ETF Tracker StatSheet

You can view the latest version here.

SURGING BOND YIELDS SPANK EQUITIES

- Moving the markets

After yesterday’s modest bounce of hope, traders and algos alike were hit with another reality check, namely the fact that the Fed’s preferred measurement of inflation, the PCE (Personal Consumption Expenditures Price Index) rose 0.6% in January and 4.7% YoY.

That exceeded market expectations and, when combined with personal spending having soared by 1.8%, which was not only above hopes of 1.4%, but also the biggest leap since March 2021, you have a recipe for market chaos.

{kind=link}

That’s exactly what we got, as the Dow dumped some 470 points early on, but that deficit was reduced a little as dip buyers could not resist and nibbled at those bottom prices. Still, to me these numbers merely represent just another nail in the “pause or pivot” agenda, as the theme, that the Fed might suddenly turn dovish, is merely a vanishing point in the rearview mirror.

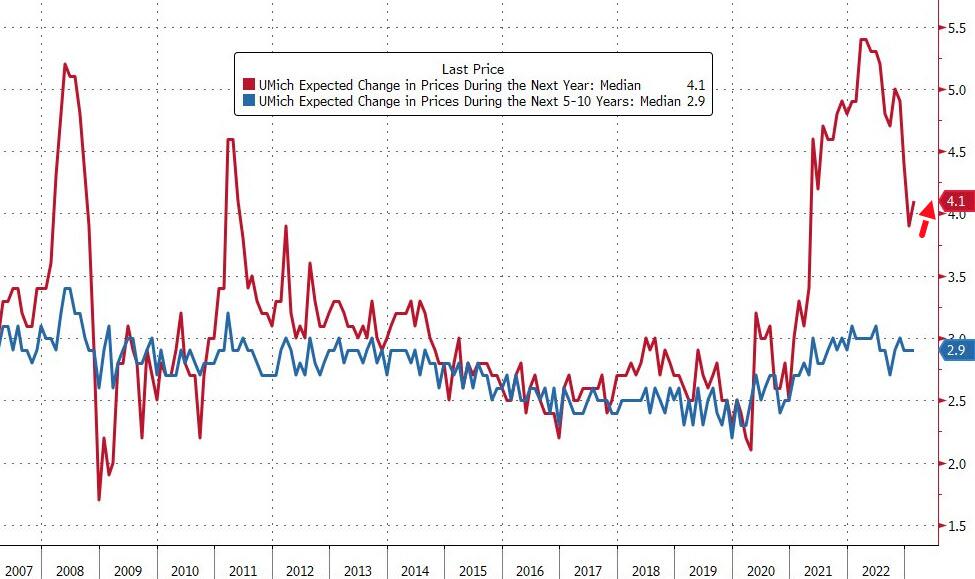

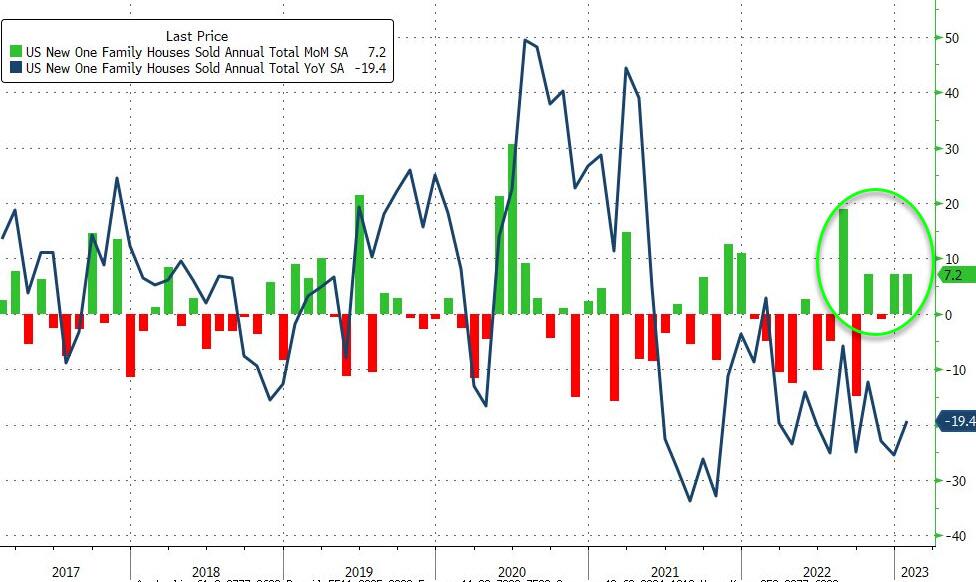

In econ news, we learned that inflation expectations rose in February, as did the Citi Economic Surprise Index. New Home Sales unexpectedly soared in January, while prices plunged.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

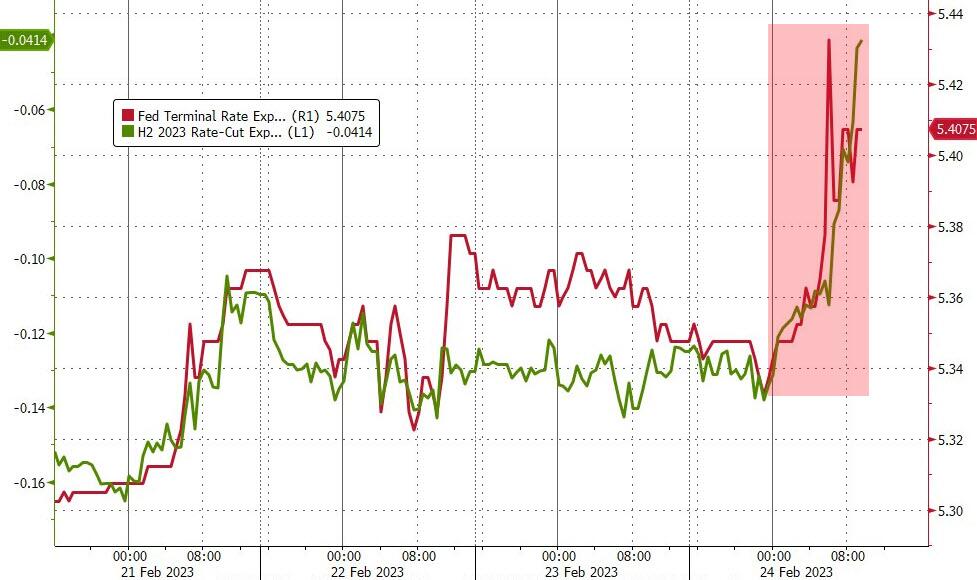

As a result, the Fed’s terminal rate propelled to a new high, as the hope for rate cuts disappeared, which is a sign that recent receding inflation numbers were nothing but transitory, and that we may now see again an increase in prices.

{kind=link}

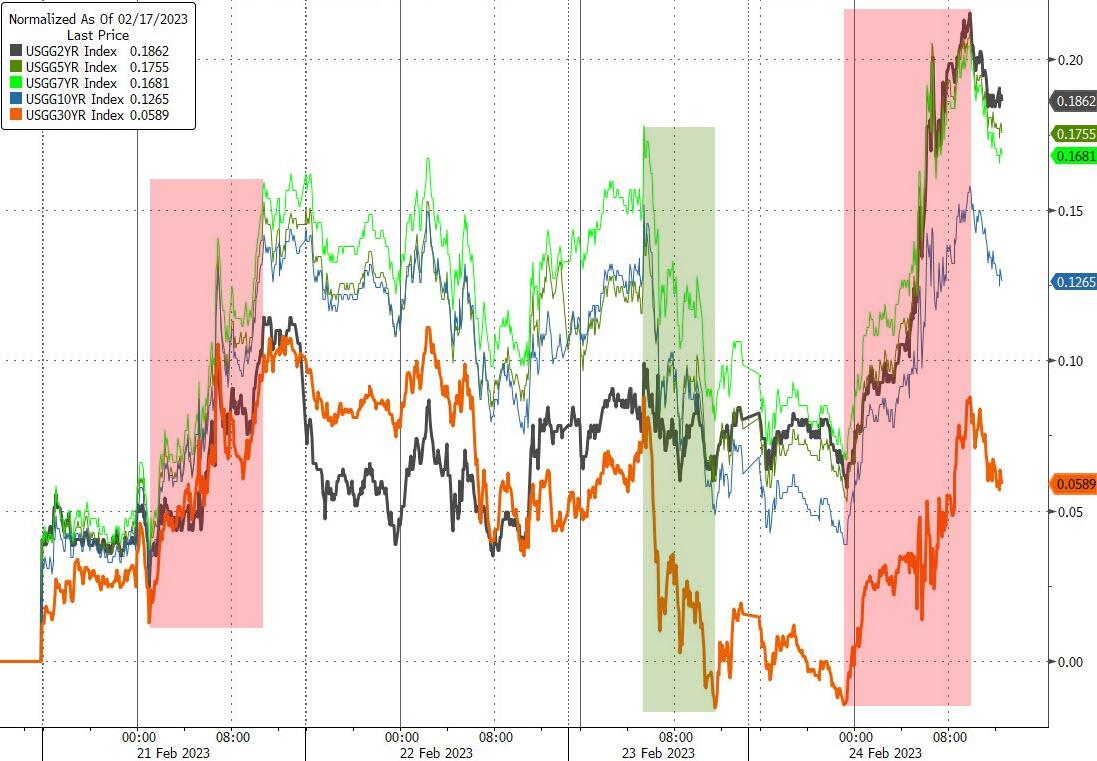

Bond yields were higher during this Holiday shortened week, with the US Dollar continuing its upswing, which now has erased all of January’s losses, a trend that was not beneficial for Gold, which, however, has managed to defend its $1,800 level.

{kind=link}

{kind=link}

{kind=link}

For the month of February, the S&P 500 has surrendered 2.6% so far, with two trading days to go. While our Trend Tracking Indexes (TTIs-section 3) have weakened as well, they still remain on the bullish side of their respective trend lines.

However, should the inflation scenario worsen, and consequently bond yields surging even higher, we must be prepared to deal with a potential sell signal in equities. For sure, I am ready to pull the trigger, if a major change in market direction necessitates such a move.

2. “Buy” Cycle Suggestions

For the current Buy cycle, which started on 12/1/2022, I suggested you reference my then current StatSheet for ETF selections. However, if you came on board later, you may want to look at the most recent version, which is published and posted every Thursday at 6:30 pm PST.

I also recommend for you to consider your risk tolerance when making your selections by dropping down more towards the middle of the M-Index rankings, should you tend to be more risk adverse. Likewise, a partial initial exposure to the markets, say 33% to start with, will reduce your risk in case of a sudden directional turnaround.

We are living in times of great uncertainty, with economic fundamentals steadily deteriorating, which will eventually affect earnings negatively and, by association, stock prices. I can see this current Buy signal to be short lived, say to the end of the year, and would not be surprised if it ends at some point in January.

In my advisor practice, we are therefore looking for limited exposure in value, some growth and dividend ETFs. Of course, gold has been a core holding for a long time.

With all investments, I recommend the use of a trailing sell stop in the range of 8-12% to limit your downside risk.

3. Trend Tracking Indexes (TTIs)

Our TTIs dropped again, as the major indexes got slammed for the week.

This is how we closed 02/24/2023:

Domestic TTI: +3.83% above its M/A (prior close +4.70%)—Buy signal effective 12/1/2022.

International TTI: +6.25% above its M/A (prior close +7.51%)—Buy signal effective 12/1/2022.

All linked charts above are courtesy of Bloomberg via ZeroHedge.

———————————————————-

WOULD YOU LIKE TO HAVE YOUR INVESTMENTS PROFESSIONALLY MANAGED?

Do you have the time to follow our investment plans yourself? If you are a busy professional who would like to have his portfolio managed using our methodology, please contact me directly to get more details.

Contact Ulli