- Moving the markets

Again, the belief prevailed on Wall Street that the worst of the regional banking crisis is now in the rearview mirror, which caused traders and algos to push the major indexes higher for the second day in a row.

Jobless claims dropped moderately but have not gone anywhere in four months, thereby supporting hopes that the Fed might be inclined to slow down its tightening efforts, as the labor market appears to show signs of cooling, which in turn gave an assist to equities.

{kind=link}

To me it looks like the market is getting ahead of itself by pricing in a Goldilocks scenario, in which we would see the best of both worlds: Traders expecting a recession with low rates and reduced inflation in an environment that does not negatively affect corporate earnings.

Sure, such a setting would indeed be good for equities, but I don’t think this scenario is even remotely realistic, because all banks are in similar situations like the failed ones, it just has not become public knowledge yet.

That means more systemically important institutions will have to be bailed out with money that the US Treasury doesn’t have. Therefore, dollars must be created out of thin air, and inflation will rear its ugly head again. If the Fed is serious about battling back, interest rates/bond yields will have to go considerably higher.

These are all known cause-and-effect facts, the only unknown at this moment is the timing of it.

Despite this unbridled optimism about the banking crisis, the regional banking index KRE slipped after riding the roller coaster all day. Stocks followed suit with one Fed governor spewing hawkish words while another walked back the tough talk with some dovish tones, which pulled equities out of their midday slide.

{kind=link}

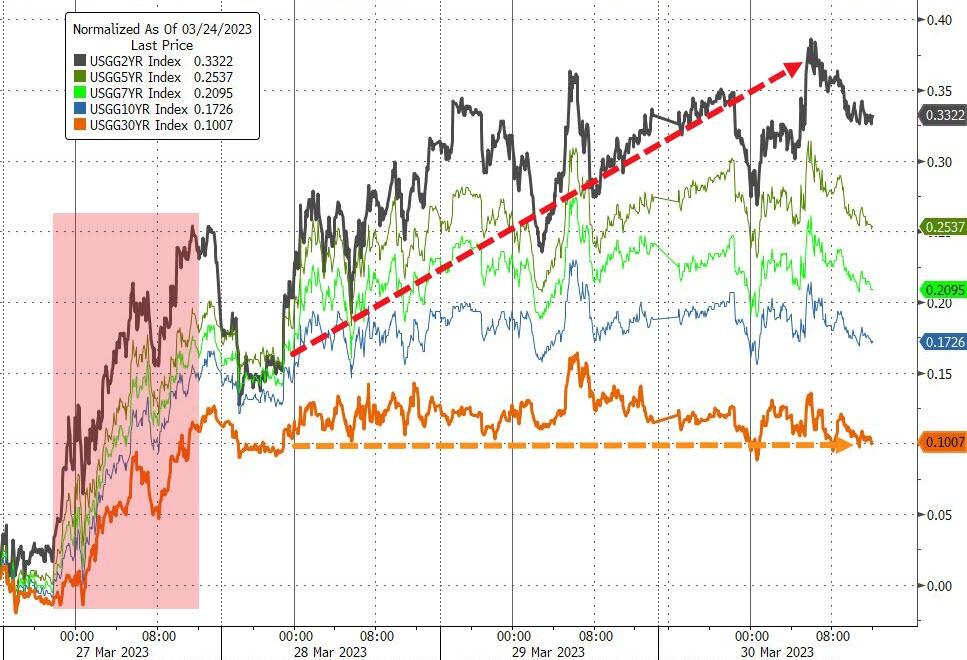

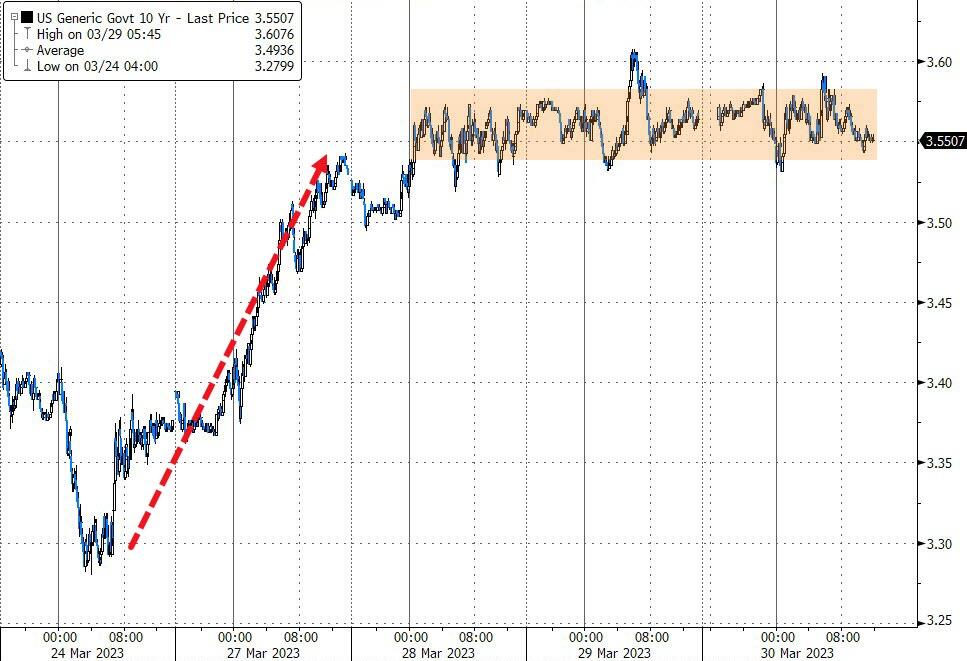

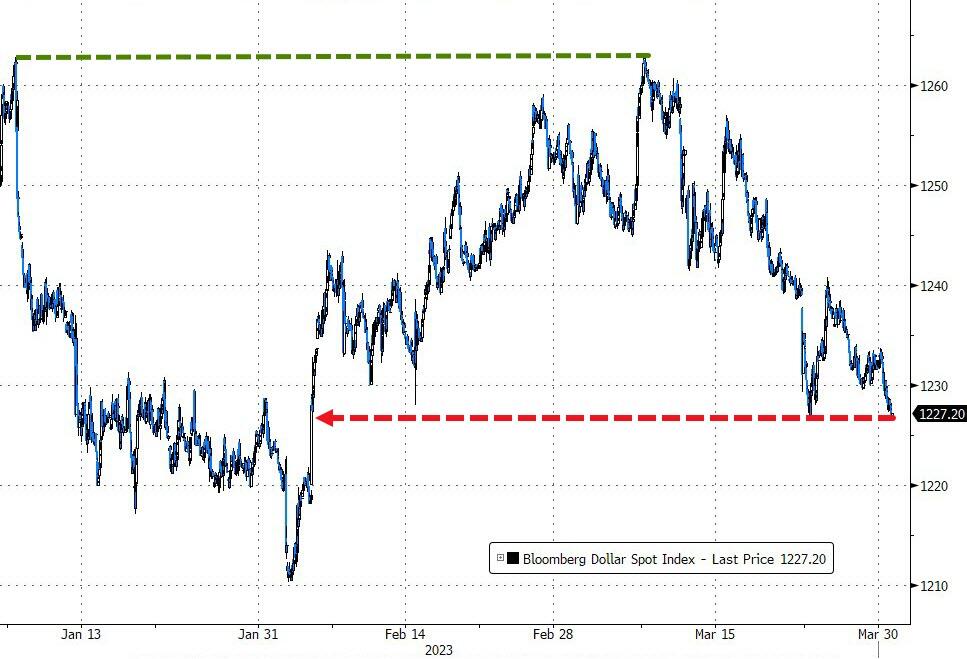

Bond yields slipped a tad, with the 10-year continuing its 3-day sideways pattern. The US Dollar fell to its lowest close since February 3rd, while Gold ripped higher by +1.63% and stopping just short of its $2k level.

{kind=link}

{kind=link}

{kind=link}

2. “Buy” Cycle Suggestions

For the current Buy cycle, which started on 12/1/2022, I suggested you reference my then current StatSheet for ETF selections. However, if you came on board later, you may want to look at the most recent version, which is published and posted every Thursday at 6:30 pm PST.

I also recommend you consider your risk tolerance when making your selections by dropping down more towards the middle of the M-Index rankings, should you tend to be more risk adverse. Likewise, a partial initial exposure to the markets, say 33% to start with, will reduce your risk in case of a sudden directional turnaround.

We are living in times of great uncertainty, with economic fundamentals steadily deteriorating, which will eventually affect earnings negatively and, by association, stock prices.

In my advisor’s practice, we are therefore looking for limited exposure in value, some growth and dividend ETFs. Of course, gold has been a core holding for a long time.

With all investments, I recommend the use of a trailing sell stop in the range of 8-12% to limit your downside risk.

3. Trend Tracking Indexes (TTIs)

With market sentiment maintaining yesterday’s bullish bias, our TTIs moved deeper into bullish territory with the Domestic one being the weaker of the two.

However, as we are moving into April next week, we will find out if this 2-day ramp higher was simply quarter ending window dressing or actually the resumption of the bull market. If it’s the latter, we will add to current holdings.

This is how we closed 03/30/2023:

Domestic TTI: +0.98% above its M/A (prior close +0.48%)—Buy signal effective 12/1/2022.

International TTI: +6.52% above its M/A (prior close +5.53%)—Buy signal effective 12/1/2022.

All linked charts above are courtesy of Bloomberg via ZeroHedge.

Contact Ulli