- Moving the market

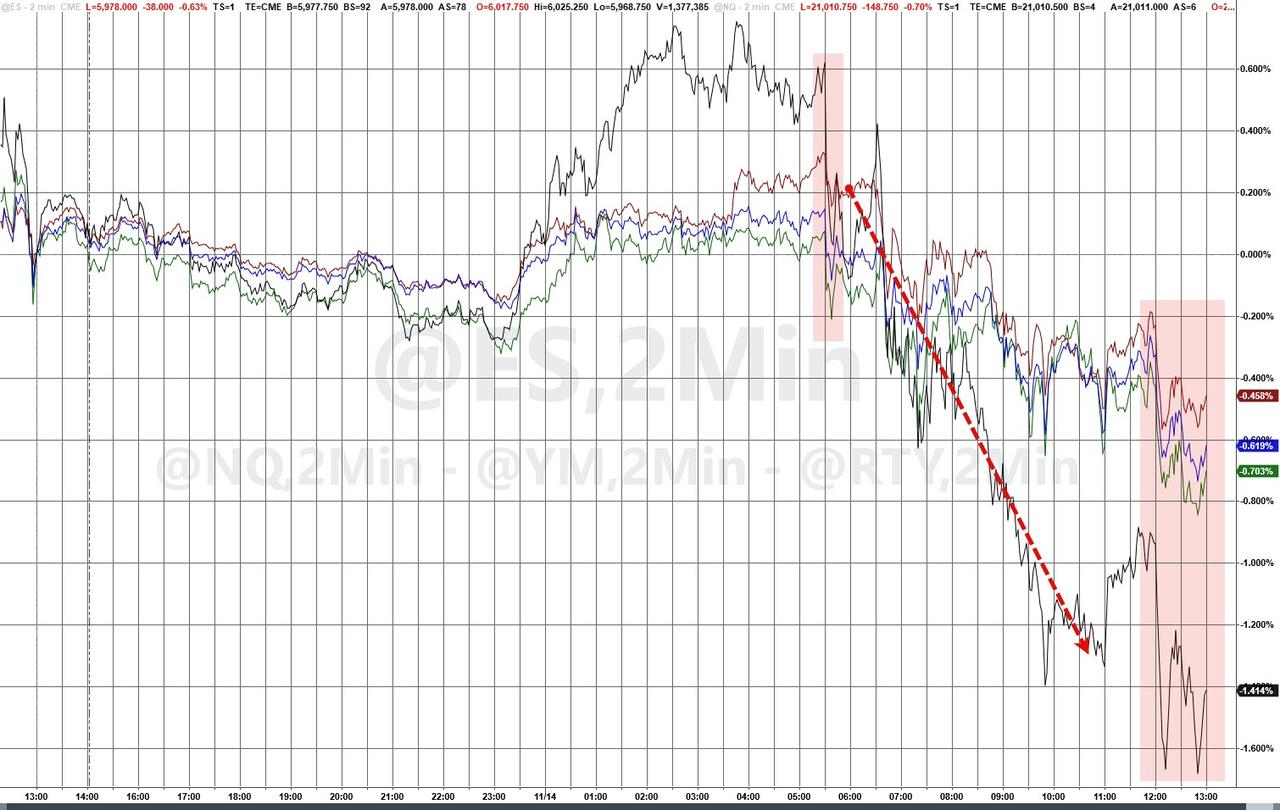

The rally in stocks and cryptocurrencies came to a halt and reversed as traders grappled with recent record highs, shifting their focus to the October Producer Price Index (PPI).

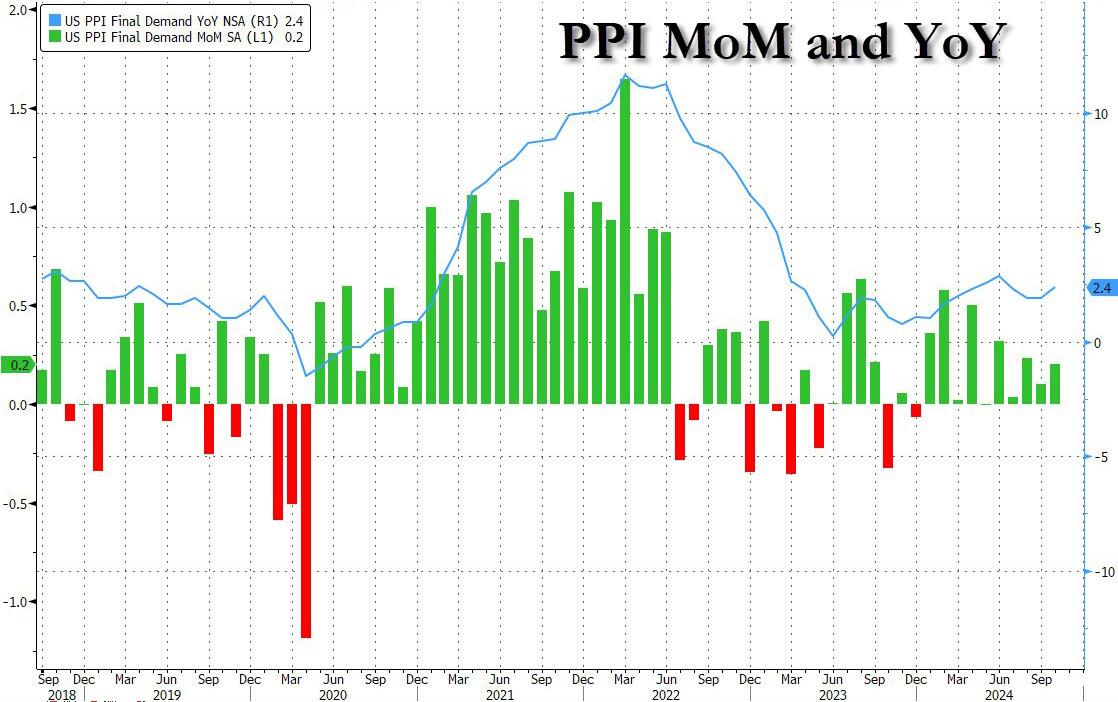

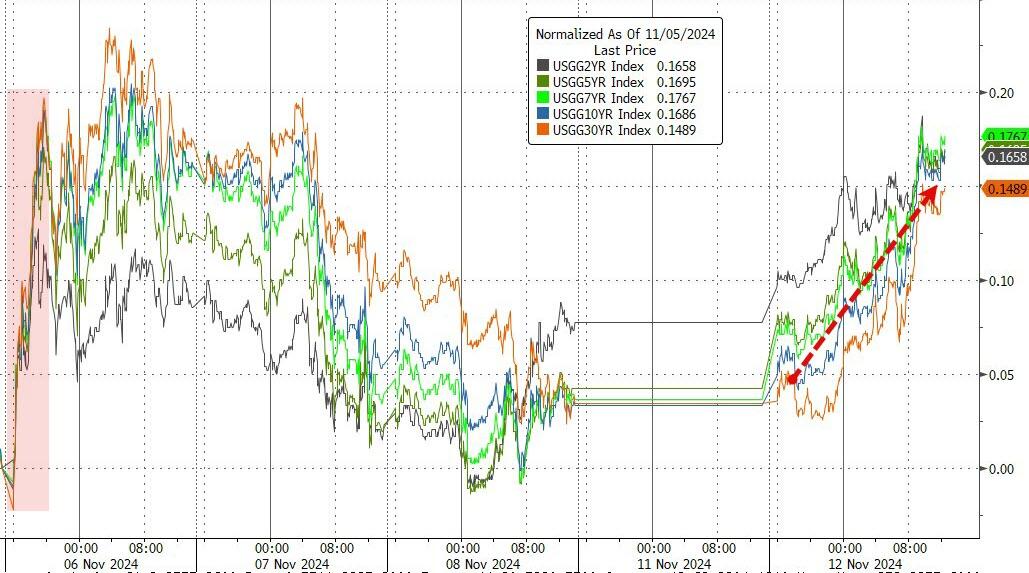

The PPI headline number matched forecasts with a 0.2% month-over-month increase, while September’s figure was revised upward from 0.0% to 0.1%. On an annual basis, the PPI rose by 2.4%, surpassing the expected 2.3%, with the previous month’s figure also revised higher from 1.8% to 1.9%.

These figures indicate that inflation is not moving towards the Federal Reserve’s 2% target but rather in the opposite direction, prompting traders to question the likelihood of a December rate cut.

This data reinforces my belief that inflation is far from over and may worsen, potentially leading to the much-dreaded condition of stagflation.

JP Morgan CEO Jamie Dimon echoed these concerns, stating:

– *DIMON: THINK THE CHANCE OF SOFT LANDING LESS THAN OTHERS THINK

– *DIMON: “NOT SO OPTIMISTIC” THAT INFLATION WILL GO AWAY QUICKLY

– *DIMON: GROWTH IS BEST POLICY TO FIX DEFICIT PROBLEM

– *DIMON: TRUMP INHERITING INFLATION THAT MAY NOT GO AWAY QUICKLY

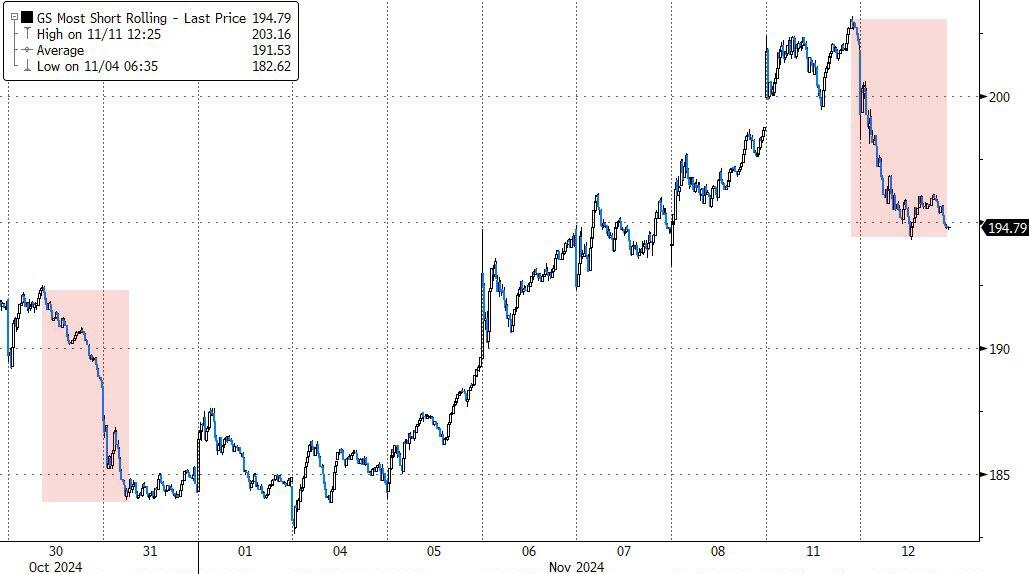

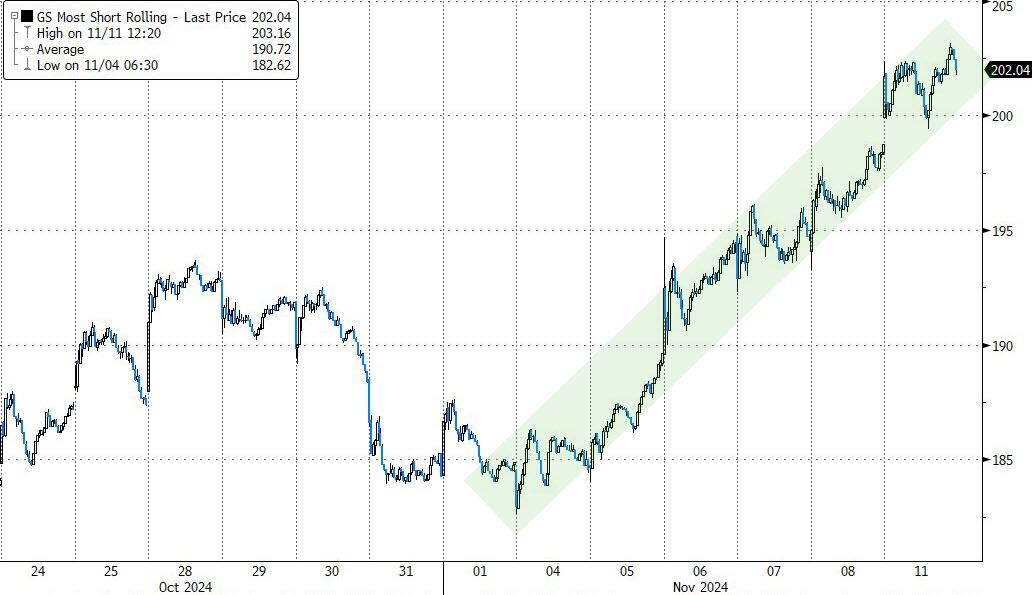

Federal Reserve Chair Jerome Powell also acknowledged in his remarks that “the Fed is in no hurry to cut rates… and inflation is on a bumpy path.” Powell’s comments accelerated the market downturn, with small-cap stocks bearing the brunt of the sell-off as heavily shorted stocks were pushed lower, erasing recent gains.

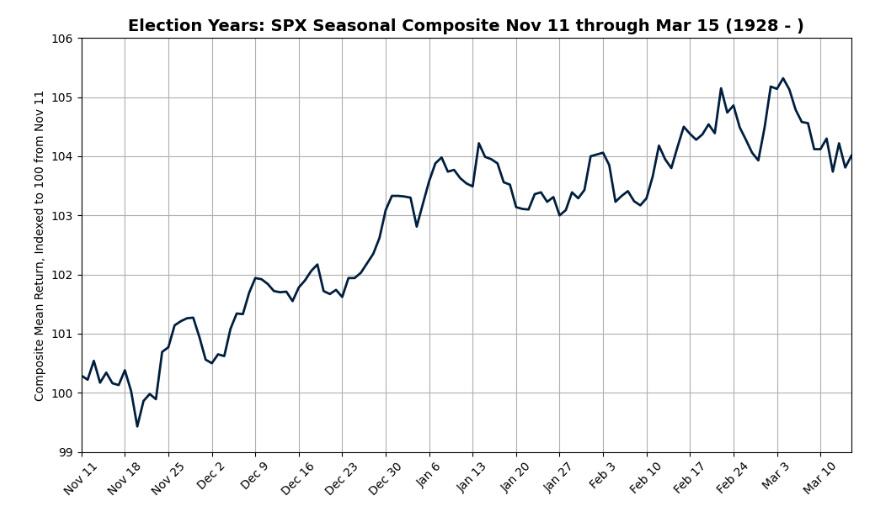

Despite this, traders are holding onto historical seasonality patterns, which suggest a rally into the inauguration during election years, followed by a peak in February.

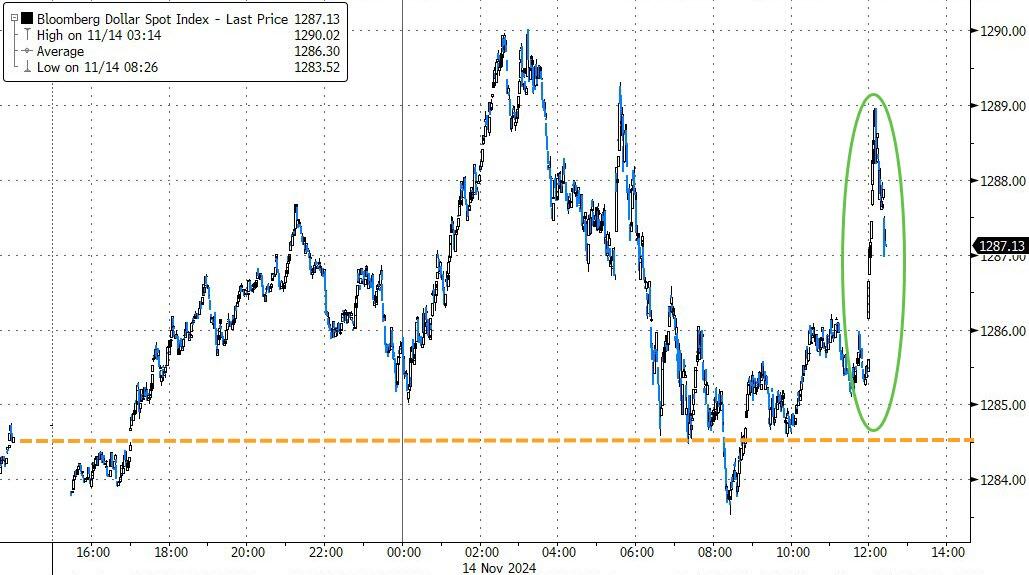

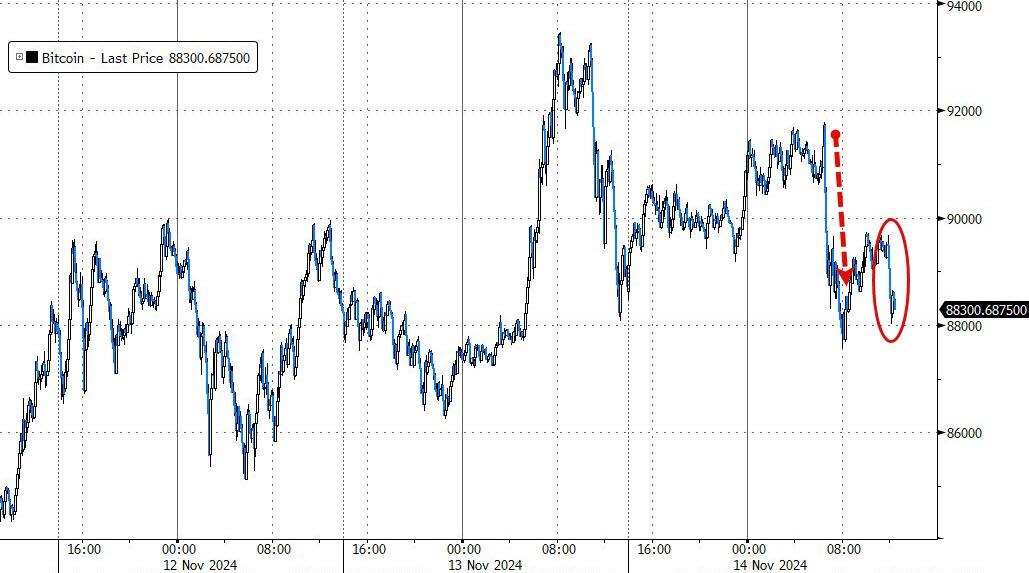

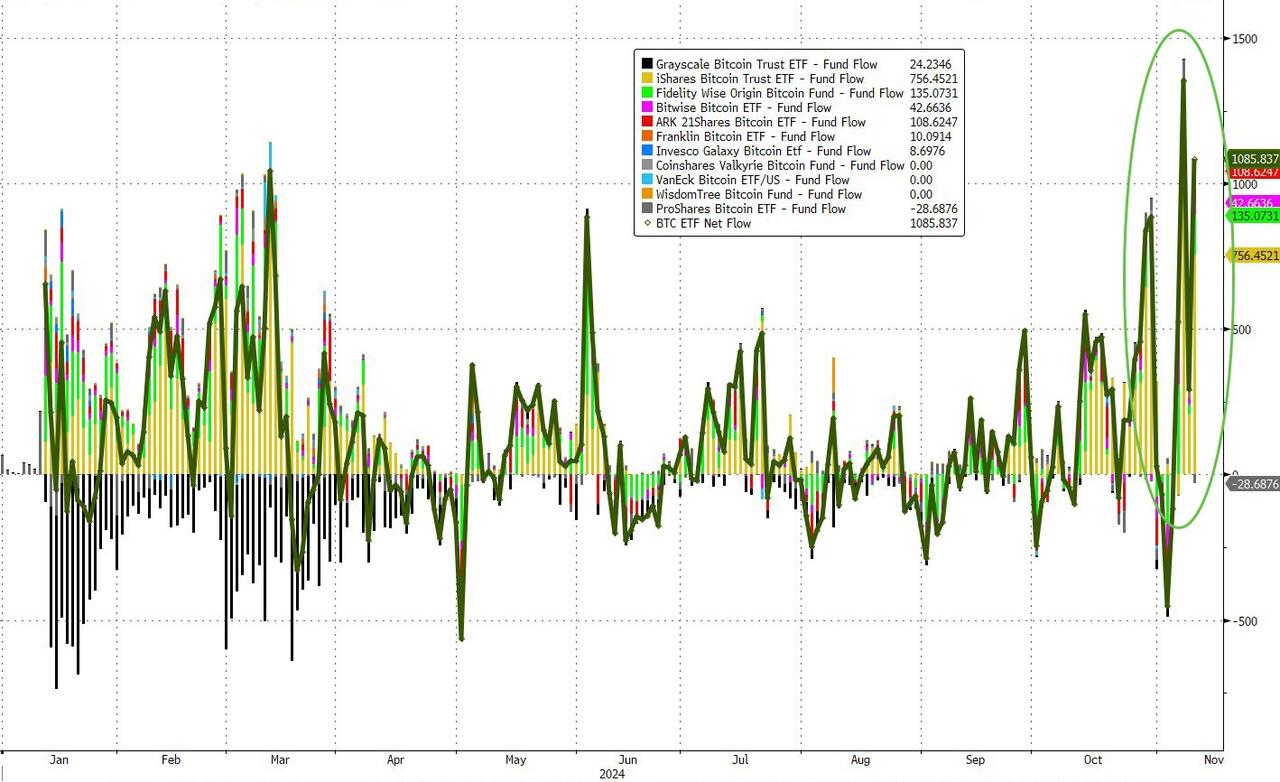

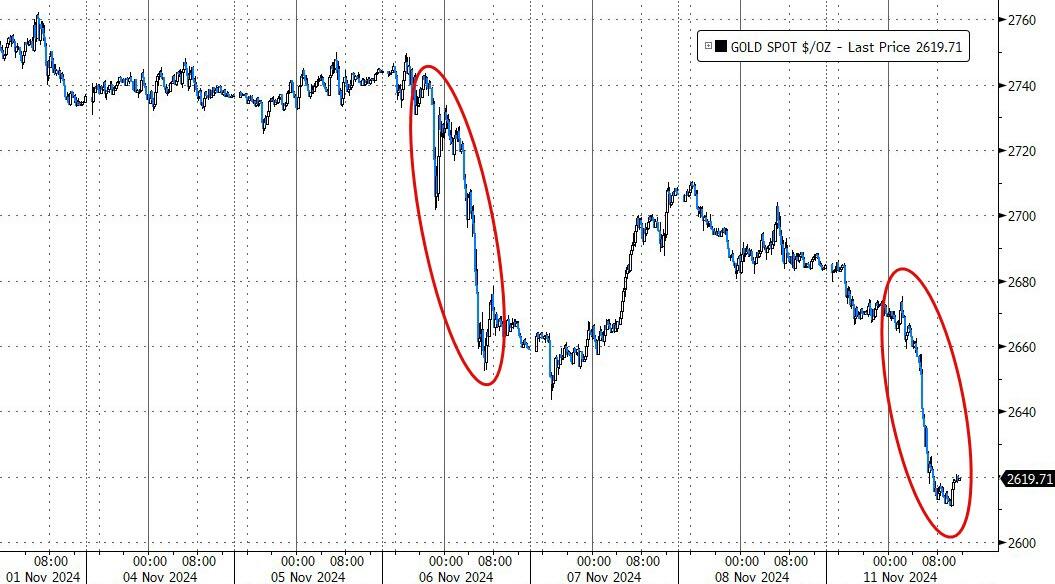

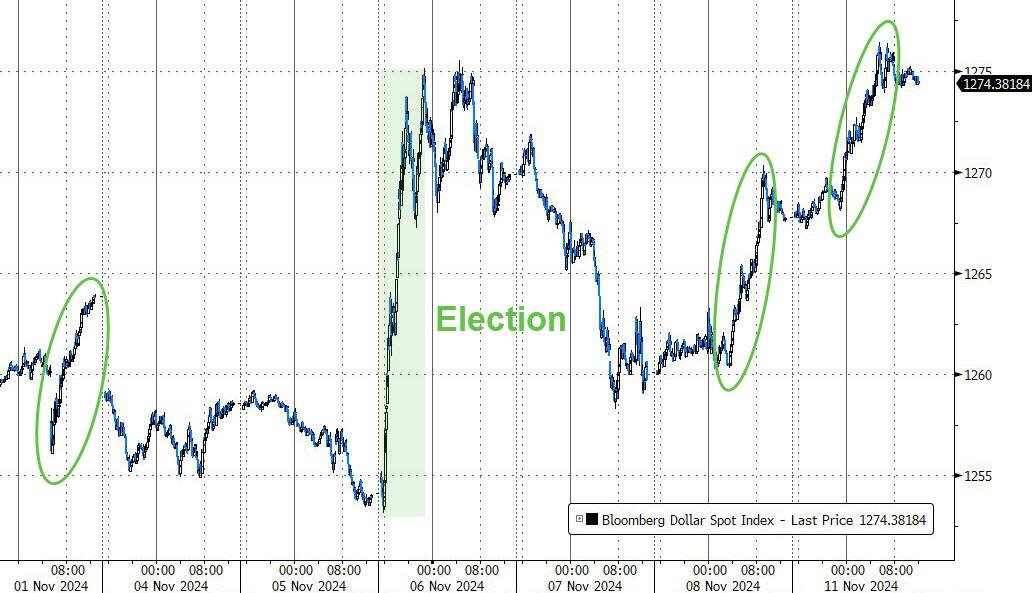

The dollar rebounded after a midday slump, as did gold, although the precious metal slipped again. Bitcoin, after an early bounce, found support at the $88,000 level.

Will tomorrow’s retail sales report add even more volatility to the markets?

Read More

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}