ETF Tracker StatSheet

You can view the latest version here.

EQUITIES FINISH THEIR WORST YEAR SINCE 2008 WITH A SELL-OFF

[Chart courtesy of MarketWatch.com]

- Moving the markets

Despite the market’s successful attempt at staging a rally yesterday, it was not enough to overcome the weakness in equities, as the indexes simply got whiplashed with nothing to show for when looking at the past week.

{kind=link}

This type of activity pretty much reflects how 2022 played out, with the indexes notching their worst year since 2008 and leaving the buy and hold crowd with steep losses, despite a positive the 4th quarter.

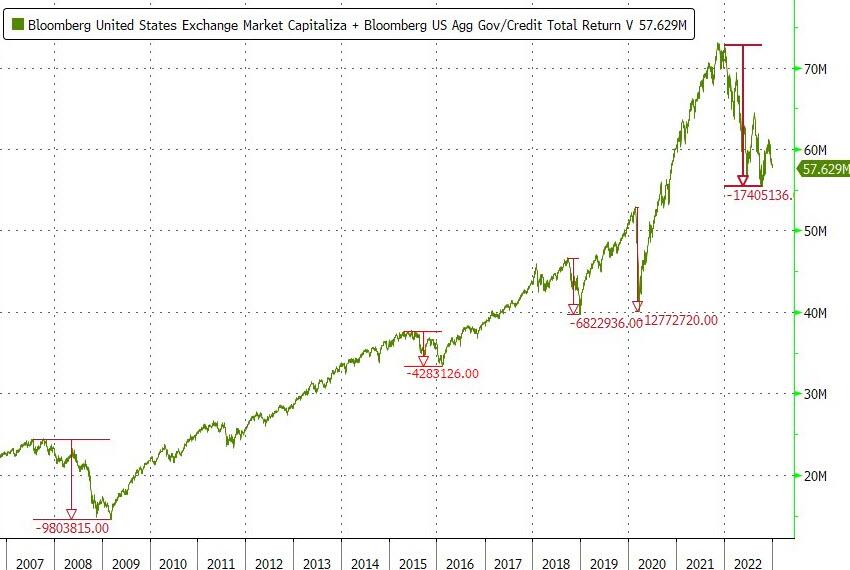

YTD, the S&P 500 (SPY) dropped around -19.3% with bonds faring far worse, as the widely held Bond ETF TLT dumped an amazing -32%, which was only “outdone” by the Nasdaq’s -33% loss. So much for the perceived safety of bonds. Combined, US equity and bond markets lost $17.4 trillion at their October lows. Ouch!

{kind=link}

The current environment is best described as skittish, which is clearly demonstrated by the lack of direction of our Trend Tracking Indexes (TTIs), which have now been hugging their trendlines for several weeks (section 3).

Geopolitical worries and mixed economic date are here to stay and will keep the Wall Street crowd on edge. After all, the menu of concerns has not been reduced, and we will still have to deal with Covid problems in China, the Ukraine conflict, slowing global growth, upcoming 4th quarter earnings, the potential slowdown in Q1 2023 earnings—and Fed policies.

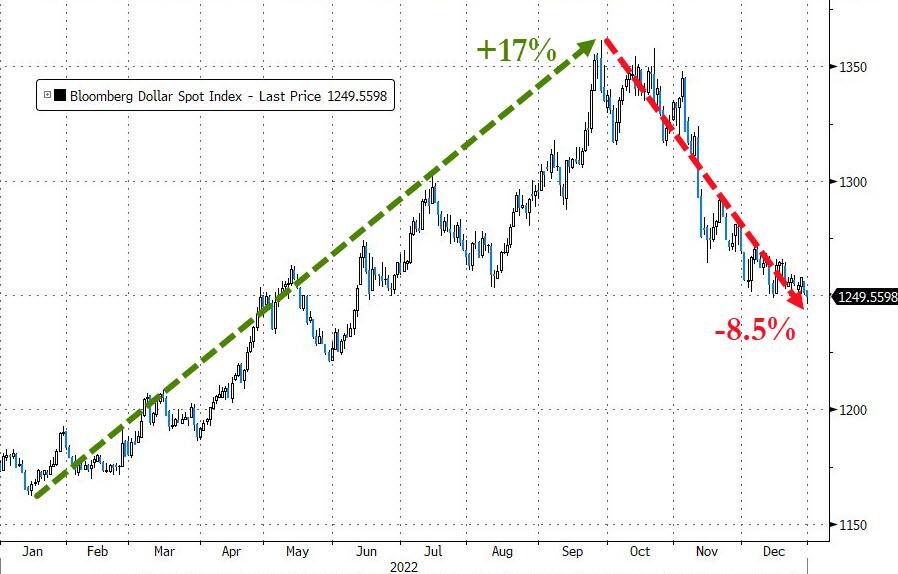

Bond yields exploded higher this year, as the Fed followed through with its inflation fighting endeavors causing the US Dollar to surge, despite a 4th quarter sell-off. Gold rode the rollercoaster but managed to close out the year unchanged.

{kind=link}

{kind=link}

{kind=link}

And for the last time in 2022, the 2008-2009 analog now looks like this.

{kind=link}

Which way will it break?

Happy New Year!

2. “Buy” Cycle Suggestions

For the current Buy cycle, which starts on 12/1/2022, I suggest you reference my most recent StatSheet for ETFs selections. If you come on board later, you may want to look at the most current version, which is published and posted every Thursday at 6:30 pm PST.

I also recommend for you to consider your risk tolerance when making your selections by dropping down more towards the middle of the M-Index rankings, should you tend to be more risk adverse. Likewise, a partial initial exposure to the markets, say 33% to start with, will reduce your risk in case of a sudden directional turnaround.

We are living in times of great uncertainty, with economic fundamentals steadily deteriorating, which will eventually affect earnings negatively and, by association, stock prices. I can see this current Buy signal to be short lived, say to the end of the year, and would not be surprised if it ends at some point in January.

In my advisor practice, we are therefore looking for limited exposure in value, some growth and dividend ETFs. Of course, gold has been a core holding for a long time.

With all investments, I recommend the use of a trailing sell stop in the range of 8-12% to limit your downside risk.

3. Trend Tracking Indexes (TTIs)

Our TTIs remained above their respective trend lines with the Domestic one showing more weakness than its international cousin.

This is how we closed 12/30/2022:

Domestic TTI: +0.16% above its M/A (prior close +0.30%)—Buy signal effective 12/1/2022.

International TTI: +2.16% above its M/A (prior close +2.06%)—Buy signal effective

12/1/2022.

Disclosure: I am obliged to inform you that I, as well as my advisory clients, own some of the ETFs listed in the above table. Furthermore, they do not represent a specific investment recommendation for you, they merely show which ETFs from the universe I track are falling within the specified guidelines.

All linked charts above are courtesy of Bloomberg via ZeroHedge.

———————————————————-

WOULD YOU LIKE TO HAVE YOUR INVESTMENTS PROFESSIONALLY MANAGED?

Do you have the time to follow our investment plans yourself? If you are a busy professional who would like to have his portfolio managed using our methodology, please contact me directly to get more details.

Contact Ulli