- Moving the market

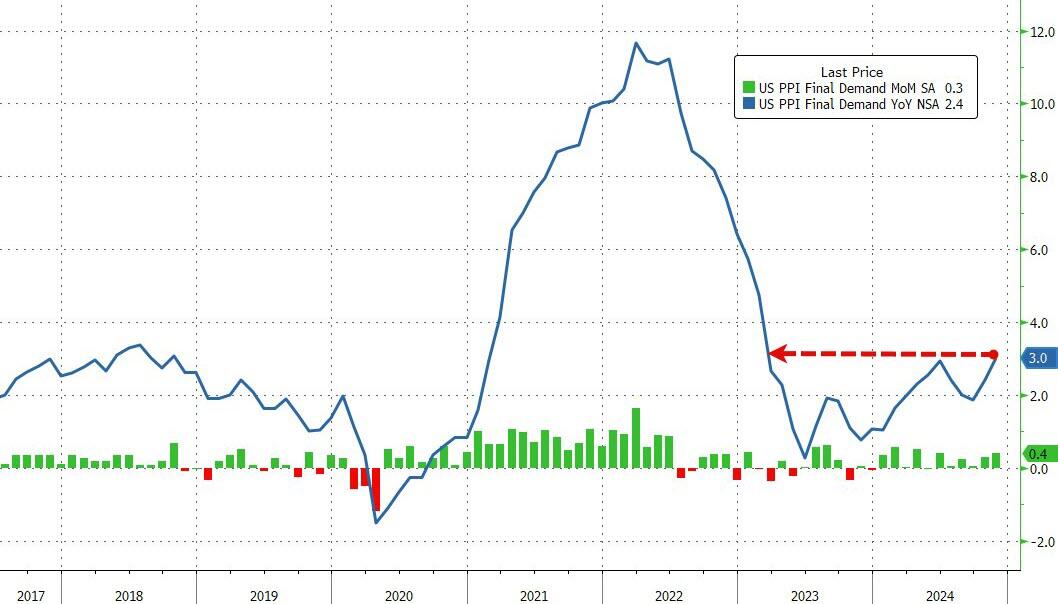

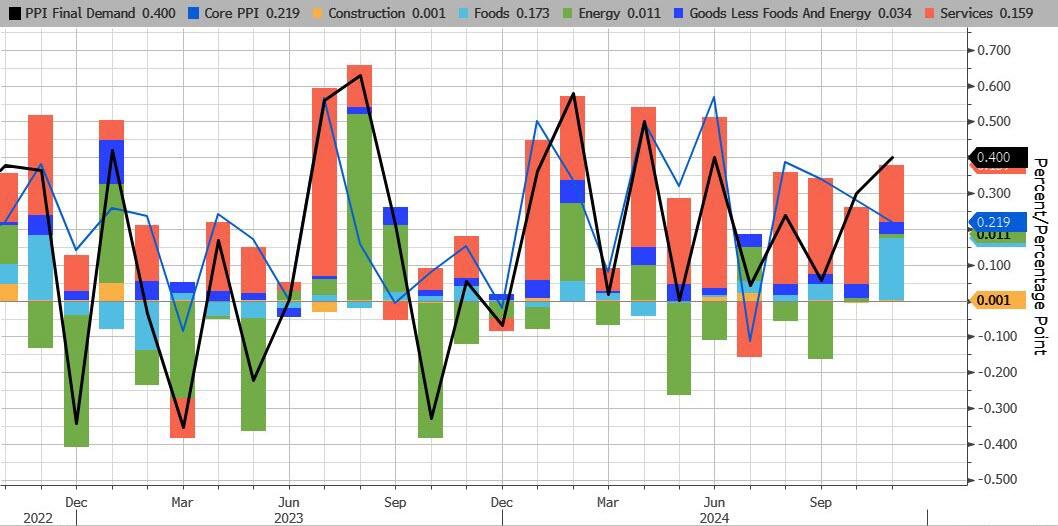

Following yesterday’s CPI report, traders were met with the release of the Producer Price Index (PPI) this morning, which showed a hotter-than-expected 0.4% price increase last month, compared to the anticipated 0.2%.

This year-over-year rise pushed prices up by 3.0%, the highest since February 2023, with food costs leading the surge, rising at their fastest pace since November 2022. The core PPI also saw a significant year-over-year increase to 3.4%, marking its worst performance since February 2023.

{kind=link}

{kind=link}

{kind=link}

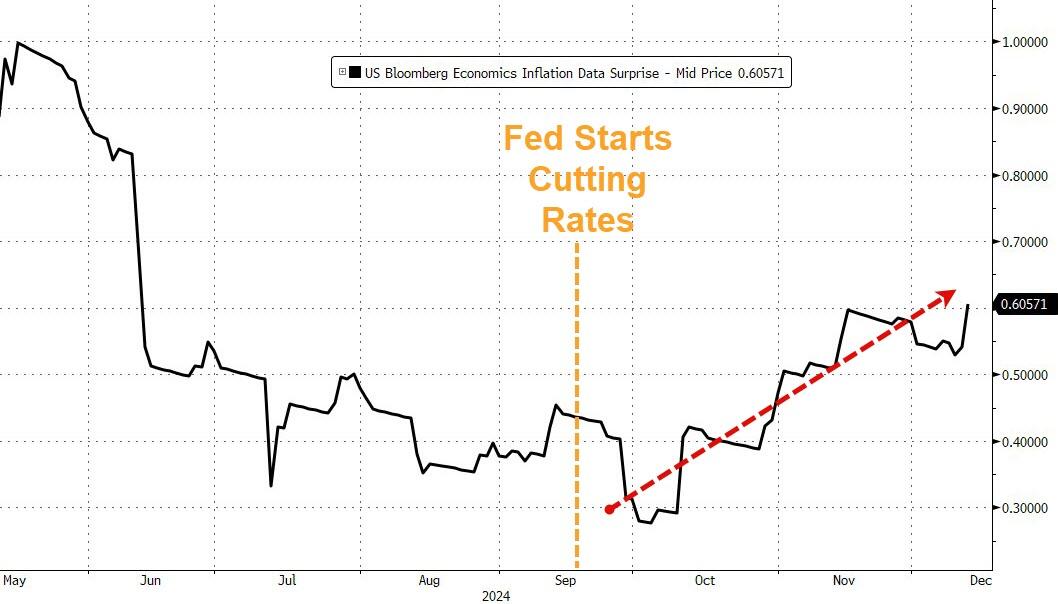

As a result, the major indexes tumbled, unable to build on the previous day’s gains. Despite this, traders remain optimistic that the Federal Reserve will proceed with a 0.25% rate cut in December, citing other recent inflation data that has shown positive trends. However, surging debt and deficits remain a concern.

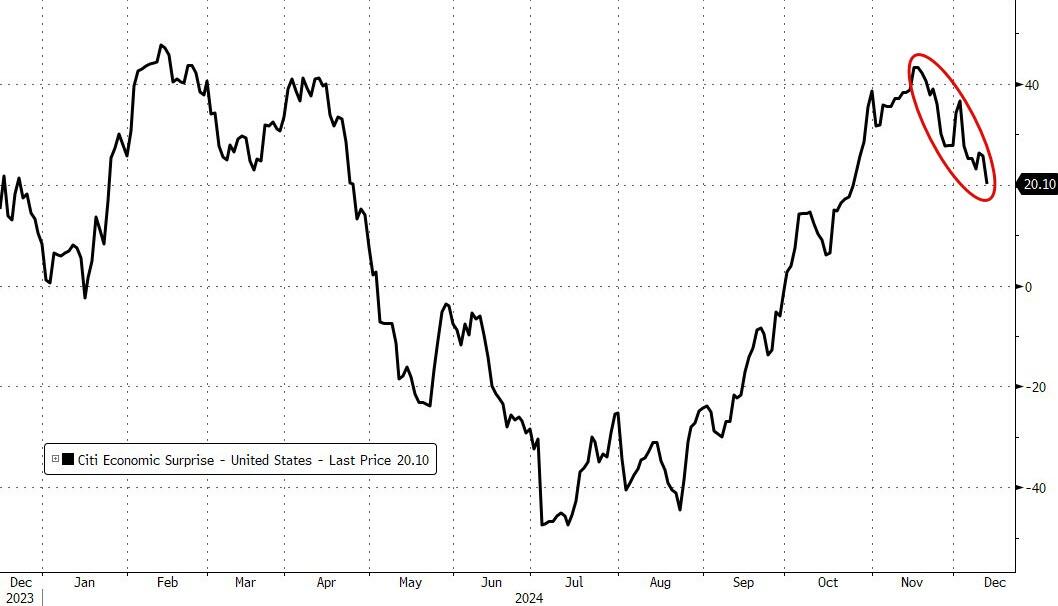

The US Inflation Data Surprise Index has been climbing since the Fed began its rate-cutting cycle, while the US Macro Surprise Index has declined amid rising jobless claims.

{kind=link}

{kind=link}

Consequently, the dollar continued its upward trajectory, while stocks, cryptocurrencies, bonds, and gold all took a hit for the day.

{kind=link}

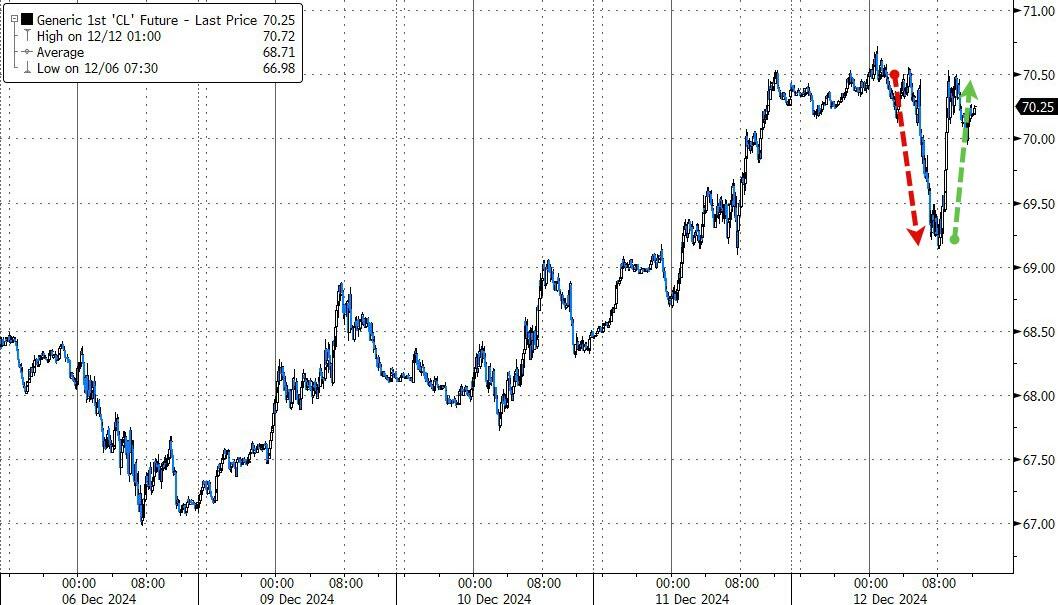

Bitcoin briefly climbed above $102,000 early in the session but fell back below the $100,000 mark. Bond yields rose, gold retreated but held its $2,700 level, and crude oil experienced volatility, ending the session slightly in the red.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Will this week’s data points influence the Fed’s upcoming decision?

2. Current “Buy” Cycles (effective 11/21/2023)

Our Trend Tracking Indexes (TTIs) have both crossed their trend lines with enough strength to trigger new “Buy” signals. That means, Tuesday, 11/21/2023, was the official date for these signals.

If you want to follow our strategy, you should first decide how much you want to invest based on your risk tolerance (percentage of allocation). Then, you should check my Thursday StatSheet and Saturday’s “ETFs on the Cutline” report for suitable ETFs to buy.

3. Trend Tracking Indexes (TTIs)

The market experienced a noticeable lack of upward momentum today, primarily due to a worse-than-expected Producer Price Index (PPI) report.

This disappointing economic data point dampened any bullish sentiment, causing the major indexes to relinquish some of the gains made in the previous session.

Our TTIs were not immune to this downturn, as both indicators experienced minor retreats.

This is how we closed 12/12/2024:

Domestic TTI: +7.14% above its M/A (prior close +7.54%)—Buy signal effective 11/21/2023.

International TTI: +4.37% above its M/A (prior close +4.70%)—Buy signal effective 11/21/2023.

All linked charts above are courtesy of Bloomberg via ZeroHedge.

———————————————————-

WOULD YOU LIKE TO HAVE YOUR INVESTMENTS PROFESSIONALLY MANAGED?

Do you have the time to follow our investment plans yourself? If you are a busy professional who would like to have his portfolio managed using our methodology, please contact me directly to get more details.

Contact Ulli