Reader Mark has some justified concerns as to where we’re going economically and how we can prepare ourselves investment wise for an uncertain future. Here’s what he wrote:

I want to ask you about something that is beginning to worry me as it relates to the markets domestically and to a lesser degree internationally. Much of the world is pinned to the value of the dollar and transactions (such as oil) are based on the dollar.

There is a growing sentiment out there that the only thing that allows the U.S. to manage its overwhelming debt burden is its ability to print money – which it can only do because most of the world accepts the dollar as the pinning currency.

However, countries are starting to pull back on the dollar as the “benchmark” currency against which transactions are pinned. China for example is not going to base as many things on the dollar value and meetings between Japan, China, and others seem to indicate the dollar may not be able to hold its international currency strength. You probably heard Geithner saying that he will not devalue the dollar but he may not have a choice.

So I am concerned about what it means for investments in general going forward. Should there be a start to more investment in gold and silver?

What is going to happen when commodities start to go on an upward tear (like gasoline, precious metals, milk, etc.)?

I am interested in your thoughts. Some stories out there indicate that the time is now to prepare for what may be a looming, major financial crisis because of a dollar that will not have clout. I read that the U.S. debt burden could not be met even if every American was taxed 100%.

Pretty scary!

I have always referred to the dollar as being the world’s favorite whipping boy. There was much talk some six months ago for the dollar era coming to an end along with another currency to become the new benchmark, especially when it came to the pricing of crude oil. The obvious contender and number 1 pick for the job was the Euro.

Well, how fast things can change. The European debt crisis, far from being over, will have far reaching unintended and unknown consequences in the future with one being the much discussed question as to whether the Euro can even survive. Let’s wait and see what happens once the first country of the Euro zone reneges on their debt obligation. I believe that this is not a matter of if but when.

Those factors have pretty much sealed the dollar’s position as the remaining reserve currency. The dollar has rallied over the past few months, much to the chagrin of Geithner and company. Their official position is a strong dollar; but in reality they prefer a weaker one to gain export advantages. In fact, all industrialized nations want their currencies to be weaker for the same reason.

Looking around the global scene, we have real estate bubbles in Canada, Australia and China with the Chinese economy needing to be reined in because of inflationary concerns. Japan is continuing to have its own debt problems resulting from their real estate bust some 20 years ago and their futile attempts to fight deflationary forces with stimulus programs.

No matter where you look, things don’t look pretty, and a major financial crisis could develop anywhere. Rather than trying to make a wild guess as to where the first domino might fall, just focus on the long-term trends of various asset classes.

Precious metals, commodities, energy and stock markets in general are trending up. If a crisis erupts, precious metals will very likely be the primary beneficiary. If global economic expansion continues, or shortages arise, energy, oil and commodities will rally higher.

That’s why I have rebalanced our portfolios over the past few months to include the above asset classes since they appear to be firmly entrenched above their respective long-term trend lines.

While you can own precious metals outright via various ETFs, my preference has been to hold them in a more conservative way via PRPFX. It makes those $50 drops in the price of gold easier to handle, although for some clients we hold positions in GLD outright.

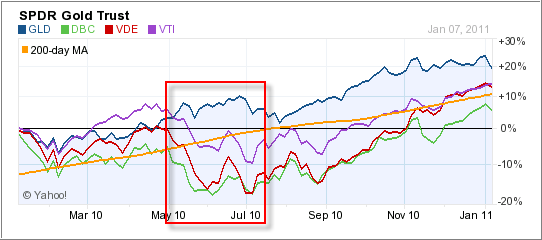

The chart above shows some of the other holdings we currently have exposure in covering the entire domestic stock market (VTI), the commodity index (DBC), energy (VDE) and gold (GLD). As you can see, after the market meltdown during May/June 09, all have resumed their previous uptrends.

No one knows what the future holds, but I believe that these asset classes are an important part of our portfolios to counteract whatever crisis might develop. Of course, this is my view right now, and I will change it not only when the facts change but when there is a clear directional trend reversal as well.

Uncertainty is here to stay with us, and it pays to be prepared should a black swan event develop in 2011, the likelihood of which seems to have increased quite a bit over the past year.