[Chart courtesy of MarketWatch.com]

- Moving the market

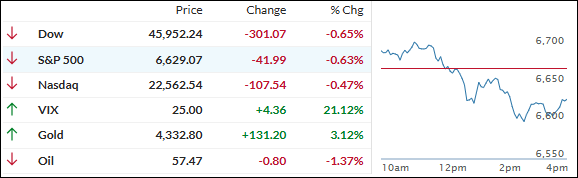

Stocks jumped out of the gate early on, fueled by upbeat bank earnings and optimistic forecasts from tech heavyweights that briefly pushed trade-war worries to the back burner.

Big Tech helped keep the early rally alive—Nvidia gained 1.2%, while Broadcom rose another 2% after Taiwan Semiconductor lifted its 2025 revenue outlook to mid-30% growth and reaffirmed plans for $42 billion in capital spending before year-end.

Momentum from earlier in the week carried over, thanks to strong reports from Goldman Sachs, Wells Fargo, and other big banks, which bolstered confidence in corporate fundamentals.

But as we’ve seen repeatedly this month, the early optimism didn’t last. Weak macro data, hawkish Fed comments, and fresh concerns over loan troubles at regional banks sapped enthusiasm by midday, with the major indexes turning south and surrendering Wednesday’s gains.

{kind=link}

The latest hit to sentiment came from two regional lenders—Zions and Western Alliance—which revealed potential loan irregularities involving alleged fraud. That renewed fears about credit quality and financial stability, sparking a flight to safety.

{kind=link}

Bonds rallied, driving the 10-year Treasury yield below 4% for the first time in a year. The dollar slipped, gold soared 3.2% to another record, and silver climbed 1.7% to crack the $54 level. Bitcoin, meanwhile, slid to $107,000 before finding some support.

{kind=link}

{kind=link}

With the market now juggling upbeat earnings, banking worries, and shifting Fed signals, is this just a healthy reset—or the start of deeper caution setting in before year-end?

2. Current domestic “Buy” Cycle (effective 5/20/2025); International “Buy” Cycle (effective 5/8/25)

Our domestic bullish cycle that began on November 21, 2023, concluded on April 3, 2025, following a market downturn triggered by President Trump’s tariff policy announcement.

This development caused significant declines across major indexes and broader market indices. However, markets subsequently rebounded, culminating in a new domestic “Buy” signal taking effect May 20, 2025.

Concurrently, our International Trend Tracking Index (TTI) experienced parallel volatility. On April 4, 2025, it breached critical thresholds, prompting a “Sell” recommendation. This position reversed as global markets recovered, with the International TTI regaining sufficient momentum to issue a new “Buy” signal effective May 8, 2025.

3. Trend Tracking Indexes (TTIs)

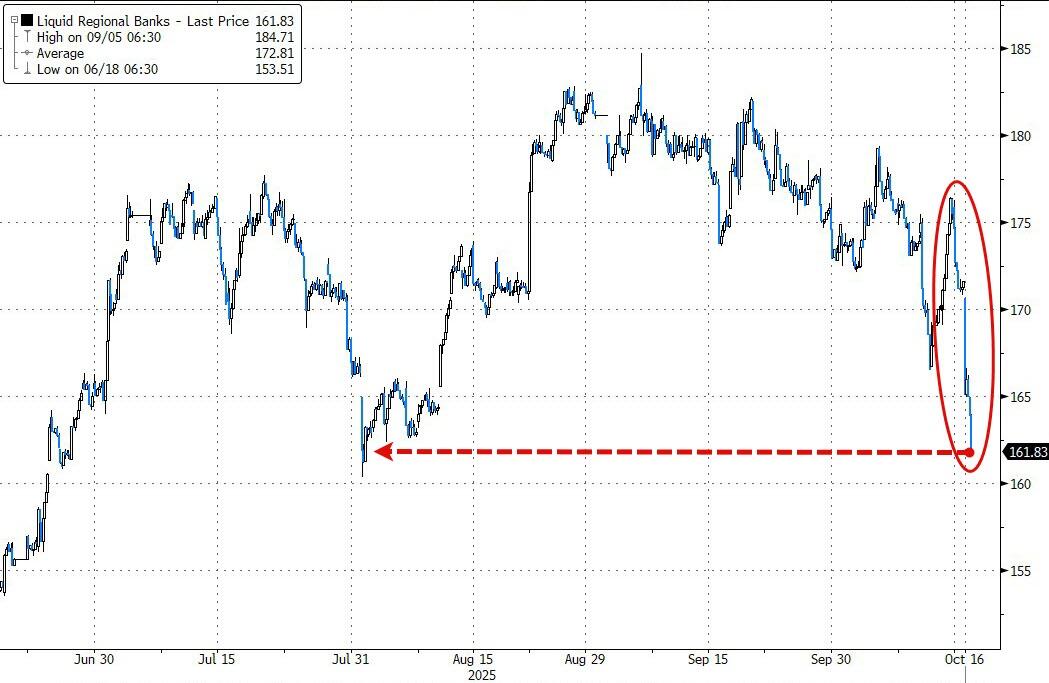

Markets came out swinging again early on, but the rally quickly hit a ceiling before fading hard into negative territory.

The main culprit this time was renewed pressure on regional banks, where concerns over loan quality and exposure to shaky commercial real estate sent a chill through the market.

A couple of lenders reported growing losses tied to bad loans, reigniting investor worries about credit risk and stability across the sector.

The selling spread beyond the banks as the session wore on, erasing the early strength that had lifted indexes at the open.

Our TTIs couldn’t fight the shift in sentiment either, with the domestic one closing lower despite remaining in broadly positive territory.

This is how we closed 10/16/2025:

Domestic TTI: +5.00% above its M/A (prior close +6.04%)—Buy signal effective 5/20/25.

International TTI: +10.87% above its M/A (prior close +10.86%)—Buy signal effective 5/8/25.

All linked charts above are courtesy of Bloomberg via ZeroHedge.

———————————————————-

WOULD YOU LIKE TO HAVE YOUR INVESTMENTS PROFESSIONALLY MANAGED?

Do you have the time to follow our investment plans yourself? If you are a busy professional who would like to have his portfolio managed using our methodology, please contact me directly to get more details.

Contact Ulli