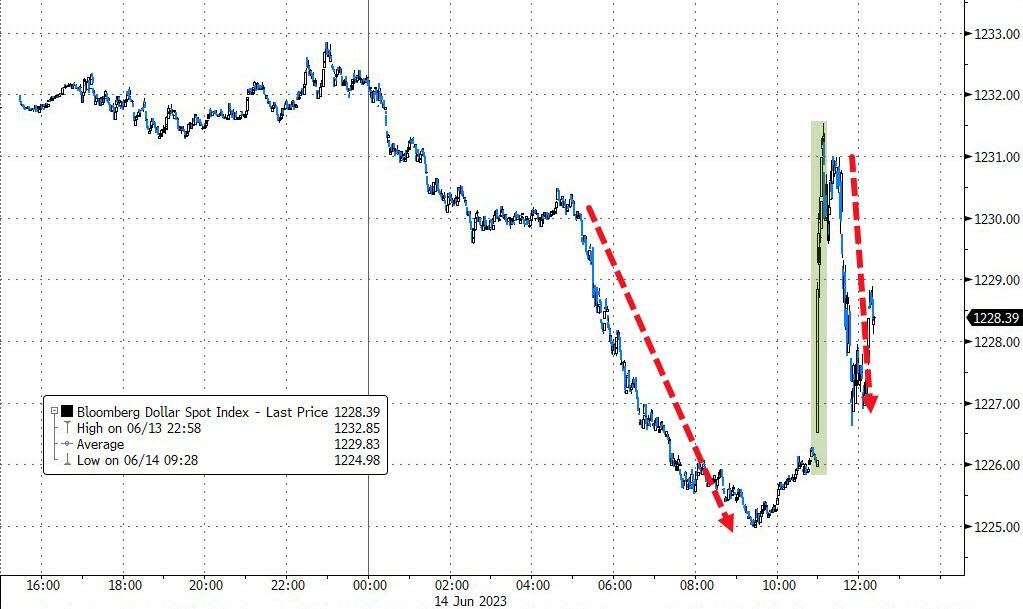

Bond yields fell after an initial spike, which dragged the dollar down to its lowest level in six weeks. Gold benefited from the weaker dollar and recovered some of its losses.

The market’s performance so far this month defies historical patterns. June is usually a weak month for stocks, especially for the Dow and the S&P 500. But this time, traders and algos are challenging the conventional wisdom and betting against the Fed.

The Fed decided to hold off on raising interest rates this month, despite signs of inflation in the economy. This was good news for traders who were hoping for a pause in the Fed’s tightening cycle. But it also raised some questions about the Fed’s credibility and its ability to fight inflation in the future.

The market got a hint of the Fed’s decision earlier in the day when the Producer Price Index (PPI) came in lower than expected. The PPI measures the change in prices of goods and services sold by producers. It fell by 0.3% in May, compared to a forecast of a 0.1% drop. This brought the annual PPI down to 1.1%, the lowest since December 2020.

This suggested that inflation pressures were easing, or at least not as bad as feared. Traders took this as a sign that the Fed would not hike rates this month, but rather wait and see how the economy evolves. They were right.

In its statement, the Fed said that it would keep its benchmark rate in the 5%-5.25% range, and that any further rate hikes would depend on the economic data. It also added a new sentence, saying that holding rates steady would allow it to assess more information and its implications for monetary policy.

The Fed also said that it was prepared to adjust its policy stance if risks emerged that could impede its goals of price stability and maximum employment. This was a subtle way of saying that it could cut rates if inflation fell too low or if the economy slowed down significantly.

The Fed’s message was clear: it was not done with hiking rates, but it was not in a hurry either. It was taking a “hawkish pause”, as ZeroHedge put it.

However, not everyone was convinced by the Fed’s logic. Some analysts pointed out that the Fed was ignoring other indicators of inflation, such as consumer prices, wages, and oil prices. They also noted that the Fed was losing credibility by changing its tone from a “dovish hike” in May to a “hawkish pause” in June.

The market reaction was mixed. Stocks initially sold off, but then recovered and ended near flat. Gold also dipped, but then bounced back. Bonds and the dollar fell and stayed low. The Nasdaq was the best performer among the major indexes, as tech stocks benefited from lower interest rates.

This chart shows the divergence between the Nasdaq and the financial conditions index, which measures how easy or hard it is to borrow money in the market. The index has been rising, indicating tighter financial conditions, while the Nasdaq has been soaring, indicating optimism.

This disconnect suggests that either the Nasdaq is too optimistic, or the financial conditions index is too pessimistic. Either way, something has to give.

The market will be watching closely how the economy performs in the coming months, and how the Fed responds to new data. Will inflation prove to be transitory or persistent? Will growth remain strong or falter? Will the Fed stick to its pause or resume its hikes?

These are the questions that will determine the direction of the market in the second half of 2023.

The CPI, which measures the average change in prices of consumer goods and services, rose by 4% in May compared to a year ago. That was the lowest annual increase since March 2021, and in line with what economists had predicted. But the Core CPI, which excludes food and energy prices and is the Fed’s preferred gauge of inflation, jumped by 5.3% over the same period. That was a tad higher than expected but still the lowest rise since November 2021.

You might be wondering how these numbers are calculated, because if you go shopping for anything these days, you’ll notice that prices have gone up much more than these percentages. And to make matters worse, inflation has been growing faster than wages for the last 26 months, which means your purchasing power is shrinking.

The stock market, however, seemed to like these numbers, and the major indexes closed higher. Investors are betting that the Fed will not raise interest rates too soon or too fast, even though inflation is running hot. Some traders think the Fed might skip a rate hike in June, when it announces its policy decision tomorrow.

But not everyone agrees on what the Fed should do. As ZeroHedge summarized this morning, there are different narratives based on different aspects of the inflation data:

• Headline CPI fell (yay, Fed can relax!).

• Goods inflation rose (Fed can pause as services prices slowed down).

• Core CPI was higher than expected and still high (Fed can’t stop, but maybe skip a hike!).

• SuperCore, which excludes volatile items like food, energy, shelter, and medical care, accelerated (Fed should keep hiking!).

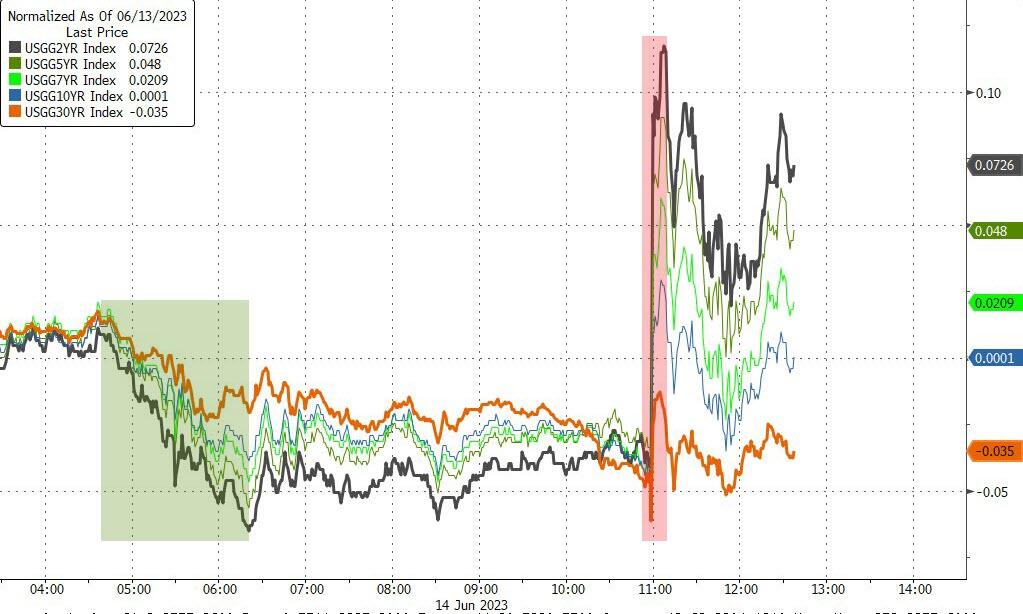

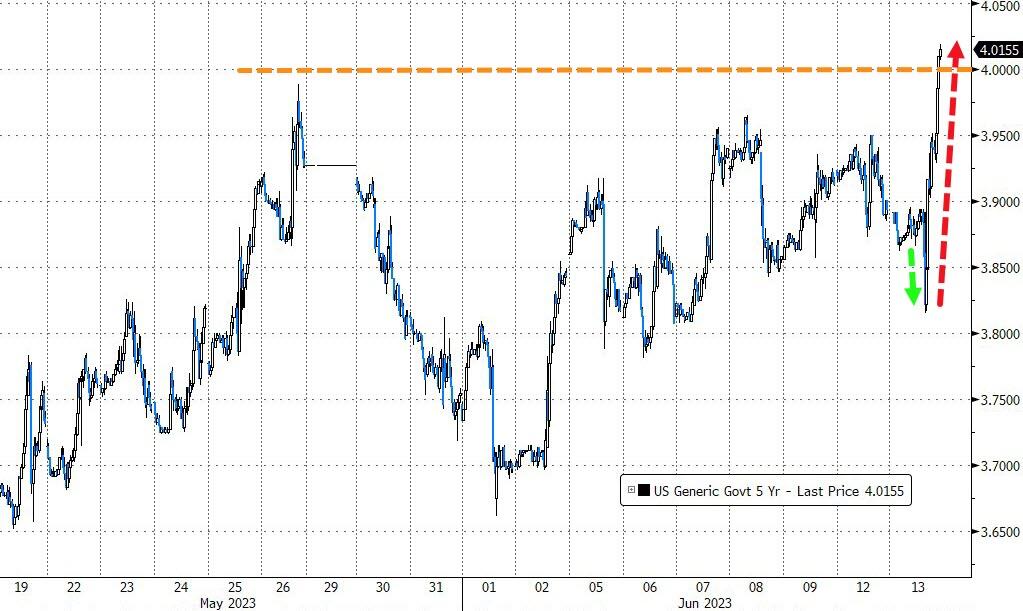

The bond market also reacted to the inflation data. After an initial drop, bond yields rose sharply, with the 2-year yield reaching 4% for the first time since March 10th. The dollar, on the other hand, fell after Treasury Secretary Yellen said she “expects a gradual decline in the dollar’s role as a reserve currency.” Ouch.

Gold also had a wild ride. It surged early on, but then plunged as bond yields went up. Remember, gold and interest rates tend to move in opposite directions.

All eyes are now on the Fed’s meeting tomorrow. Will they signal a change in their stance on inflation and interest rates? The Bespoke Investment Group showed this chart of how the S&P 500 performed after the last six Fed meetings.

Will history repeat itself, or will it be different this time?

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}