Below, please find the latest High-Volume ETF Cutline

report, which shows how far above or below their respective long-term trend

lines (39-week SMA) my currently tracked ETFs are positioned.

This report covers the HV ETF Master List from Thursday’s

StatSheet and includes 322 High Volume ETFs, defined as those with an average

daily volume of more than $5 million, of which currently 259 (last week 270)

are hovering in bullish territory. The yellow line separates those ETFs that

are positioned above their trend line (%M/A) from those that have dropped below

it.

In case you are not familiar

with some of the terminology used in the reports, please read the Glossary of Terms.

If you missed the original

post about the Cutline approach, you can read it here.

An early upturn hit the skids after a report

that a Chinese delegation had canceled plans to visit farms in Montana, as part

of negotiations designed to sell more farming products. Helping the positive tone

early on was news that Trump was exempting hundreds of Chinese products from

tariffs.

Things fell apart when it became known that

Trump wanted a “complete” deal and not just a temporary agreement to promote U.S.

agricultural goods. The trade mood went from bad to worse when he then added

that he “does not need a China deal before the election,” causing the Trade

Deal odds to tumble.

Even the Fed, with its current battle to control

the greatest liquidity crisis in overnight repos in over a decade, seems to be

confused, as two of its talking heads offered opposing opinions, according to

ZH:

Bullard:

Recession straight ahead!

Rosengren:

Bubbles ready to burst!

So, which is it?

That kind of split within the Fed makes me realize

that there are no certainties in the current market environment. That’s why it remains

to be of great importance to have an exit strategy in place, so we don’t get caught

on the wrong side, should things fall apart.

For the week, the major indexes slipped and

so did bond yields, which came off their recent highs with the 10-year dropping

from 1.9% to 1.73%, as this chart

shows.

We’ll have to wait and see if this softening

of bond yields is a sign of more to come, which should help equities to move out

of this week’s doldrums.

On the other hand, the Fed’s emergency

liquidity measures in the overnight lending market, if not resolved satisfactorily,

could extract a pound of flesh from equities when trading resumes next week.

ETF Data

updated through Thursday, September 19, 2019

Methodology/Use of this StatSheet:

1. From the universe of over 1,800 ETFs, I have selected only those with a

trading volume of over $5 million per day (HV ETFs), so that liquidity and a

small bid/ask spread are assured.

2. Trend Tracking Indexes (TTIs)

Buy or Sell decisions for Domestic and International ETFs (section 1 and

2), are made based on the respective TTI and its position either above or below

its long-term M/A (Moving Average). A crossing of the trend line from below

accompanied by some staying power above constitutes a “Buy” signal. Conversely,

a clear break below the line constitutes a “Sell” signal. Additionally, I use a

7.5% trailing stop loss on all positions in these categories to control

downside risk.

3. All other investment arenas do not have a TTI and should be traded

based on the position of the individual

ETF relative to its own respective trend line (%M/A). That’s why those signals

are referred to as a “Selective Buy.” In other words, if an ETF crosses its own

trendline to the upside, a “Buy” signal is generated. Since these areas tend to

be more volatile, I recommend a wider trailing sell stop of 7.5% -10% depending

on your risk tolerance.

If you are unfamiliar with some of the terminology, please see Glossary of Termsand new subscriber information in section 9.

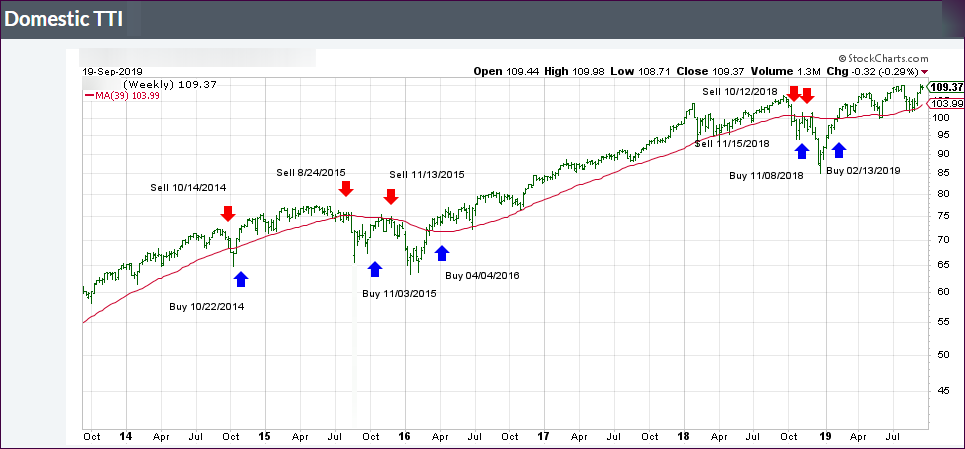

1. DOMESTIC EQUITY ETFs: BUY

— since 02/13/2019

Click on chart to enlarge

Our main directional indicator, the Domestic Trend Tracking Index (TTI-green line in the above chart) is now positioned above its long-term trend line (red) by +5.74% after having generated a new Domestic “Buy” signal effective 2/13/19 as posted.

Yesterday’s “feel good” closing

ramp carried over into today’s opening, as the major indexes were getting close

to test new record highs. Better-than-expected housing and manufacturing data

contribute to the bullish sentiment.

While the S&P 500 is

within 1% of its record closing high, it may not get there until next week due

to tomorrow’s quadruple witching day for the US markets. That means volatility

may spike as a result of the simultaneous quarterly expiration of futures,

options on indexes and stocks.

Yesterday, I mentioned the

liquidity crunch in the overnight lending market. It continued today with the Fed

promising billions of dollars to “support” the system from blowing out of control.

The liquidity shortfall rose by almost $4 billion compared to Wednesday morning.

Ouch!

We saw some fallout of that,

as the markets skidded, assisted by odds

of a China trade deal slipping, with news hitting the headlines that the

White House favors increasing some tariffs to possibly 50% or even 100%. That

took the starch out of upward momentum, and we ended up just about unchanged.

Traders are still digesting the

Fed’s rate cut, and we may not see any attempt to break through to all-time highs

until next week, although that July 2019 high may very well serve as overhead resistance.

As expected, the Fed delivered

the goods and cut rates by 0.25%; but stocks sold off. The reason was that the

accompanying language in its statement and economic projections cast doubt not

only on another rate cut this year but also in 2020. That was a disappointment

for traders, who had firmly believed that at least one more reduction prior to

December 11 was a sure thing.

However, the sell-off was mild,

and we saw another last hour pump to get the indexes to a green close, which worked

except for the Nasdaq. In the end, not much was lost or gained, as we ended up

hugging the unchanged line.

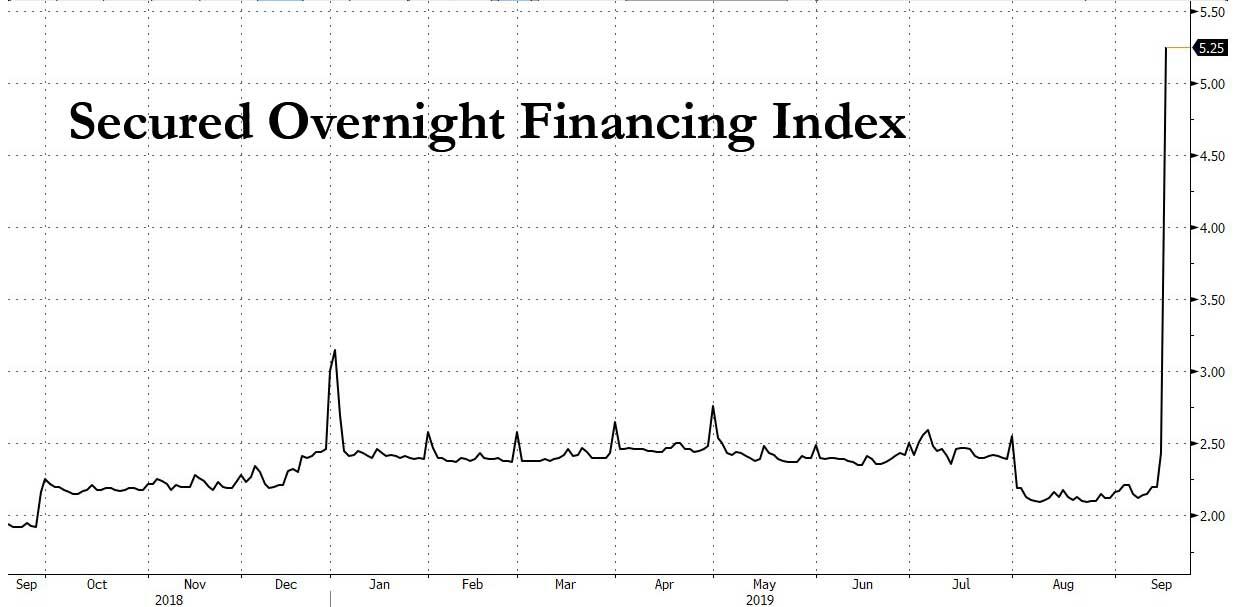

What was not addressed was

the liquidity crunch in the overnight lending market, where the Fed had to step

in and provide some $75 billion in liquidity as the Secured Overnight Financing

Index (SOFI)

spiked to 5.25% from 2.25%. This was the Fed’s first intervention in over 10 years.

These are complicated repo

transactions, which can have a dire effect on equities but have not been reported

by MSM. If this topic interests you, you can read more here

and here.

I am merely pointing this out as a fact that has been conveniently ignored by the

markets but may come back to haunt them.

The last hour rebound was a function

of Fed head Powell promising more Quantitative Easing (QE) by disguising his words

like this:

“It is certainly a possibility

that we’ll need to resume the organic growth of the balance sheet sooner than

we thought.”

What that means is that QE

is on its way, at some point, but stocks managed to joyfully jump into the close

with the S&P 500 reclaiming its recently lost 3k milestone marker.

The Fed did exactly what was

expected, but it remains to be seen if this will be enough for equities to continue

climbing the mountain towards new all-time highs.

It was a matter of treading

water for most of the day, with the major indexes limping around their respective

unchanged lines, until a last-minute pump pushed the indices up and into a

green close.

Mid-day attempts to get a rally

going fell short, as weakness in the energy sector, due to reports that Saudi

Arabia may recover sooner than expected, pulled oil off its lofty level. According

to Reuters, Saudi Arabia will restore 70% of the 5.7 million barrels a day production

lost rather quickly and the balance within the next two to three weeks.

If so, yesterday’s crude oil

spike will turn out to be an outlier with no consequences to equity markets. Traders

seemed to share that view and quickly focused their attention on the Fed and expectations

that they would reduce interest rates when they meet tomorrow.

It is a foregone conclusion that

a -0.25% ease is priced in the market, although the whisper number of -0.5% is

still making the rounds. One thing is for sure, if the Fed does not deliver a rate

cut, equities will sell off sharply. Remember, these markets are like a drug

addict that does not function very well without a regular dose of stimulus.

ZH summed it up this way:

Tomorrow’s rate cut will

come with full employment, surging inflation, record high stock prices, and near

record low interest rates.

{kind=link}

{kind=link}

{kind=link}

{kind=link}