- Moving the market

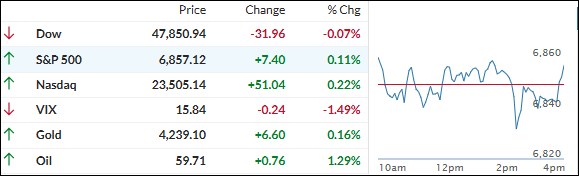

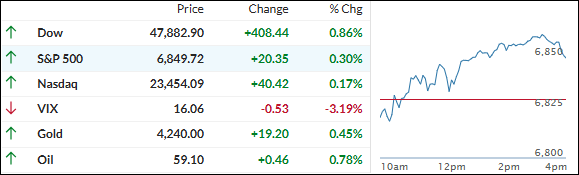

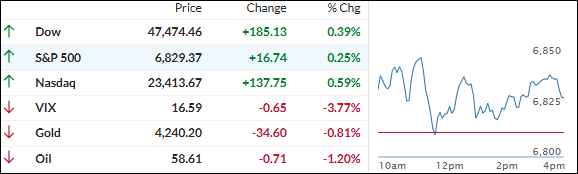

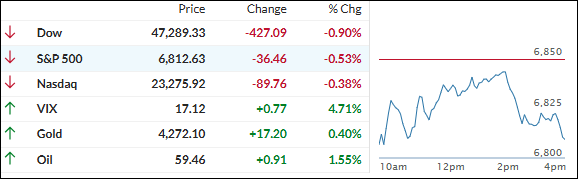

The day felt like the market was stuck in neutral—early trading was super quiet as everyone digested more signs the job market is cooling off.

The Challenger report showed U.S. companies have now announced over 1 million job cuts this year (blame restructuring, AI, and tariff worries), and yesterday’s weak ADP payrolls number added to the pile.

Traders basically shrugged at today’s weekly jobless claims hitting their lowest since September 2022 and focused on the big picture: the labor market is softening enough that a December Fed rate cut feels like a lock.

Markets are now pricing an 89% chance of a quarter-point cut next Wednesday—way up from just a couple weeks ago. That dovish vibe kept things calm, even though it was a choppy, directionless session overall.

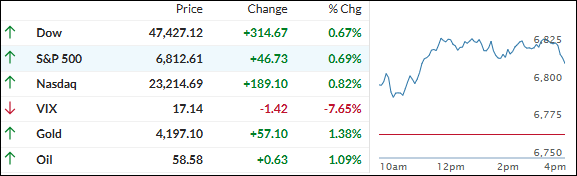

Small caps were the clear winners (short squeeze still in full swing), while the rest of the market just bounced around.

Bond yields crept higher, the dollar finished flat, gold squeaked out a tiny win and got back above $4,200, and bitcoin gave back some of its recent gains to settle around $92K.

On a brighter note, for wallets: average gas prices nationwide just dipped below $3.00/gallon for the first time since May 2021 (California folks… yeah, we’re still paying the premium).

Tomorrow, we get consumer sentiment, personal income/spending, and—most importantly—the September Core PCE number, the Fed’s favorite inflation gauge.

That one could actually move the needle.

Read More

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}