- Moving the markets

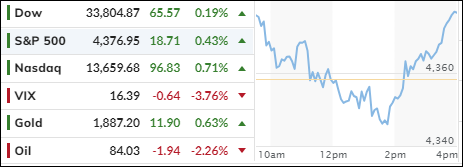

U.S. stocks ended lower on Thursday, snapping a four-day winning streak, as investors digested the latest inflation data and a dismal bond auction.

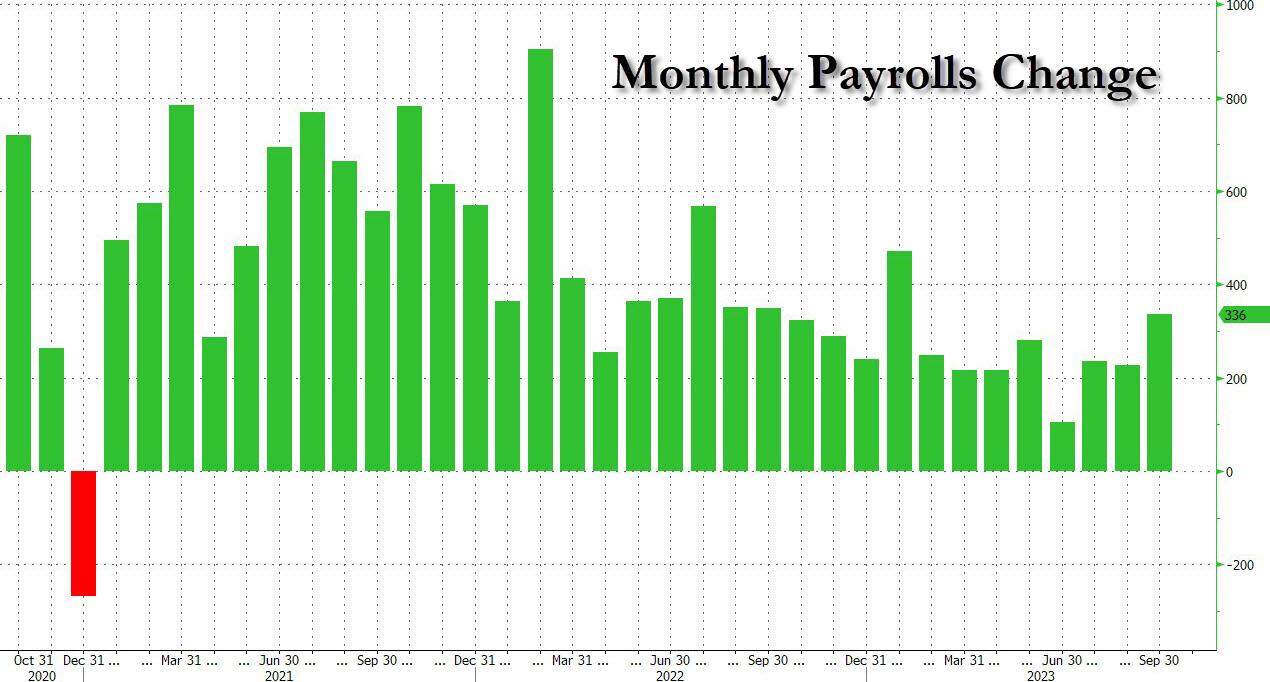

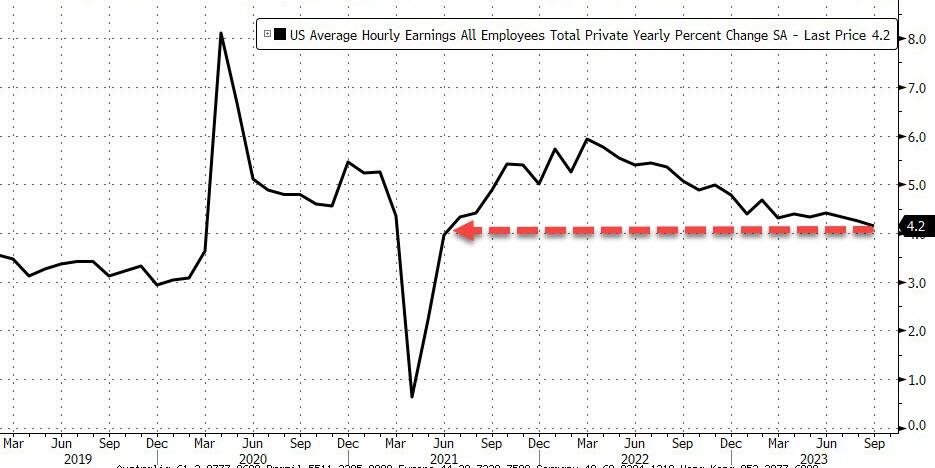

The consumer price index (CPI), a key measure of inflation, rose by 0.4% in September and 3.7% year-over-year, beating the consensus estimates of 0.3% and 3.6%, respectively.

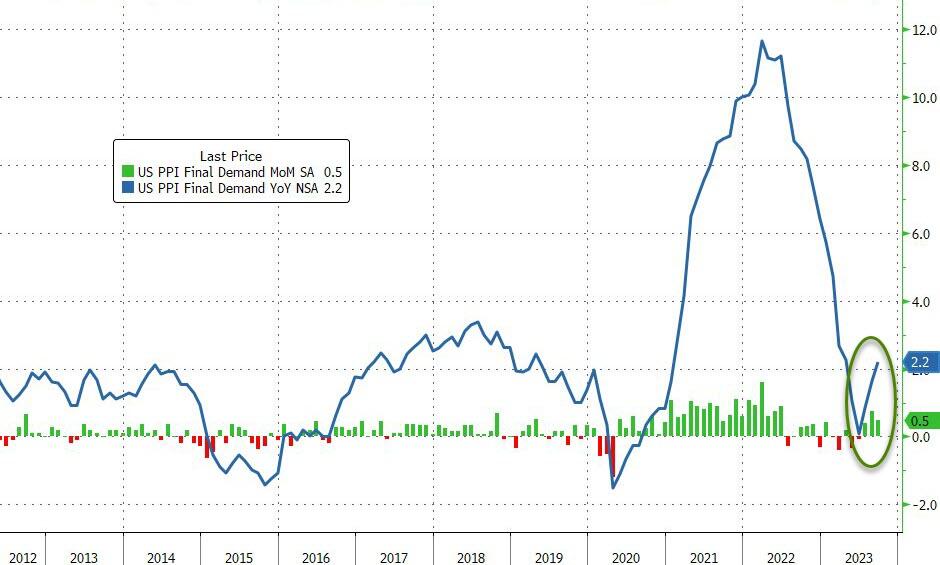

The core CPI, which excludes volatile food and energy prices, matched the expectations of 0.3% monthly and 4.1% annual increases. The inflation data followed a stronger-than-expected producer price index for September, which showed a stronger-than-expected producer price index for September.

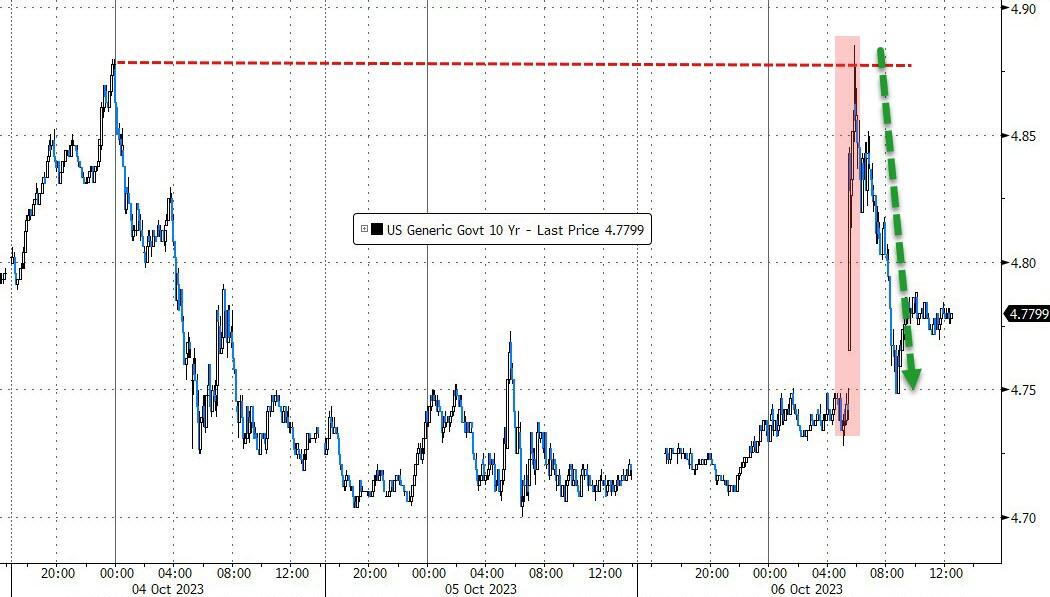

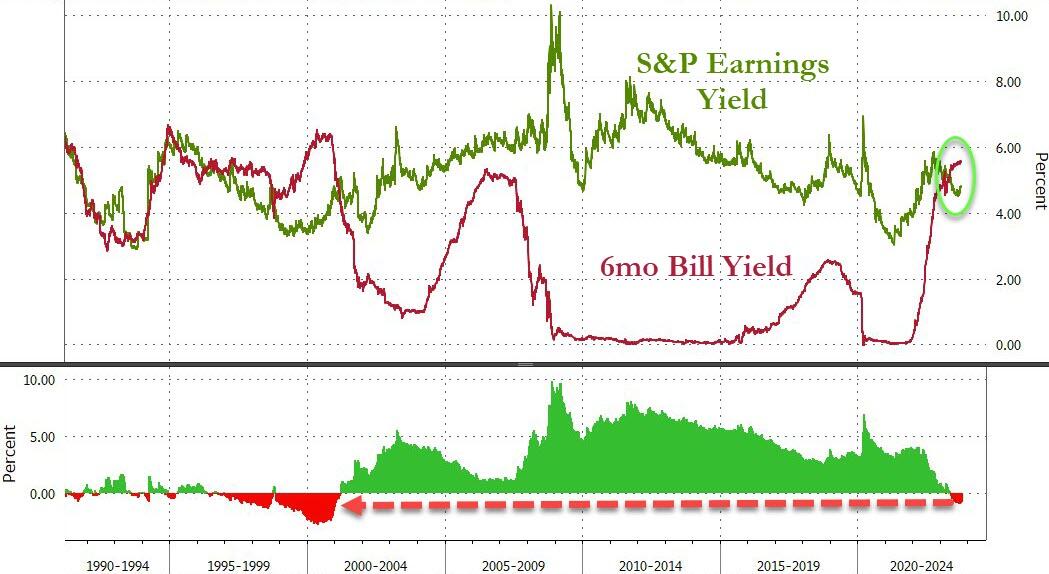

The inflation numbers spooked the bond market, sending the yields on the 10-year Treasury note soaring by more than 14 basis points to 4.705%, near its intraday high. The catalyst for the yield spike was a terrible 30-year bond auction, which had the highest yield since 2011.

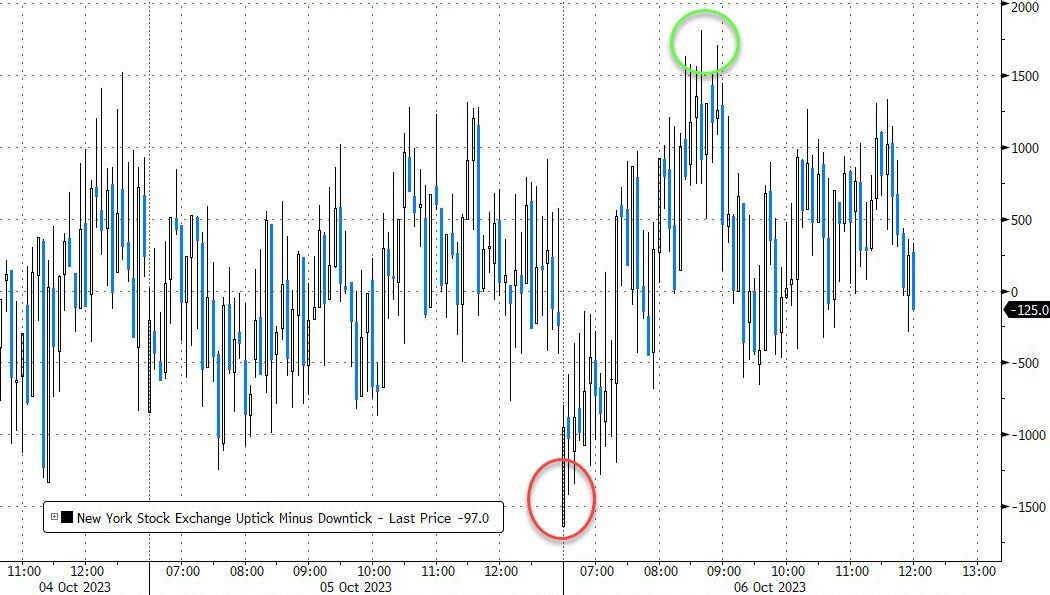

The bond market rout dragged down the stock market, as higher yields make equities less attractive and raise borrowing costs for companies and consumers.

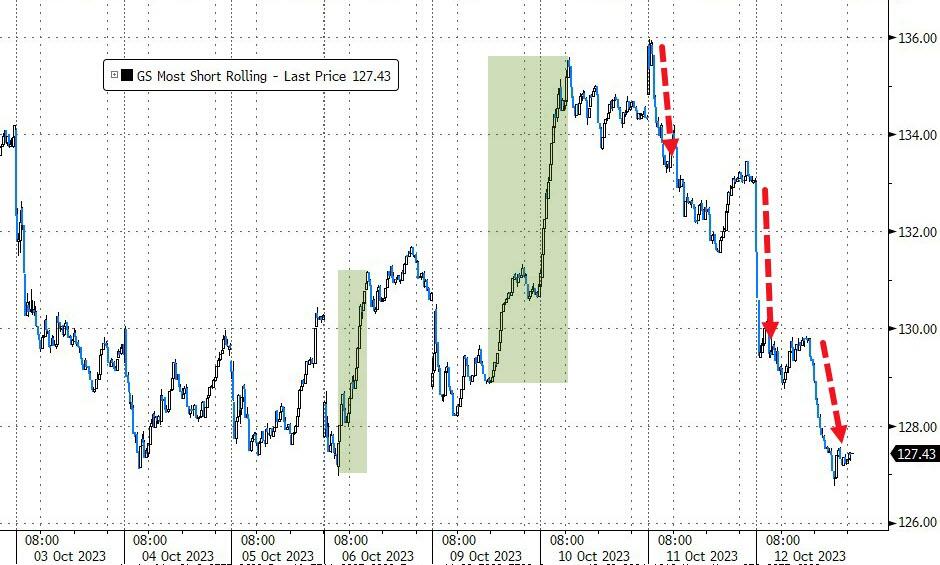

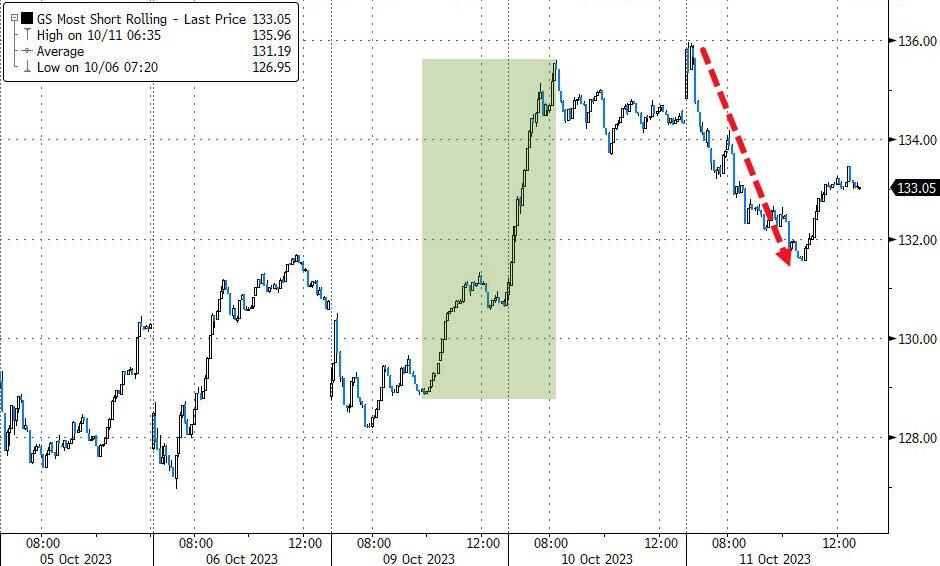

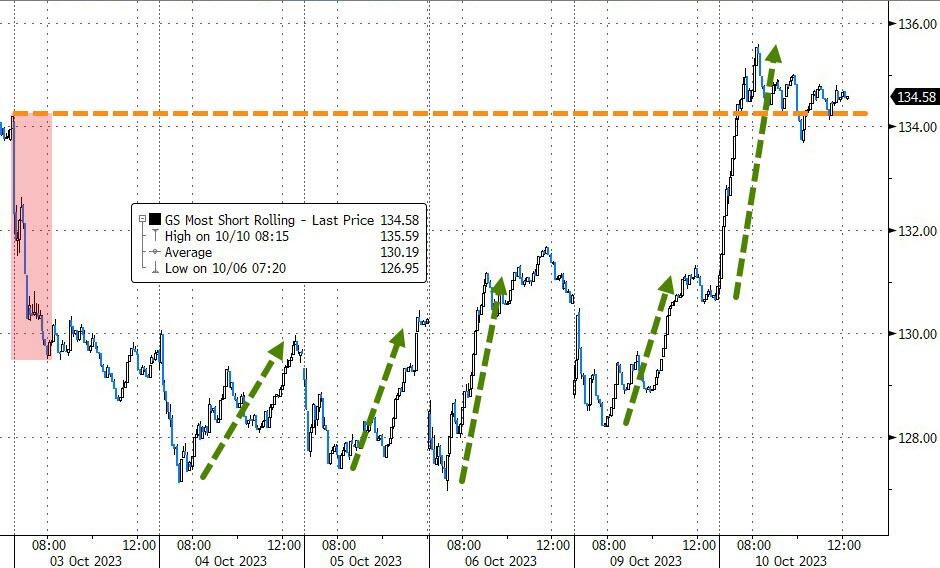

The sell-off was broad-based, but especially hit the most shorted stocks, which plunged and erased their gains for the year.

Crude oil prices were flat, despite the ongoing conflict between Israel and Hamas, which raised fears of a supply disruption in the Middle East.

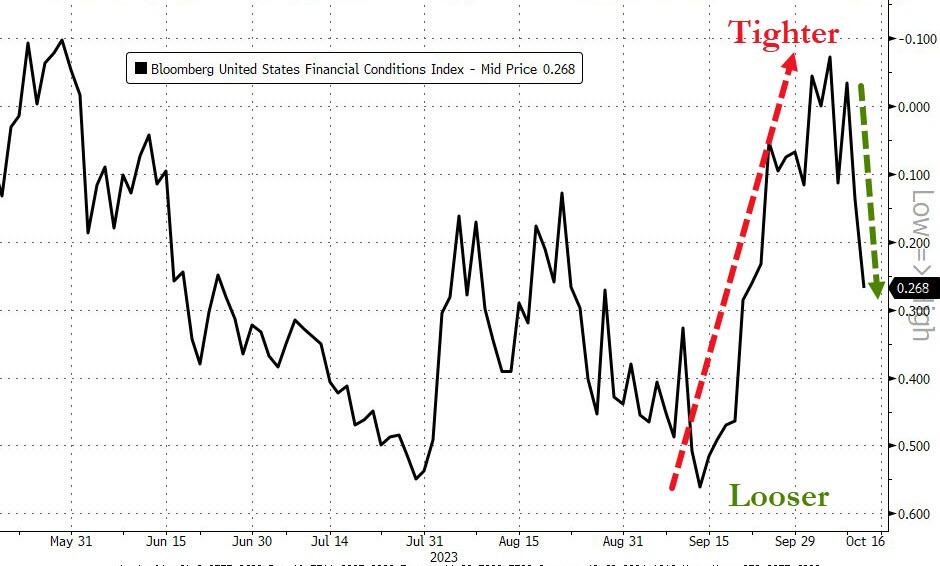

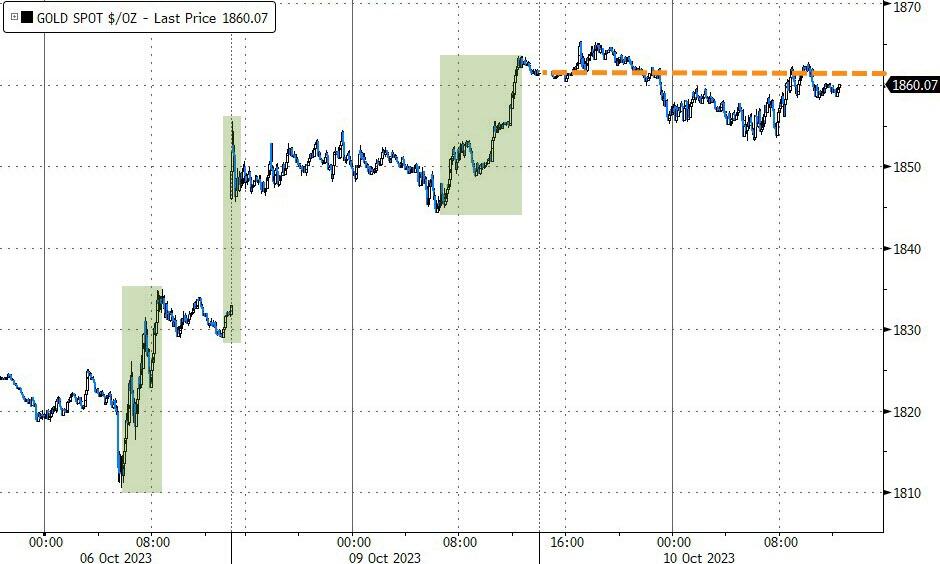

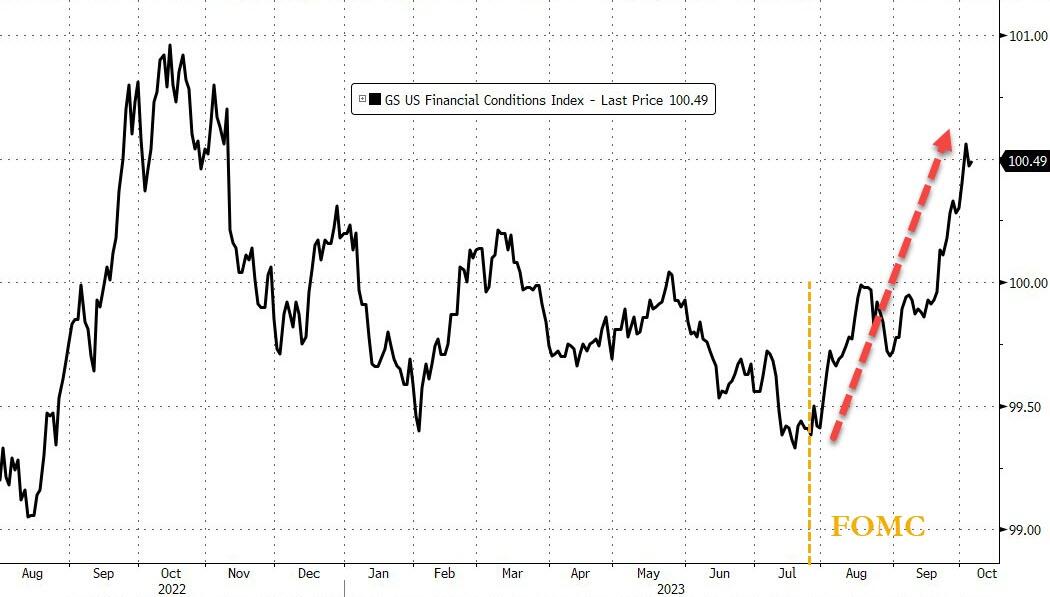

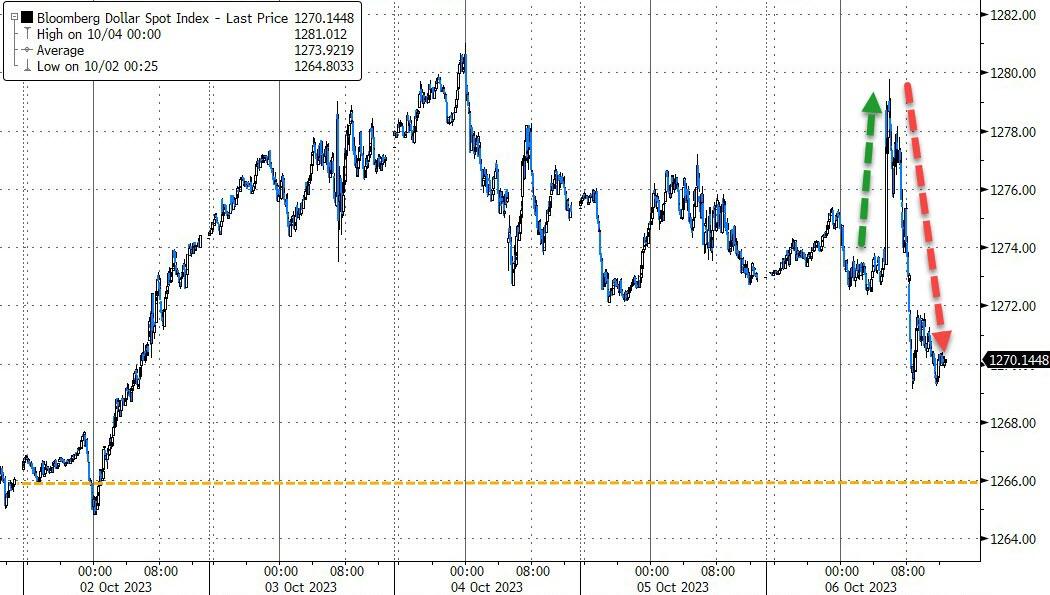

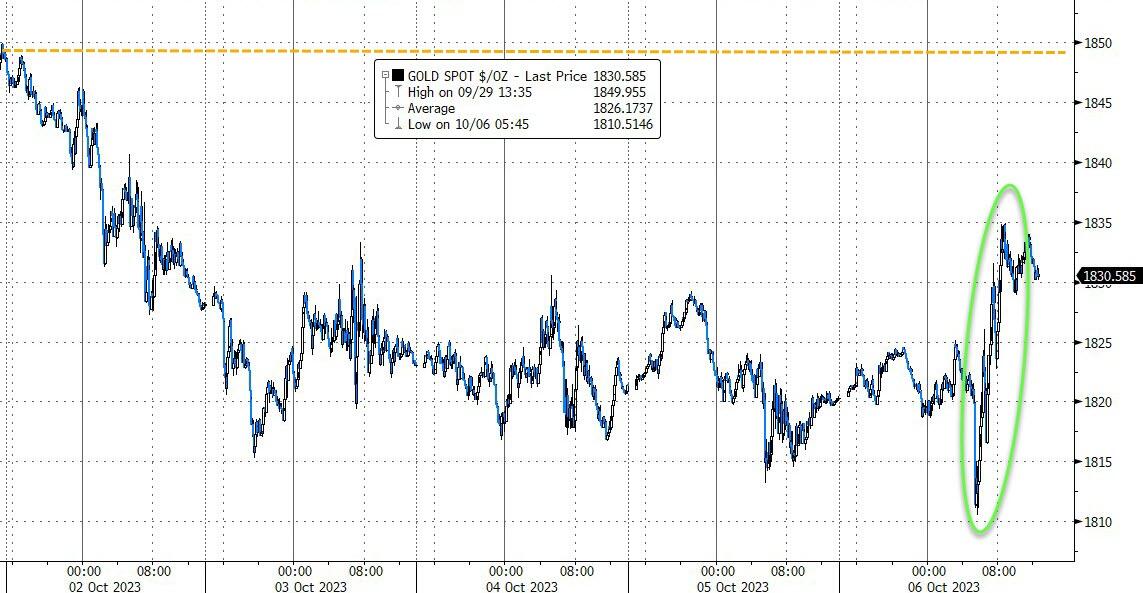

The dollar rallied on the back of rising yields, while gold prices gave up their earlier gains. Financial conditions eased, despite the Fed’s recent announcement that it was happy with the market’s tightening response.

Will the Fed change its course if inflation persists, and bond yields continue to surge? How will the stock market react to the Fed’s next move? These are the questions that traders will be asking themselves in the coming days.

Read More

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}