Below, please find the latest High-Volume ETF Cutline

report, which shows how far above or below their respective long-term trend

lines (39-week SMA) my currently tracked ETFs are positioned.

This report covers the HV ETF Master List from Thursday’s

StatSheet and includes 322 High Volume ETFs, defined as those with an average

daily volume of more than $5 million, of which currently 272 (last week 278)

are hovering in bullish territory. The yellow line separates those ETFs that

are positioned above their trend line (%M/A) from those that have dropped below

it.

In case you are not familiar

with some of the terminology used in the reports, please read the Glossary of Terms.

If you missed the original

post about the Cutline approach, you can read it here.

Yesterday’s

extremely dovish words by the Fed’s mouthpiece Williams seem to have struck

some raw nerves, as the Fed tried to walk back the “communications debacle.” It

was like putting the toothpaste back in the tube, as William’s viewpoint raised

market expectations to an upcoming 0.5% rate cut as opposed to a potential

0.25% reduction.

This

kind of head fake caused the NY Fed to subsequently release a statement stating

that “President William’s speech on Thursday afternoon was not intended to

send a signal that the Fed might make a

large interest rate cut but rather is was ‘an academic speech on 20 years of

research.’”

Of

course, the markets reacted positively yesterday, but today’s reality check pulled

the major indexes off their early session highs and sent them south with all

three of them not only closing in the red but also at the lows for the day. Summing

it up, the Fed better deliver a 0.25% rate cut, or equities will head south in

a big way.

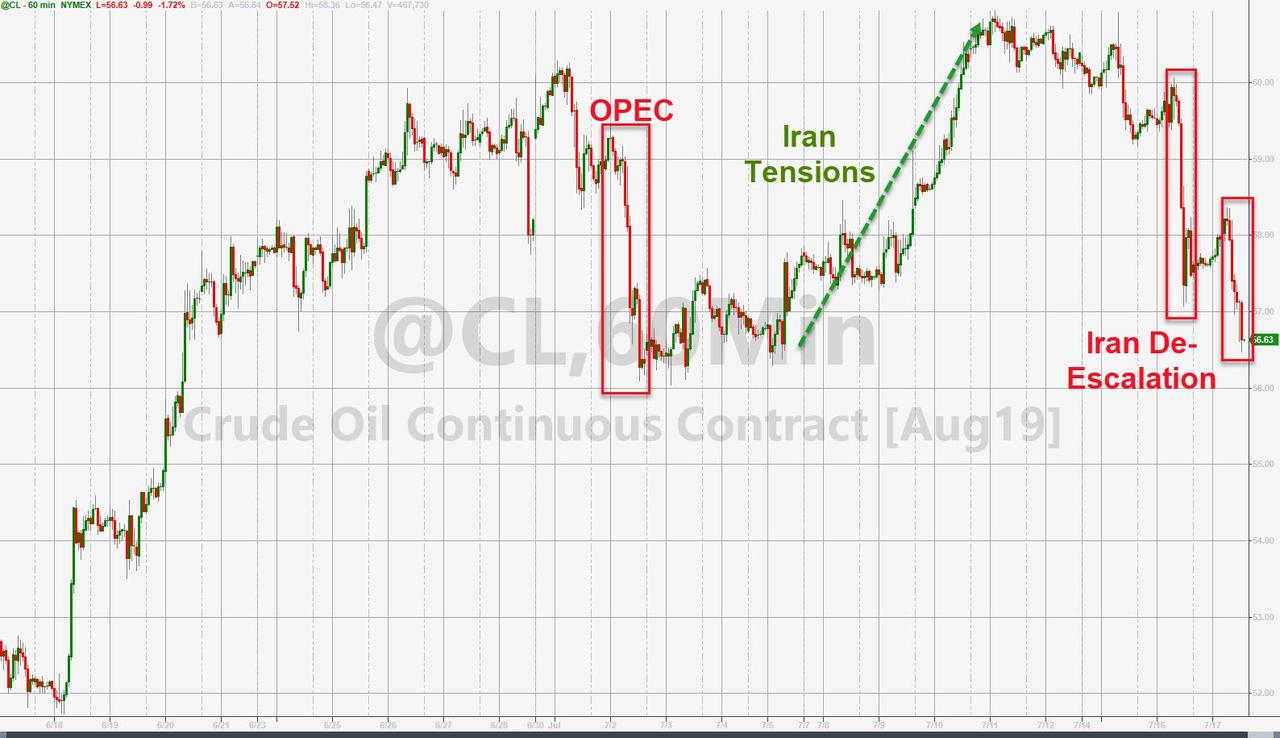

Tensions

in the Middle East ratcheted up a notch, as a drone was downed, and an oil tanker

was hijacked, which had traders is a sour mood adding to the overall negativity

in the marketplace.

While

bond yields tumbled for the week, they did spike today, thereby negatively

affecting bond prices, as well as low volatility ETFs, such as SPLV.

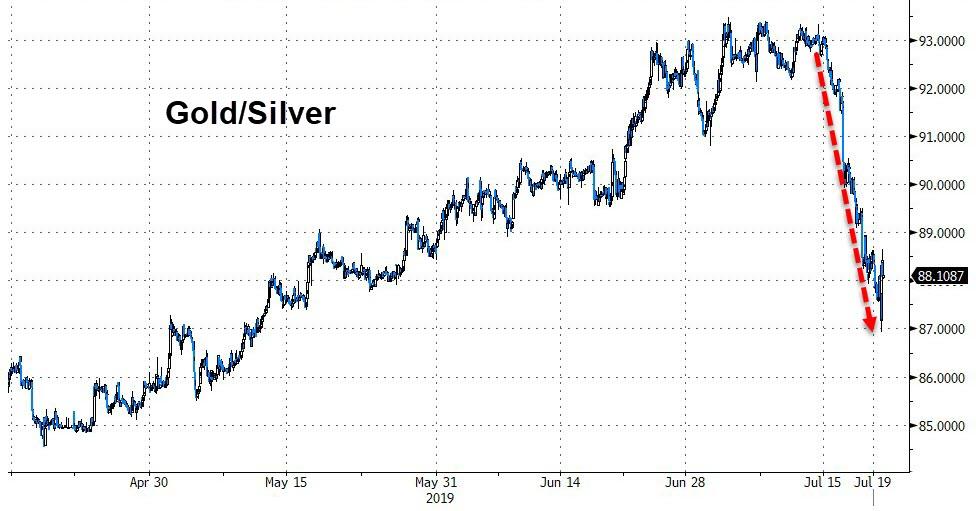

Benefiting

from all this turmoil was the long-forgotten metal, namely silver. It soared

over 6% for the week and is back above $16. This was silver’s biggest weekly

gain since July 2016, and it improved its ratio with gold considerably, as the chart

shows.

While

all eyes are on the Fed, they will not issue their verdict on interest rates

until July 31, which means we have another 1.5 weeks to put up with the seemingly

endless jawboning as to why they should or should not pull the trigger.

1. From the universe of over 1,800 ETFs, I have selected only those with a

trading volume of over $5 million per day (HV ETFs), so that liquidity and a

small bid/ask spread are assured.

2. Trend Tracking Indexes (TTIs)

Buy or Sell decisions for Domestic and International ETFs (section 1 and

2), are made based on the respective TTI and its position either above or below

its long-term M/A (Moving Average). A crossing of the trend line from below

accompanied by some staying power above constitutes a “Buy” signal. Conversely,

a clear break below the line constitutes a “Sell” signal. Additionally, I use a

7.5% trailing stop loss on all positions in these categories to control

downside risk.

3. All other investment arenas do not have a TTI and should be traded

based on the position of the individual

ETF relative to its own respective trend line (%M/A). That’s why those signals

are referred to as a “Selective Buy.” In other words, if an ETF crosses its own

trendline to the upside, a “Buy” signal is generated. Since these areas tend to

be more volatile, I recommend a wider trailing sell stop of 7.5% -10% depending

on your risk tolerance.

If you are unfamiliar with some of the terminology, please see Glossary of Termsand new subscriber information in section 9.

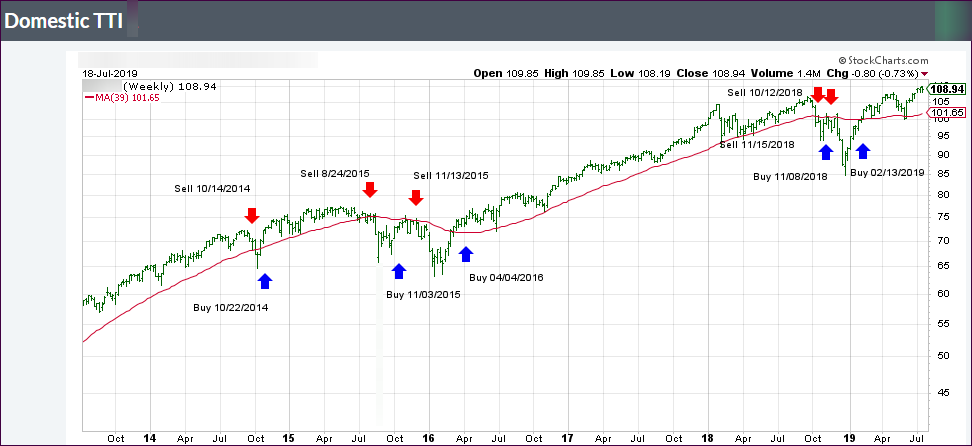

1. DOMESTIC EQUITY ETFs: BUY

— since 02/13/2019

Click on chart to enlarge

Our main directional indicator, the Domestic Trend Tracking Index (TTI-green line in the above chart) is now positioned above its long-term trend line (red) by +7.44% after having generated a new Domestic “Buy” signal effective 2/13/19 as posted.

Yesterday, the markets closed on a sour note by scoring

their lows for session in the final seconds of trading. That usually does not

bode well for the next day’s opening, and today was no exception.

The major indexes slipped early on but managed to rebound

by mid-day with fresh upward momentum pushing equities into the green, caused

by the Fed’s Williams opining that:

“interest rates should be cut as insurance against an

economic downturn,”

And

“when you have only

so much stimulus at your disposal, it pays to act quickly to lower rates at the

first sign of economic distress.”

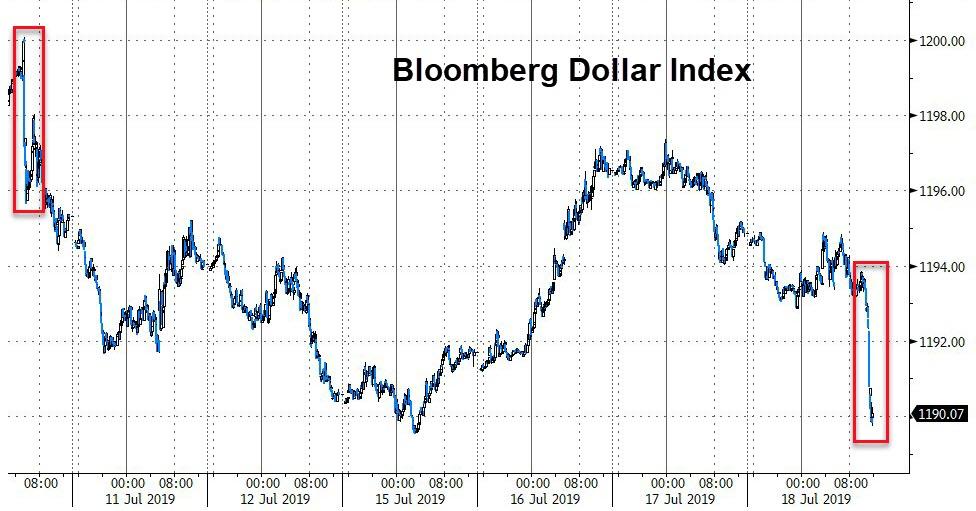

That pretty much saved the day for stocks but took the starch

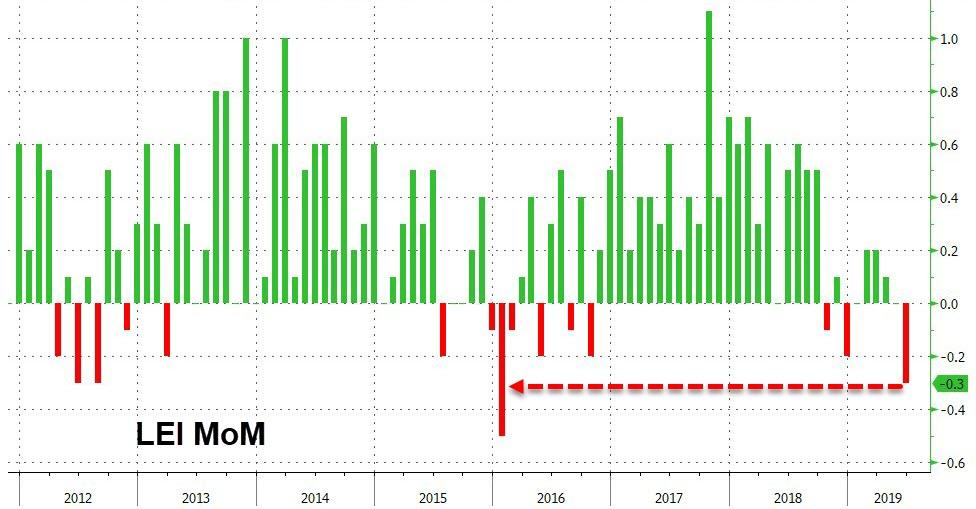

out of the US

dollar, as the latest Leading Indicators headline did not help matters. They

slumped the most in over 40 months by tumbling -0.3% in June, which was their

biggest MoM

drop since early 2016.

Then the WSJ reported that trade-deal negotiations

between the U.S. and China had hit a snag (what else is new?) raising doubts

about whether the warring parties can ever reconcile their differences.

On the earnings front, things were mixed at best with

Netflix being the loser of the day by surrendering almost -11%. This was due to

a bad miss on expectations for new paying subscribers.

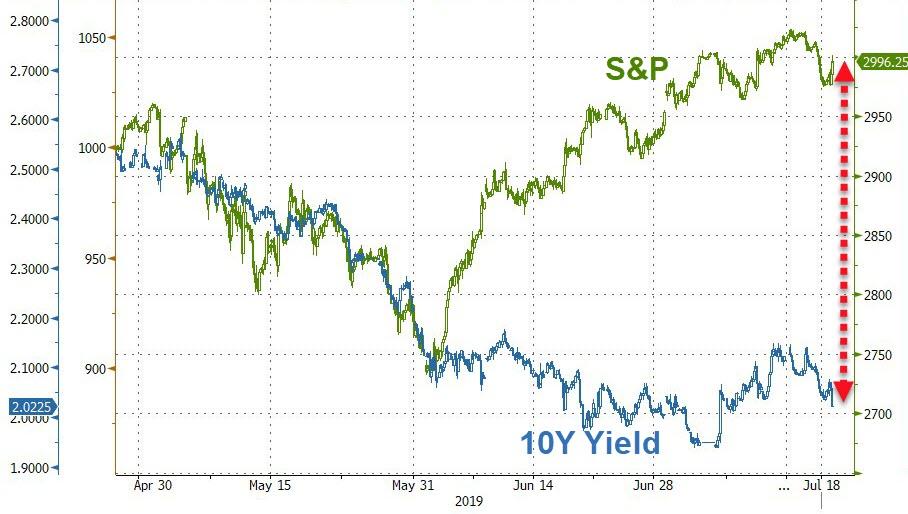

In the end, the S&P 500 failed to reclaim its recently

lost 3k marker, while the Dow barely held on to a green close. The decoupling

between the S&P 500 and the 10-year yield continues uncompromisingly, the latter

of which has been now trending

back towards the 2% level.

There was not much motivation on the part of the bulls to

engage and keep this market from fizzling. The big three, namely lack of progress

on the trade dispute with China, mixed earnings results and weak headlines for economic

numbers, combined to create a lackluster session.

In other words, the recently observed last 30-minute pump

was only a distant memory causing the major indexes, who spent most of the day

below their unchanged lines, to dive into the close. The losses were moderate, given

the recent relentless push into record territory, but it appeared that we

simply ran out of steam.

Not helping matters were Building Permits, which plummeted

the most in 3 years (-6.1% MoM) putting another nail in the coffin of weak home

sales data and mortgage applications, despite ongoing low interest rates. ZH reported

that Housing Starts followed suit and dropped -0.9% MoM (vs. -0.7% expected).

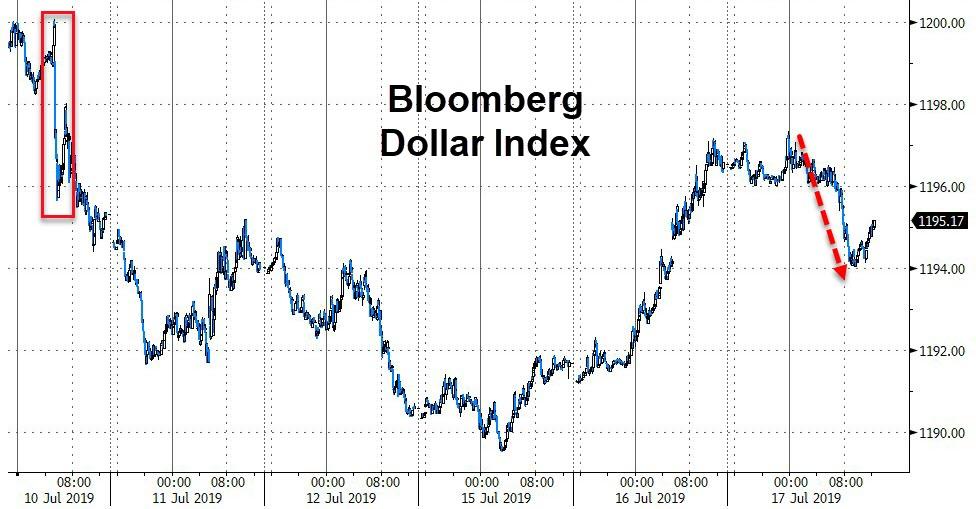

Bond yields headed lower again with the widely held 10-year

having almost made up the losses

sustained in the last week, when we hovered around the 2.14% marker, which is quite

a drop to today’s 2.06%. At the same time, the US

Dollar pulled back, while Oil continued its downward

spiral after a de-escalation of tensions with Iran.

Only about 7% of the S&P 500 companies have reported earnings

so far, so we certainly will have more surprises on deck, any of which can push

the markets in either direction.

It was a tug-of-war between news stories that kept

traders on edge with some headlines causing a sell-off, others creating a recovery,

but in the end, the major indexes closed in the red.

We didn’t see the usual last 30-minute rebound due to

Trump’s comments that “trade has a long way to go,” as well as bank earnings,

which painted a mixed picture of the economy and the financial services arena.

Fed chair Powell chimed in from a speech in France that the

“economic outlook hasn’t improved since the last FOMC meeting in June,”

which instilled hope that the stage for an interest rate cut later this month

appears to be set.

This view was crushed a little bit when June retail sales

were released. They exceeded expectations by surging 0.7% MoM, which translates

to 4.6% YoY, the most in 12 months. That ended up being a discouragement for the

low interest rate crowd. After all, if the consumer, which accounts for 67% of

GDP, is spending, why would we need a rate cut?

The loser of the day was oil prices, which tanked -2.64%

and had a wild

ride throughout the session, but in the end the administration’s

willingness to “talk to Iran,” took the starch out of the early rally and gave

the bears something to cheer about.

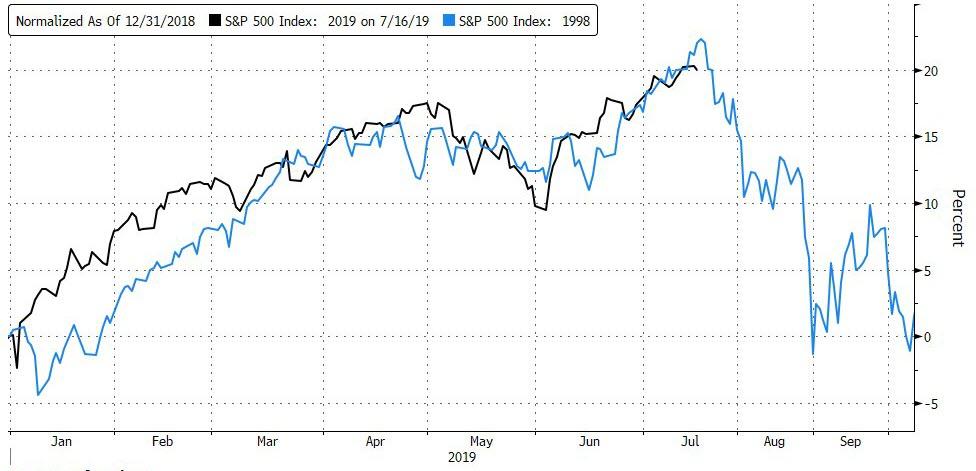

Market behavior today when compared with history may very

well be random and totally meaningless. However, it’s interesting to note the similarities

when looking at the S&P 500 in 2019 compared to 1998. A tip of the hat goes

to ZH for this

chart.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}