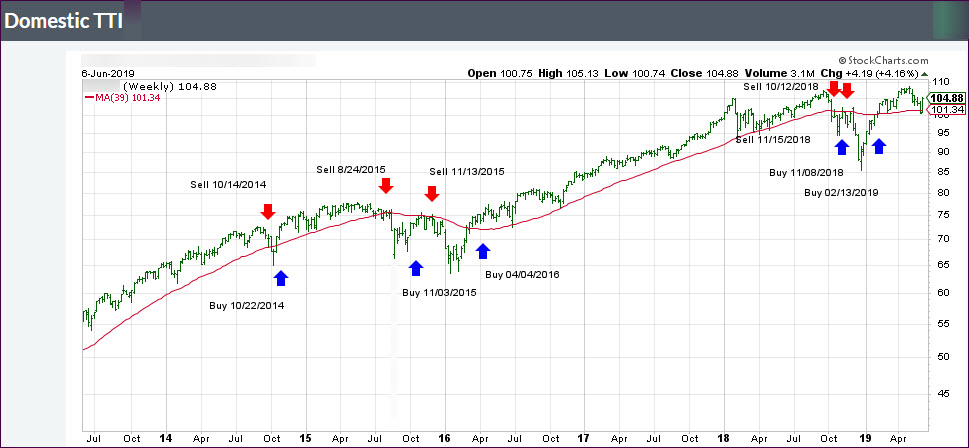

ETF Tracker StatSheet

You can view the latest version here.

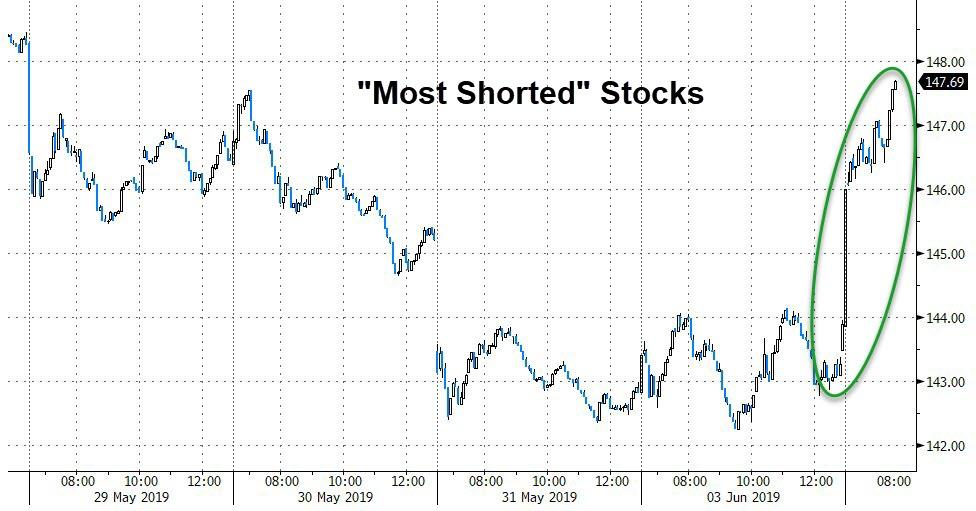

BAD NEWS IS GOOD NEWS—AGAIN

- Moving the markets

Never mind poor economic news such as a huge payroll miss, as only 75k new jobs were created during the month of May. That was against a consensus of 175k, so you would be thinking clearly had you expected a subsequent sell-off in the equity markets.

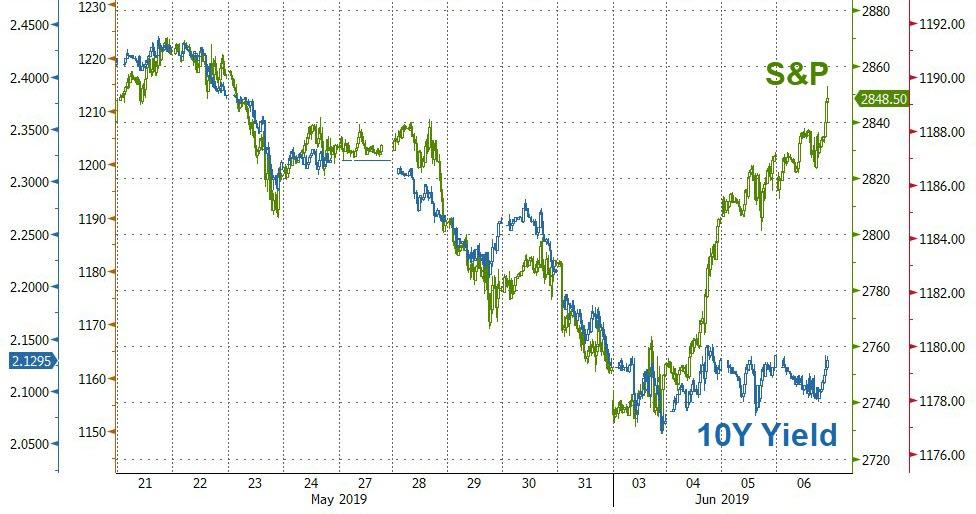

Well, that is not how it works these days. The worse the economic numbers, the greater the likelyhood that the Fed ‘could’ lower interest rates, which would be a boost for the stock market. Of course, the economy has been showing weakness wherever you look, which has been the justification for bond yields to head as far south as they did.

Unfortunately, those low bond yields are painting a picture of a possible recession, while the S&P 500 paints a picture of economic growth, which has created this conundrum with one analyst correctly observing that Bonds are from Venus and Stocks are from Mars.

Eventually a re-syncing will have to occur, and my guess is that the ‘smart money’ (bonds) will win this battle ultimately. This simply means that stocks will have to catch down to the reality of low bond yields—eventually.

In the end, it was the Fed’s jawboning about possible lower rates that sparked the best week for equities in some 6 months, which in the past did not end well, as that chart shows.

And for some Friday humor, ZH quipped:

“Markets jump on optimism U.S. economy sliding into recession.”

“The Fed won’t cut rates until stocks plunge, which won’t happen because the Fed is expected to cut if stocks plunge…”

And then posing this question tongue-in-cheek:

So, Finally, what drove this week’s almost unprecedented surge in stocks?

Answer:

Simple – Trump launching Mexican, Indian trade war; US labor market cracking; US GDP slowing; German manufacturing collapsing; S. Korean export drop needs a bigger chart; Global PMIs plunging; bond yields crashing…

Other than that, everything is fine, but I’m left pondering “how much upside is really left?”

Read More

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}