- Moving the markets

The November Fed minutes revealed that a rate hike was on the horizon, but the path from then on forward was uncertain and that “monetary policy in 2019 was not on a pre-set course.” Additionally, it was made clear that the expectation of 3 hikes was “flexible” and could change, if the economic picture shifted dramatically.

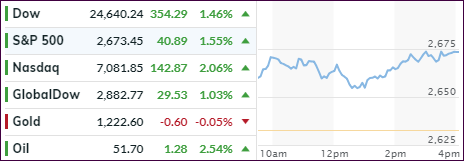

Nothing new there, but the markets took it as less uncertainty than we had prior to yesterday’s announcement, and see-sawed around the unchanged line all day before closing slightly in the red.

Still, the indexes have now recovered to where they are hovering at critical levels with their key moving averages. That simply means that these levels could serve as resistance points or, if broken solidly, as a base for new advances and a break back into bullish territory.

Headline news will likely make that decision, as words like G-20, Fed, Trump and Trade are the ones that will affect market direction soon. Interest rates took a dive with the 10-year bond yield dropping below the 3% level for the first time since the middle of September, before rallying off that point to close at 3.03%. That is an amazing collapse in yields when considering that earlier this month we were at 3.24%.

This makes me wonder if economic conditions are as solid as advertised, because if they were, yields would continue to rise and not drop. Consider, we have a plunge in pending home sales to the weakest in 5 years, jobless claims soaring to 8-month highs, while some car manufacturers are closing plants and laying off workers. These are signs of weakening conditions that may need an assist from the Fed in form of lower rates. Is that why the Fed showed a softer “dovish” side yesterday?

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}