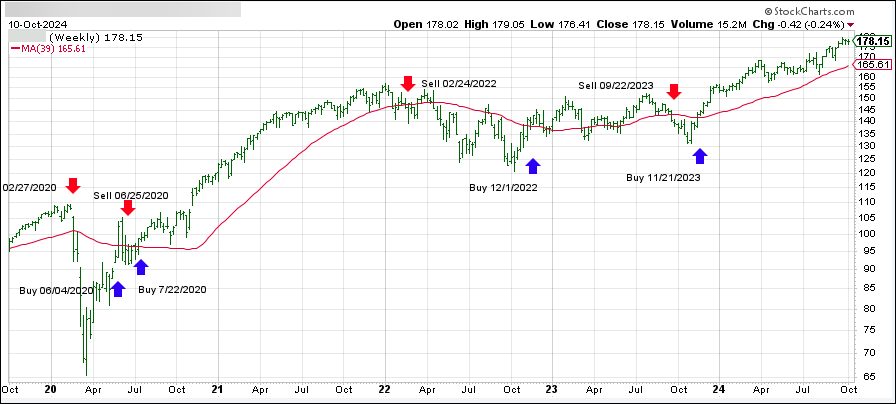

ETF Tracker StatSheet

You can view the latest version here.

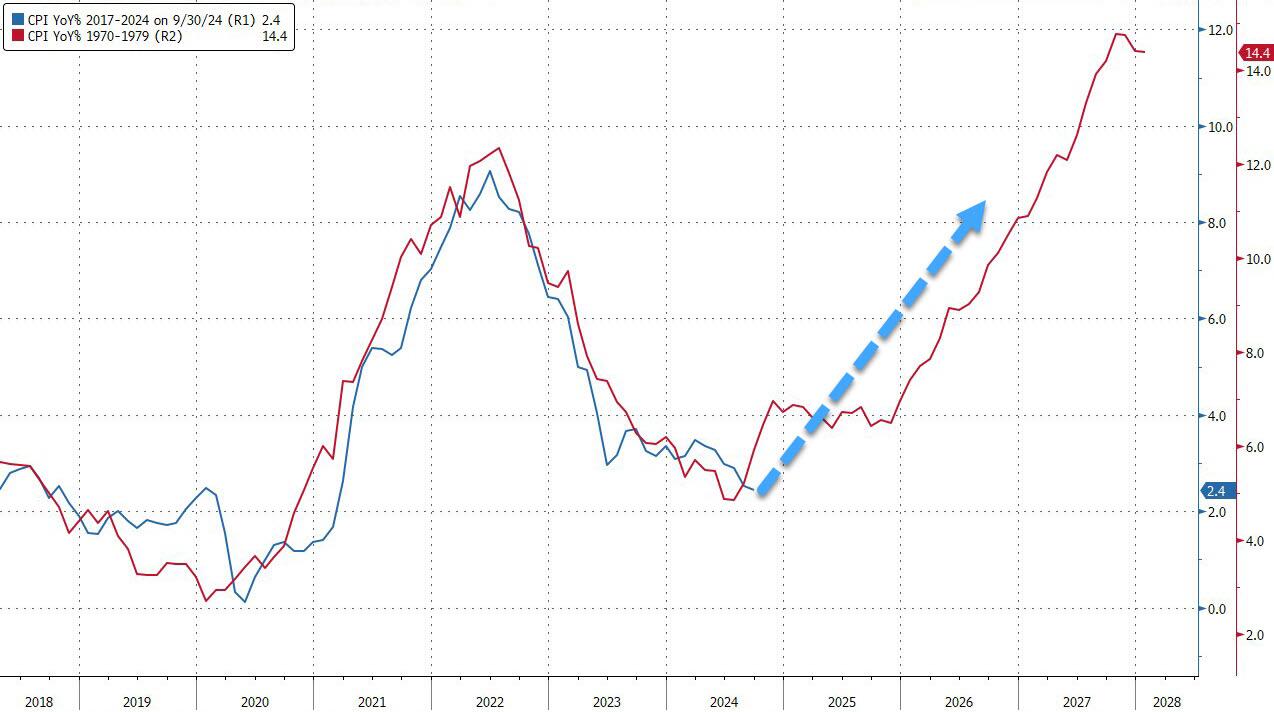

INFLATION FEARS PERSIST AS STAGFLATION LOOMS, YET MARKETS CLIMB HIGHER

- Moving the market

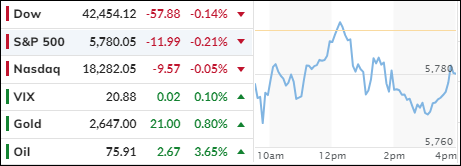

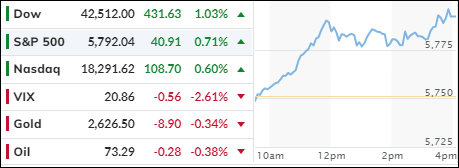

After undergoing a dip on Thursday, the major indexes regained upward momentum, with the S&P 500 not only achieving a fifth consecutive winning week but also setting a record.

However, the Nasdaq lagged, partly due to Tesla shares plummeting by approximately 7% following an underwhelming announcement about their “robotaxi.”

The start of the earnings season contributed to the positive market sentiment, as major banks exceeded profit and revenue expectations. HP Morgan advanced by 5%, while Wells Fargo surged around 6%.

The Producer Price Index (PPI) remained unchanged in September, contrary to the expected 0.1% increase, but it rose by 1.8% year-over-year, surpassing the 1.6% expectation. This temporarily alleviated some inflation concerns triggered by a higher-than-anticipated Consumer Price Index (CPI) increase. Consequently, traders are still anticipating two more 0.25% rate cuts this year.

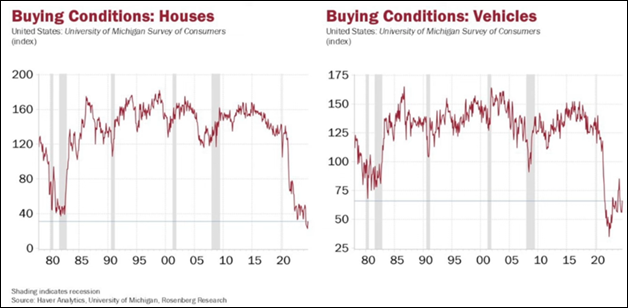

However, medium-term inflation expectations increased, as reflected in the University of Michigan’s sentiment data for October, indicating that U.S. consumers are aware that inflation will persist in various aspects of life.

Additionally, the specter of stagflation has reemerged, with inflation rising and macroeconomic growth data declining. Despite these challenges, computer algorithms continued to drive stocks higher. Even the 10-year bond yield approaching 4.10% did not dampen bullish enthusiasm.

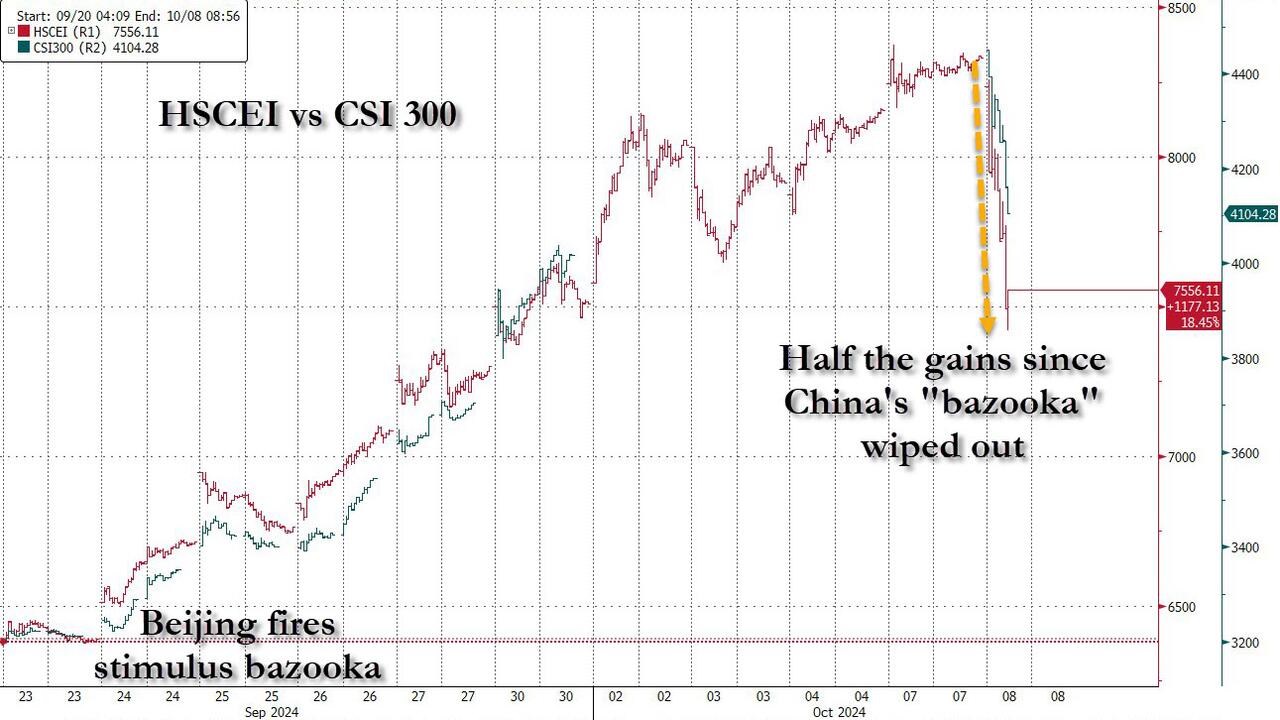

Heavily shorted stocks experienced significant short squeezes, while Chinese markets remained in turmoil due to government crackdowns, leading to an exodus of foreign investors.

Bond yields were mixed for the day, but the long end rose for the week. The dollar rallied for the second consecutive week but pulled back towards the close. Gold rebounded from Wednesday’s lows but fell short of its $2,700 target.

Crude oil traded sideways but managed to post a weekly gain. Bitcoin surged, reaching the $63,000 level.

Will Bitcoin continue to follow the direction of liquidity as shown in this chart?

Read More

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}