[Chart courtesy of MarketWatch.com]

- Moving the market

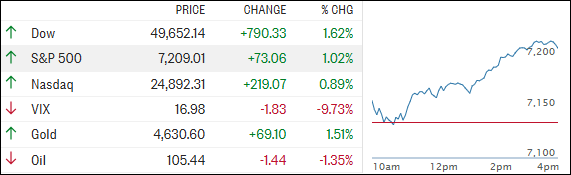

All three major indexes opened the day in positive territory, but the Dow clearly stole the show, surging more than 1% early on thanks to a strong earnings report from caterpillar, which jumped 9%.

That strength helped keep the broader market afloat even as technology struggled.

Tech was a different story. Meta platforms and Microsoft weighed heavily on the S&P 500 and Nasdaq, falling 9% and 5%, respectively.

Meta was pressured by higher‑than‑expected capital spending and softer user growth, while Microsoft pulled back after projecting total spending could climb to $190 billion due to rising memory costs.

Even with today’s tech weakness, the bigger picture remains constructive. A strong run in recent weeks has put all three major averages on track to finish the month solidly higher.

The S&P 500 is now up more than 9% month‑to‑date, setting up its best monthly performance since November 2020.

Markets are coming off a mixed session following the fed’s decision to hold rates steady at 3.5%–3.75%. While the outcome was expected, the 8‑4 vote raised eyebrows, marking the first time since 1992 that four fed officials dissented.

Several policymakers appear increasingly uneasy about inflation and seem eager to signal that the next move may not be a rate cut.

After treading water earlier in the week, stocks melted higher as dip buyers stepped in and pushed indexes to fresh all‑time highs. Among the magnificent seven, results were mixed — Google surged to a new record, while Meta went the other way.

{kind=link}

{kind=link}

Overnight, intervention by the bank of Japan pushed the dollar lower and helped drag bond yields and oil prices down as well, giving a boost to risk assets.

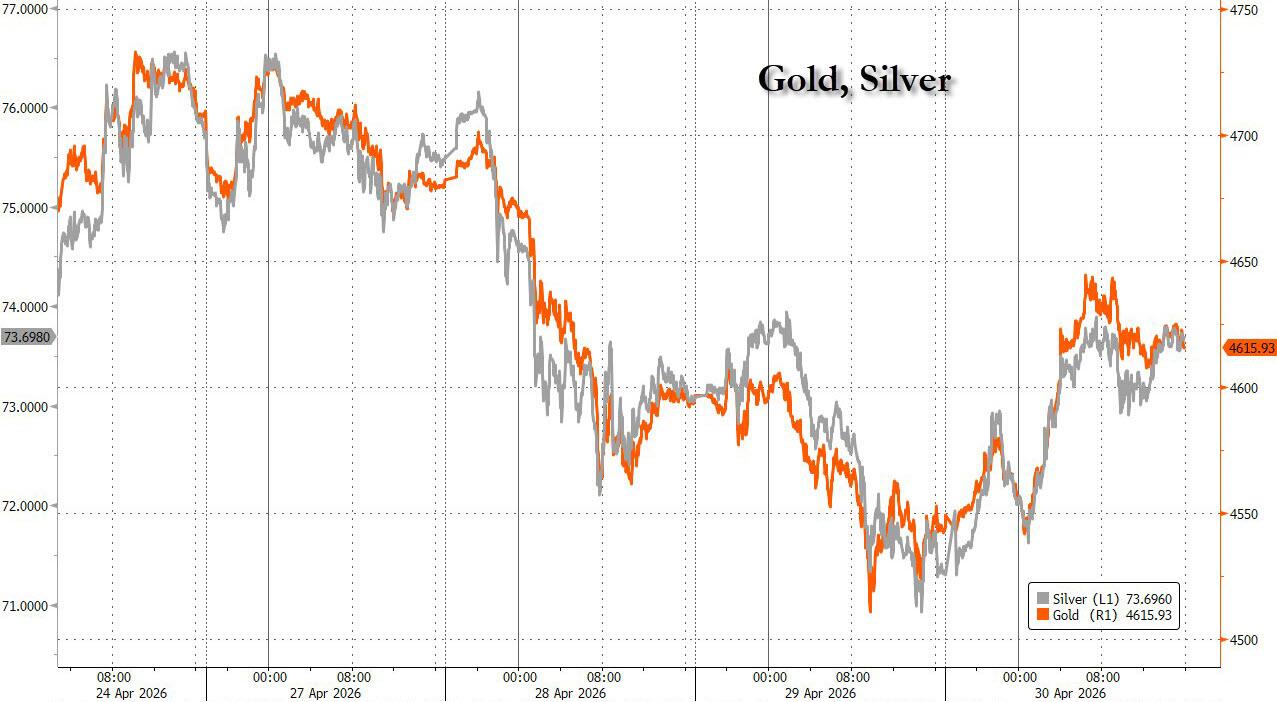

Precious metals and Bitcoin bounced during the session but remain largely stalled.

{kind=link}

{kind=link}

With Apple earnings due out this afternoon, the big question is: will they provide the next leg higher—or throw some cold water on the rally?

2. Current domestic “Buy” Cycle (effective 5/20/2025); International “Buy” Cycle (effective 5/8/25)

Our domestic bullish cycle that began on November 21, 2023, concluded on April 3, 2025, following a market downturn triggered by President Trump’s tariff policy announcement.

This development caused significant declines across major indexes and broader market indices. However, markets subsequently rebounded, culminating in a new domestic “Buy” signal taking effect May 20, 2025.

Concurrently, our International Trend Tracking Index (TTI) experienced parallel volatility. On April 4, 2025, it breached critical thresholds, prompting a “Sell” recommendation. This position reversed as global markets recovered, with the International TTI regaining sufficient momentum to issue a new “Buy” signal effective May 8, 2025.

3. Trend Tracking Indexes (TTIs)

After spending most of the week treading water, the Dow came out strong right from the opening bell and never looked back, pulling the S&P 500 and Nasdaq higher along with it.

Leadership stayed firmly intact throughout the session, giving the rally some real follow‑through.

Metals and Bitcoin joined the upside move, and our TTIs clearly got the memo—both posted solid gains, reinforcing the sense that momentum is building again.

This is how we closed 04/30/2026:

Domestic TTI: +6.25% above its M/A (prior close +4.66%)—Buy signal effective 5/20/25.

International TTI: +8.69% above its M/A (prior close +7.12%)—Buy signal effective 5/8/25.

All linked charts above are courtesy of Bloomberg via ZeroHedge.

———————————————————-

WOULD YOU LIKE TO HAVE YOUR INVESTMENTS PROFESSIONALLY MANAGED?

Do you have the time to follow our investment plans yourself? If you are a busy professional who would like to have his portfolio managed using our methodology, please contact me directly to get more details.

Contact Ulli