Do you want to know which ETFs are hot and which ones are not? Then you need my High-Volume ETF Cutline report. It tells you how close or far each of the 311 ETFs I follow is from its long-term trend line (39-week SMA). These are the ETFs that trade more than $5 million a day, so they are not some obscure funds that nobody cares about.

The report is split into two parts: The winners that are above their trend line (%M/A), and the losers that are below it. The yellow line is the line of shame that separates them. You can see how many ETFs are in each group and how they have changed since the last report (36 vs. 98 current).

JOBS REPORT FLOP, BOND YIELD DROP, STOCK MARKET POP: IS THIS A NEW BULL MARKET?

[Chart courtesy of MarketWatch.com]

Moving the markets

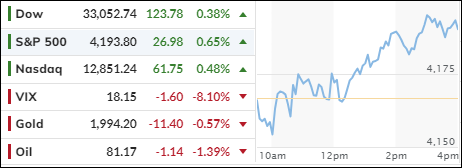

The stock market had a blast last week, despite a dismal jobs report that sent bond yields and the dollar plunging. Investors cheered the alleged end of the Fed’s rate hikes and squeezed the bears out of their positions. The major indexes posted their best weekly performance since November 2022, thanks to the largest short squeeze in 12 months.

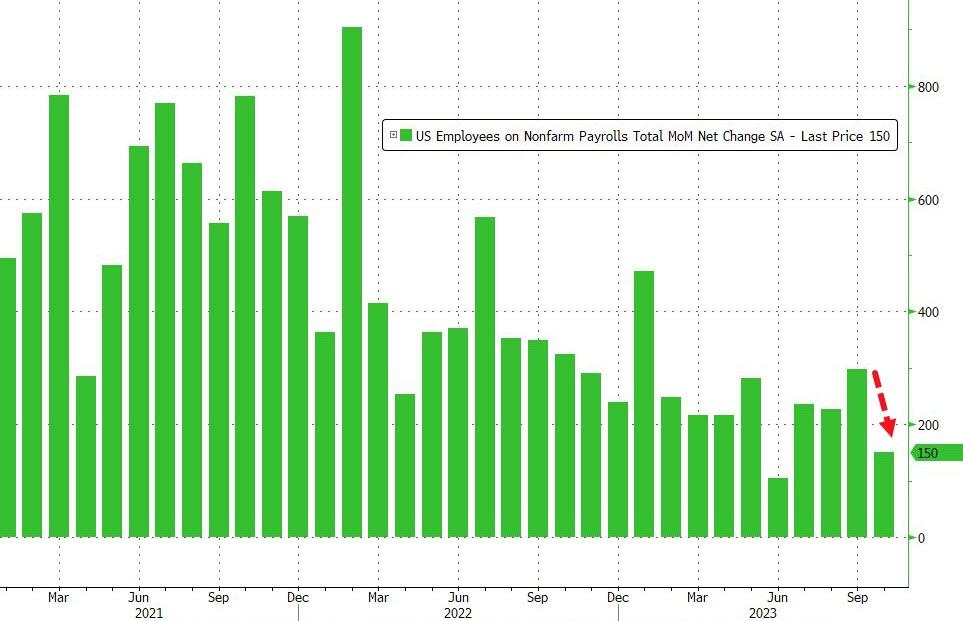

The October jobs report was a shocker, as the economy added only 150k jobs, less than half of the September figure. And that’s not all, the previous two months were revised down by a whopping 101k jobs. That makes it eight months in a row of downward revisions. Something fishy is going on here…

But the markets don’t care about facts, they care about expectations. And the expectations are that the Fed will be more dovish and less hawkish in the face of weak jobs and wage growth. That’s why stocks and bonds rallied, while the dollar tanked.

Lower bond yields and inflation worries also helped the equity market, which still shows signs of a healthy labor market that is creating more jobs than the break-even rate of 100k. The 10-year Treasury yield dropped by 14 basis points to 4.52%, well below the 5% peak it reached last month.

Apple was one of the few losers, as it fell 1.5% after giving disappointing revenue guidance for the December quarter. The tech giant beat the earnings estimates for the fourth quarter, but its sales declined for the fourth consecutive quarter. However, this did not have a major impact on the overall market sentiment.

Lower bond yields, a weaker dollar, and the improved financial conditions should have boosted the oil and gold prices, but surprisingly, they did not. Oil prices dropped, while gold stayed around its $2k level.

After a five-day rally, the S&P 500 recovered all its losses since our last “Sell” signal, and our TTIs are close to triggering a new “Buy” signal (section 3). But the question is:

Are we witnessing a genuine bull market or a fake-out breakout?

ETF Data updated through Thursday, November 2, 2023

How to use this StatSheet:

Out of the 1,800+ ETFs out there, I only pick the ones that trade over $5 million per day (HV ETFs), so you don’t get stuck with a lemon that nobody wants to buy or sell.

Trend Tracking Indexes (TTIs)

These are the main indicators that tell you when to buy or sell Domestic and International ETFs (section 1 and 2). They do that by comparing their position to their long-term M/A (Moving Average). If they cross above, and stay there, it’s a green light to buy. If they fall below, and keep going, it’s a red light to sell. And to make sure you don’t lose your shirt if things go south, I also use a 12% trailing stop loss on all positions in these categories.

All other investment areas don’t have a TTI and should be traded based on the position of each ETF relative to its own trend line (%M/A). That’s why I call them “Selective Buy.” In other words, if an ETF goes above its own trend line, you can buy it. But don’t forget to use a trailing sell stop of 12%, or less if you’re feeling nervous.

If some of these words sound like Greek to you, please check out the Glossary of Terms and new subscriber information in section 9.

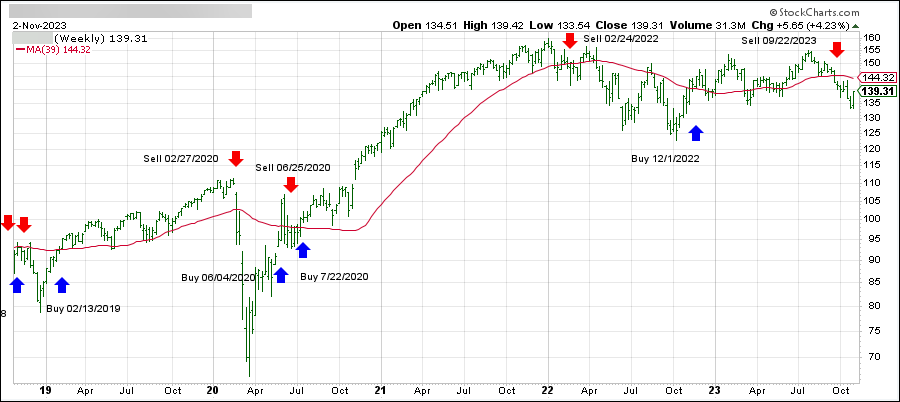

DOMESTIC EQUITY ETFs: SELL— since 09/22/2023

Click on chart to enlarge

This is our main compass, the Domestic Trend Tracking Index (TTI-green line in the above chart). It has now broken below its long-term trend line (red) by -3.67% and has moved into “Sell” mode effectively 9/22/2023.

The stock market bulls were in full force today, as they shrugged off the Fed’s hawkish hints and drove the indexes higher for the fourth day in a row. They were betting that the central bank had finished raising interest rates for 2023, after seeing some signs of easing inflation in the latest data.

The rally was broad and strong, with all 11 sectors of the S&P 500 and the equally weighted index joining the party. The tech sector was not the only star of the show, as some of the most beaten-down sectors like energy and financials also bounced back thanks to a short squeeze assist.

The bond market also rallied, sending the 10-year Treasury yield down to 4.669%, after it had spiked above 5% last month.

However, not everything was rosy in the market, as some earnings disappointments dragged down some individual stocks. Moderna shares plunged 10% after reporting a huge third-quarter loss, while SolarEdge dropped 15% after missing expectations and lowering its outlook. These results reminded investors that the pandemic was not over yet, and that some sectors were still struggling to cope with the challenges.

Some analysts were also skeptical about the sustainability of the rally, pointing out that the Fed had not ruled out a rate hike in December, and that inflation was still a major threat to the economy. They argued that Wall Street was too optimistic about the Fed’s dovish stance, and that the market would be setting itself up for a rude awakening if the central bank changed its mind.

My view is that this rally was just a rebound from a very oversold condition, and that it had not produced any new gains for buy-and-hold investors.

In fact, the S&P 500 was still higher on September 22, when our Trend Tracking Index signaled a “Sell,” than at today’s close. As trend followers, we are still ahead of the game, and we will wait for another buy signal before re-entering the market.

So, is this rally a real recovery or just a bear market trap? Will the Fed surprise us with a rate hike in December or stay on hold? Will inflation cool down or heat up again? And most importantly, will Santa Claus bring us a gift or a lump of coal this year?

These are some of the questions that are on my mind.

Stocks rallied on Wednesday, bouncing back from a dismal past three months, after the Federal Reserve kept interest rates unchanged for a second consecutive time.

This led traders and algorithms to believe that the central bank would stay put for the rest of the year.

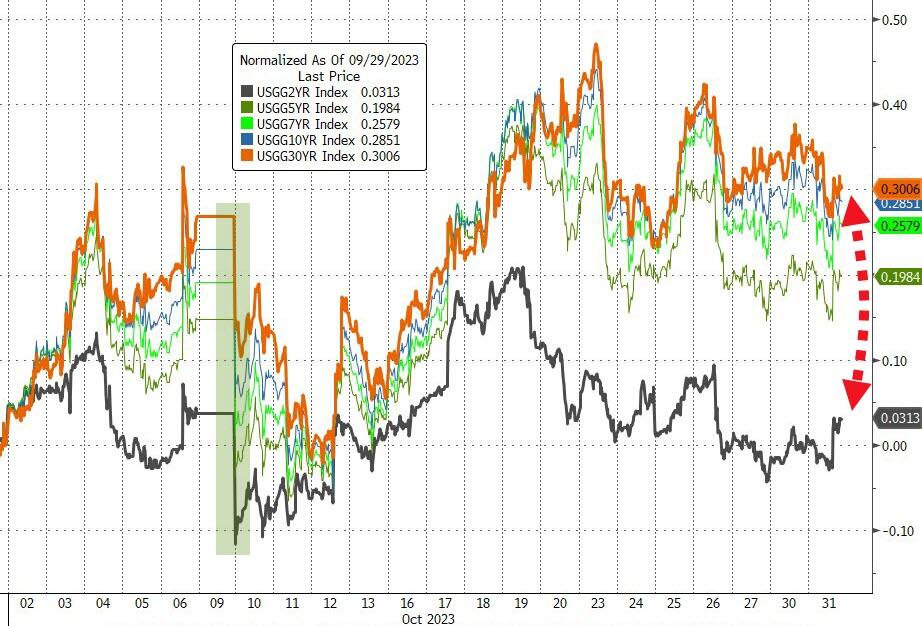

The Treasury detailed plans of the size of its future bond sales amid growing concerns of the U.S. government’s rising debt load. It appeared to be in line with what traders were expecting, with the Treasury auctioning $112 billion in debt the next week, largely matching what Wall Street was anticipating.

The 10-year Treasury yield slipped slightly after the Treasury announcement and closed down 17 basis points to end the session at 4.757%, thereby increasing its distance to the much-feared 5% level.

The Fed kept rates in a range of 5.25% to 5.5%, as was widely expected. The central bank also said that “economic activity expanded at a strong pace in the third quarter.” In previous remarks, it noted that the economy was growing at a “solid pace.”

It seems that, given the recent rise in yields, the Fed is less likely to raise rates in December, with the possibility of raising them later to keep reducing inflation, as tighter financial conditions since the September FOMC meeting have already partially achieved the Fed’s goals.

However, Fed Chair Jerome Powell at the post-decision press conference would not rule out a hike next month, saying that the idea that it would be difficult to raise rates after pausing for two meetings was wrong. Powell didn’t help early on in his press conference with some hawkish-sounding comments:

• *POWELL: PROCESS OF GETTING INF. TO 2% HAS LONG WAY TO GO

• *POWELL: FULL EFFECTS OF TIGHTENING YET TO BE FELT

• *POWELL: NOT CONFIDENT WE’VE REACHED STANCE FOR 2% INFLATION

Traders were not deterred by Powell’s hawkish tones and instead savored the fact that rates remained unchanged, which appeared to be reason enough to drive equities higher. In other words, the market only had eyes and ears for dovish thoughts and stocks ripped higher during Powell’s speech, with Nasdaq leading the charge and Small Caps rebounding into the green.

Hedge fund guru Stan Druckenmiller made the prescient observation that “bonds are adjusting to a post-QE world, but for some reason equities haven’t.” This chart makes his view abundantly clear:

The S&P 500 managed to end the day in the green, but it was not enough to save the month from being a disaster.

Treasury yields soared to levels not seen since 2007, making bonds look more attractive than stocks.

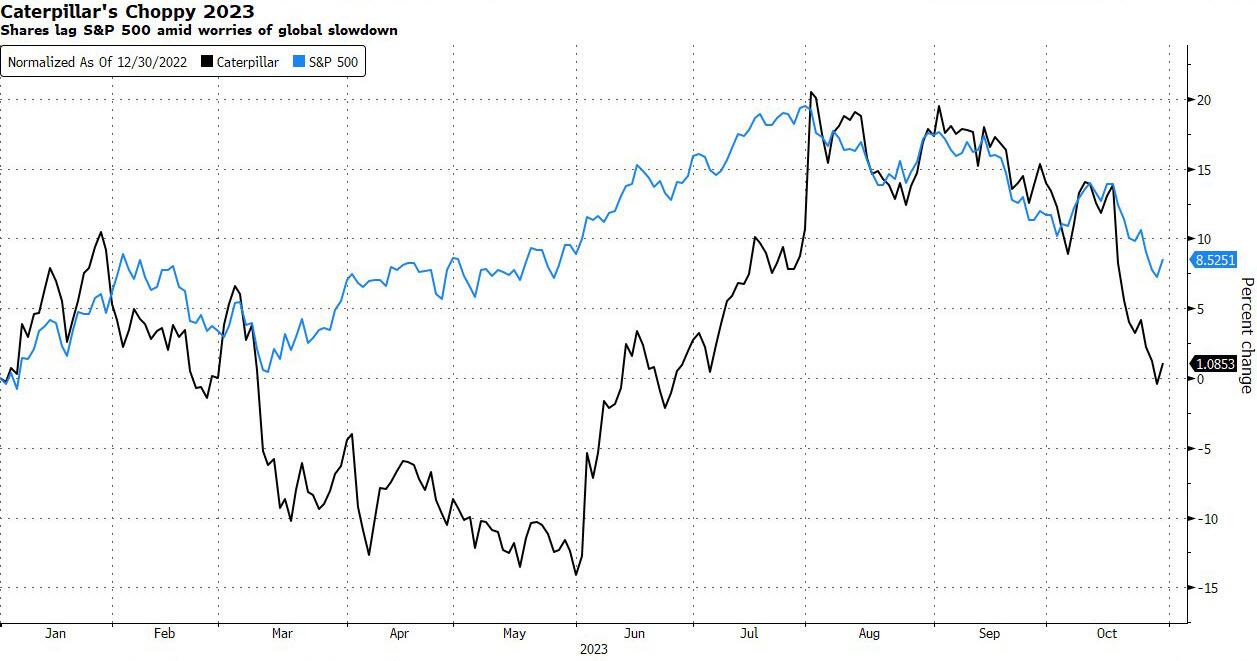

Caterpillar, the maker of heavy machinery, beat earnings expectations for the third quarter, but warned that its fourth-quarter revenue would be only slightly better than last year. Investors were not impressed and dumped the stock, sending it down more than 5%.

The major indexes suffered their third consecutive monthly loss, something that has not happened since the pandemic hit in March 2020. The Dow and the S&P 500 lost about 2.2% and 3%, respectively, while the Nasdaq dropped more than 3%.

The tech sector was hit hard by rising interest rates, which hurt the valuations of growth stocks. But the biggest loser of the month was the Small Caps index, which plunged over 7% in October, marking its third straight negative month and its worst performance since September 2022.

Wall Street is now waiting for the Fed to announce its interest rate decision on Wednesday. The market is almost certain that the Fed will keep rates unchanged, but it is also looking for clues about its future plans. Will they hint at more rate hikes, or will they be more cautious?

Traders are also hoping for some good news from the October payrolls report, which will be released on Friday. They hope that the labor market will show some signs of cooling down, which could ease the pressure on the Fed to tighten monetary policy. But is that wishful thinking?

ZeroHedge summed up the latest data points like this:

Today saw wage inflation rising faster than hoped (hawkish for Fed) and consumer confidence worsened (with inflation expectations jumping).

Not exactly a great way to end the month.

But, as Financial Conditions tightened for the 3rd straight month in October, they failed to spook the economy…

Bond yields moved in different directions in October, with the long bond rising over 30 basis points, but the short bond staying flat.

The dollar gained strength for the third month in a row, thanks to higher bond yields. Gold had its best month since March, but it failed to stay above its $2k level and slipped slightly today.

The markets are still overpriced compared to GDP and history is not on their side. This chart shows how the current level of the 1923 Dow compares to its 1987 and 1928 performance.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}