- Moving the markets

The stock market was in a bad mood on Monday, even though the politicians managed to avoid a government shutdown at the last minute.

The market ended the day flat, like a pancake. The small-cap stocks were especially unhappy, as the Russell 2000 index dropped 1.7% and turned red for the year. This was the first time the index lost money in 2023, showing that small is not always beautiful.

The Senate passed a bill to keep the government running until mid-November, just before the clock struck midnight on Saturday. President Biden signed it into law, and then probably went to bed. The lawmakers now have more time to figure out how to spend our money.

The market usually doesn’t care much about government shutdowns because they don’t affect the S&P 500 much. The average change for the index during a shutdown is zero, which is also the number of people who like shutdowns.

The Fed’s top watchdog, Michael Barr, said on Monday that interest rates will stay high for a long time. He said we should focus more on how long they will be high, rather than if they will go up one more time this year. The market got the message and shifted its expectations from dovish to hawkish.

The Manufacturing PMI report showed that inflation was heating up faster than a microwave, and the Fed speakers confirmed that they were not going to cool it down anytime soon. Fed Governor Michelle Bowman said that they may need to raise rates several times to bring inflation back to 2%. She said she still expects more rate hikes in the future, which is like saying she expects more pain in the future.

{kind=link}

That tough talk boosted the dollar, which hurt oil and gold prices. Oil slipped below $90, while gold hit new lows. Gold bugs must be feeling very lonely right now.

{kind=link}

{kind=link}

{kind=link}

Bond yields jumped with the 10-year Treasury yield rising more than 10 basis points to 4.68% on Monday. Investors dumped Treasurys like hot potatoes after they heard that the government was not going to shut down. Apparently, they prefer risk over safety these days.

{kind=link}

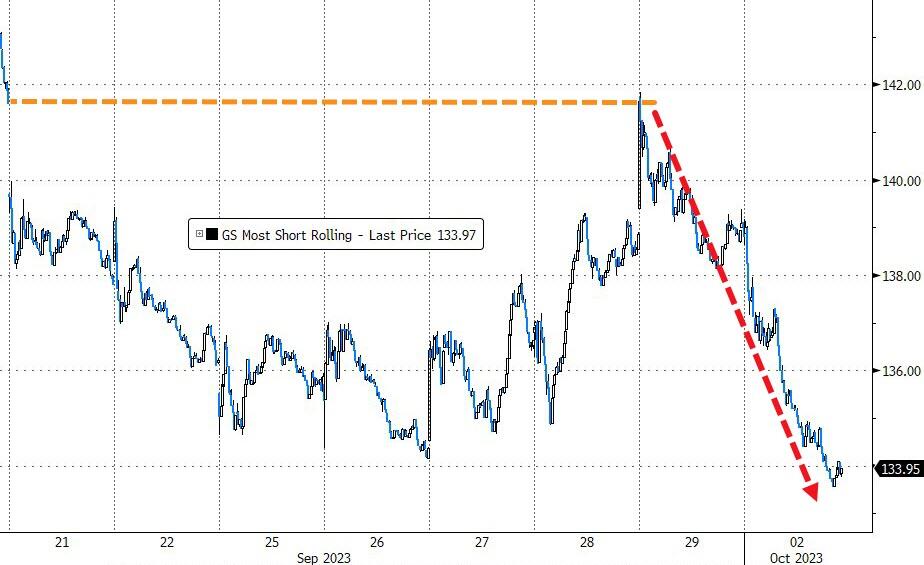

The most hated stocks got crushed, as the short squeeze from last Thursday ran out of steam and reversed. The shorts must be feeling very smug right now. Financial conditions are getting tighter, which means that stocks may have more downside ahead, according to ZeroHedge.

{kind=link}

{kind=link}

But who knows, maybe a big rally will come out of nowhere and change everything. Could that happen? Or are we doomed? You never know what will happen next in this crazy market.

2. “Buy” Cycle (12/1/22 to 9/21/2023)

The current Domestic Buy cycle began on December 1, 2022, and concluded on September 21, 2023, at which time we liquidated our holdings in “broadly diversified domestic ETFs and mutual funds”.

Our International TTI has now dipped firmly below its long-term trend line, thereby signaling the end of its current Buy cycle effective 10/3/23.

We have kept some selected sector funds. To make informed investment decisions based on your risk tolerance, you can refer to my Thursday StatSheet and Saturday’s “ETFs on the Cutline” report.

Considering the current turbulent times, it is prudent for conservative investors to remain in money market funds—not bond funds—on the sidelines.

3. Trend Tracking Indexes (TTIs)

The S&P 500 was mostly lower than the previous day, but it recovered slightly and ended with a small gain. Only a few stocks did well.

Our Domestic TTI dove and showed that the US market is in bad shape and likely to stay that way for a while.

The International TTI also indicated that the foreign market is not doing well and gave us a “Sell” signal, effective tomorrow, unless the market surprises us with a huge rebound.

This is how we closed 10/2/2023:

Domestic TTI: -3.70% below its M/A (prior close –2.61%)—Sell signal effective 9/22/2023.

International TTI: -1.38% below its M/A (prior close -0.36%)—Sell signal effective 10/3/2023.

All linked charts above are courtesy of Bloomberg via ZeroHedge.

Contact Ulli