- Moving the Markets

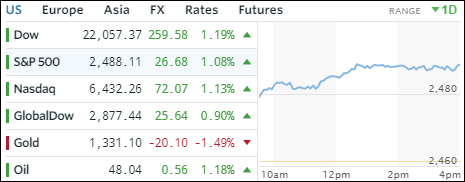

After yesterday’s massive rebound, the major indexes continued with their bullish theme supported by Treasury Secretary Mnuchin’s words that he’s hopeful a tax overhaul can be accomplished by the end of the year. He also hinted that they’re considering backdating any reform to the beginning of 2017. That’s all it took, and stocks ended at record highs, although in zigzag fashion, however, without ever touching the unchanged line.

The Dow ended in the green, but would have done so with far more conviction had it not been for weakness in McDonalds (-3.22%) and Apple (-0.40%), the latter of which managed to wipe out most of its early losses, as the new iPhone launch could not meet hyped up expectations as problems with the facial recognition feature and delayed ship dates were found to be upsetting.

In the ETF equity arena, we saw SmallCaps (SCHA) take the lead with a gain of +0.67%, with Transportations (IYT) taking a close second by adding +0.61%. Emerging Markets (SCHE) and Aerospace & Defense (ITA) showed the only red numbers, namely –0.07% and -0.21% respectively.

The dead cat bounce in Treasury yields continued with the 10-year rising 3 basis points to 2.17%. That took the bullish steam out of the 20-year bond price (TLT), which sank -0.53%. The US dollar index (UUP) traded in a tight range and gave back a modest -0.04% joined by gold, which retreated -0.22% to close at $1,333.