- Moving the market

Stocks started the day on a mixed footing as investors digested a fresh round of corporate earnings and took a breather from the prior session’s rally.

The industrial and consumer names led the way, with General Motors stealing the spotlight—its stock surged more than 13% after the automaker raised its full-year outlook and topped quarterly estimates with its strongest results since 2017.

Coca-Cola and 3M followed suit, climbing 3% and 2%, respectively, after both companies posted better-than-expected profits and reaffirmed upbeat guidance for the year.

Traders are navigating a packed earnings week, with Netflix set to report after the bell and Tesla due up Wednesday.

So far, the results have given markets plenty to cheer about—roughly three-quarters of S&P 500 companies reporting have beaten expectations, extending the momentum from an already strong start to earnings season.

Adding to the optimism is speculation that the Federal Reserve could deliver another quarter-point rate cut at its late-October meeting, while Friday’s CPI report will provide the latest checkpoint on inflation pressures.

But volatility made a strong return by the afternoon. Gold plunged 6.3%, and silver tumbled 8.7%—their biggest drop in years—after months of enormous gains. However, Goldman Sachs maintained its bullish long-term outlook of $4,900.

{kind=link}

{kind=link}

For sure, a correction was likely overdue following gold’s 67% and silver’s 81% year-to-date surges. Bitcoin, meanwhile, rallied sharply earlier in the session before fading after President Trump suggested his meeting with China’s Xi may be postponed, sending risk assets wobbling again.

{kind=link}

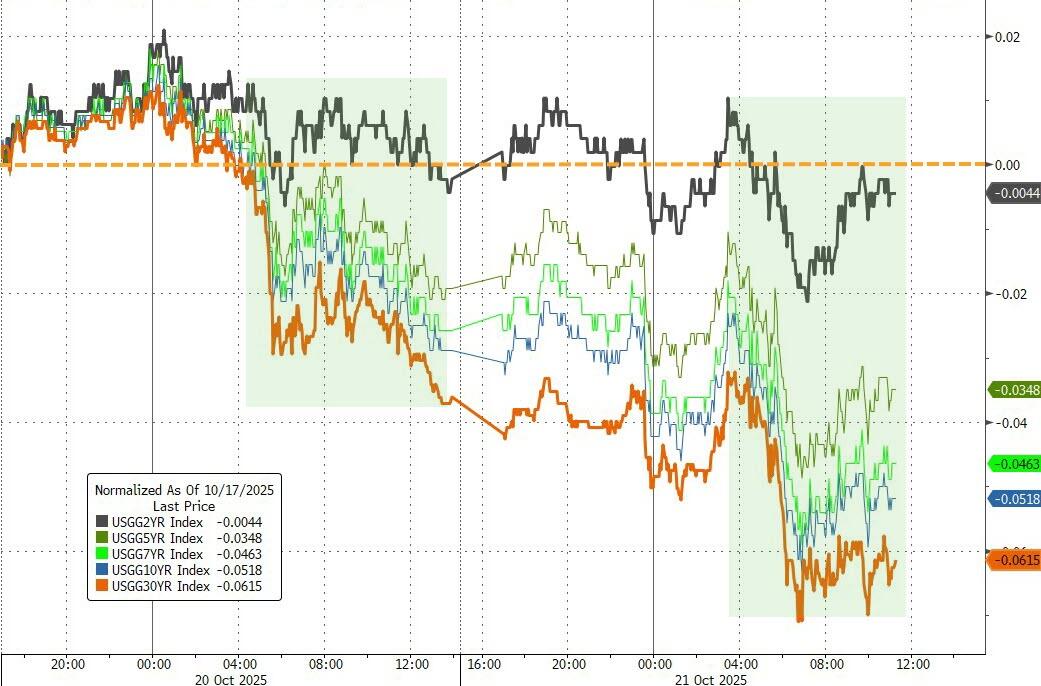

Bond yields fell, with the 10-year Treasury extending its slide below 4%, while the dollar strengthened for the third straight day.

{kind=link}

{kind=link}

{kind=link}

After such a wild session, will earnings keep providing a tailwind—or is the market showing signs of reaching its near-term limit?

2. Current domestic “Buy” Cycle (effective 5/20/2025); International “Buy” Cycle (effective 5/8/25)

Our domestic bullish cycle that began on November 21, 2023, concluded on April 3, 2025, following a market downturn triggered by President Trump’s tariff policy announcement.

This development caused significant declines across major indexes and broader market indices. However, markets subsequently rebounded, culminating in a new domestic “Buy” signal taking effect May 20, 2025.

Concurrently, our International Trend Tracking Index (TTI) experienced parallel volatility. On April 4, 2025, it breached critical thresholds, prompting a “Sell” recommendation. This position reversed as global markets recovered, with the International TTI regaining sufficient momentum to issue a new “Buy” signal effective May 8, 2025.

3. Trend Tracking Indexes (TTIs)

Markets were all over the place today, with early optimism giving way to a choppy afternoon that left only the Dow eking out a gain, while the S&P 500 and Nasdaq faded into the red by the close.

After a strong start to the week, traders took a breather as earnings season kicked into high gear and profit-taking hit some of the high-flying tech names that had led the recent rally.

Precious metals bore the brunt of the selling, with gold and silver both pulling back after their impressive runs. Given how far they’ve climbed year-to-date, a bit of cooling off wasn’t too surprising.

Our TTIs ended mixed—mirroring the broader market tone—with the domestic TTI creeping higher as strength in cyclical sectors helped offset the tech slump, while the international one slipped slightly.

This is how we closed 10/21/2025:

Domestic TTI: +6.92% above its M/A (prior close +6.43%)—Buy signal effective 5/20/25.

International TTI: +11.53% above its M/A (prior close +11.52%)—Buy signal effective 5/8/25.

All linked charts above are courtesy of Bloomberg via ZeroHedge.

———————————————————-

WOULD YOU LIKE TO HAVE YOUR INVESTMENTS PROFESSIONALLY MANAGED?

Do you have the time to follow our investment plans yourself? If you are a busy professional who would like to have his portfolio managed using our methodology, please contact me directly to get more details.

Contact Ulli