U.S. equities fought off early pressure but retreated at the end, giving benchmark indexes their first back-to-back drops in one month. The exacerbated concerns over the possible scaling back of asset purchases by the Federal Reserve along with disappointing Chinese manufacturing data were just too much to overcome.

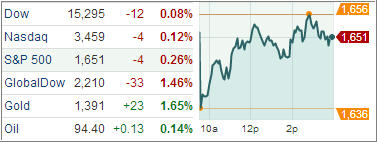

The Dow Jones Industrial Average lost 12 points (0.1%) to 15,295, the S&P 500 Index declined 5 points (0.3%) to 1,651, and the Nasdaq Composite descended 4 points (0.1%) to 3,459.

All ten sectors of the S&P 500 began the session with sharp losses before the daylong rebound helped some groups return to yesterday’s closing levels. The Index opened with a loss of 1.2% after Japan’s Nikkei tumbled 7.3%, largest drop since the aftermath of the March 2011 earthquake and Tsunami. What caused that swan dive?

The pressure on Japanese stocks came courtesy of the rallying yen while the yield on Japan’s benchmark 10-year government bond rose to 1% for the first time in a year. Adding insult to injury was news out of China where the HSBC Flash Manufacturing PMI Index unexpectedly declined to 49.6 for May from 50.4 in April. Economists forecasted the index to remain at the same level. A reading below 50 denotes a reduction in output for the manufacturing sector.

The utilities sector was the weakest performer, ending lower by 0.8% after a morning flash crash in American Electric Power and NextEra Energy briefly wiped out more than $33 billion in combined market capitalization.

While the Dow and Nasdaq made a couple intraday appearances in positive territory, the S&P was kept from seeing green by the weakness in banks. The financial sector settled lower by 0.6% as most majors registered losses. Other defensively-oriented sectors outperformed the broader market with the telecom space registering a gain. Cyclical groups were mixed throughout the day as technology and materials made a brief appearance in positive territory.

Elsewhere, the relative strength in chemical producers overshadowed the weakness of steelmakers as the materials sector ended little changed. Gold miners also outperformed as the yellow metal rose 1.8% to $1391.30 per troy ounce. However, copper fell 1.9% as disappointing Chinese data weighed.

At lease there was some good news. Initial claims for unemployment insurance dropped 23,000 last week, the most in six weeks, to 340,000. Economists expected a smaller pullback to 345,000. The four-week average of claims indicates a downward trend in firings. This level of claims is consistent with modest payrolls growth. Economic fundamentals remain shaky; beg the question, how much addicted is stock to QE stimulus?

Well, we all know the answer that question. In the event QE is being removed in serious fashion, this bull market will be over in a hurry. So, always be prepared and have your trailing sell stops ready to be executed.

While that moment in time has not arrived yet, our Trend Tracking Indexes (TTIs) showed weakness and joined the major indexes by pulling back as well. The Domestic TTI ended the day at +4.28% while the International TTI closed at +8.87%.

For all of the latest charts and momentum figures, be sure to tune into my latest StatSheet, which I will post around 6 pm PST.

Contact Ulli