With the markets having been on a tear since Labor Day, our Domestic Trend Tracking Index (TTI) has advanced at a very steep angle. The reason for that is that this indicator includes an interest rate sensitive component, which has, due to lower rates, exaggerated the slope.

With the markets having been on a tear since Labor Day, our Domestic Trend Tracking Index (TTI) has advanced at a very steep angle. The reason for that is that this indicator includes an interest rate sensitive component, which has, due to lower rates, exaggerated the slope.

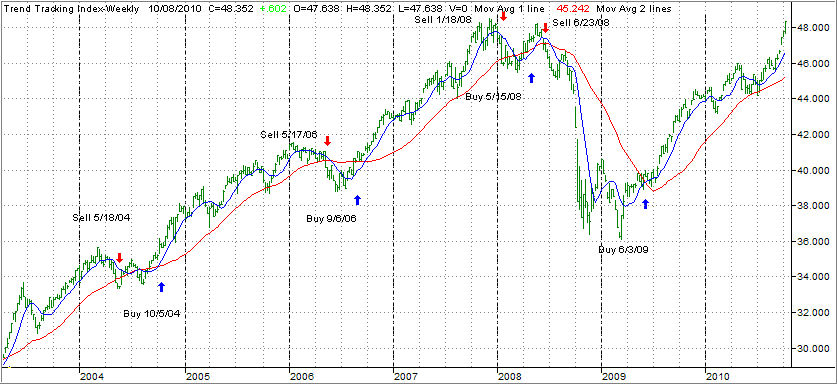

Let’s take a look at an enlarged portion of the TTI to the left.

Upward momentum caused a break-away gap in the chart (see arrow) recently, which means that the previous week’s high was lower than the next week’s low. As I have written before, these gaps will always be “closed” eventually when prices decline again to a point that represents the beginning of the gap.

The timing of it is the unknown. Take a look at the left side of the chart and notice the exhaustion gaps during the selloff in 2008. They were eventually closed as the prices rose above them in 2009. It works the same in reverse.

Over many years of studying charts, I have found that accelerated up moves, such as we’ve seen recently, will very likely be followed by equally sharp moves to the downside. Just because a gap has occurred, however, does not mean the eventual downside reversal will stop there; it merely serves as a point of reference.

To me, it’s a sure thing that a pullback through at least the gap level is in the cards. When that will happen is anyone’s guess. All you can do is be prepared via your sell stops to deal with it, should a reversal turn out to be more than just a temporary correction in a bullish trend.