Below, please find the latest High-Volume ETF Cutline

report, which shows how far above or below their respective long-term trend

lines (39-week SMA) my currently tracked ETFs are positioned.

This report covers the HV ETF Master List from Thursday’s

StatSheet and includes 322 High Volume ETFs, defined as those with an average

daily volume of more than $5 million, of which currently 274 (last week 250)

are hovering in bullish territory. The yellow line separates those ETFs that

are positioned above their trend line (%M/A) from those that have dropped below

it.

In case you are not familiar

with some of the terminology used in the reports, please read the Glossary of Terms.

If you missed the original

post about the Cutline approach, you can read it here.

The hope that Amazon’s earnings report would

provide the firepower to propel the markets into record territory proved to be

false, as the behemoth showed its first profit drop in two years, causing its

stock to subsequently take a dive of some 8% in yesterday’s afterhours trading.

With that horse being out of commission,

traders and algos needed a new driver to push the slow crawl of the indexes towards

all-time highs into overdrive. That turned out to be the latest headlines

promoting that “US and China are near completion of some aspects of the

phase one trade

deal that was supposed to be all papered last week.”

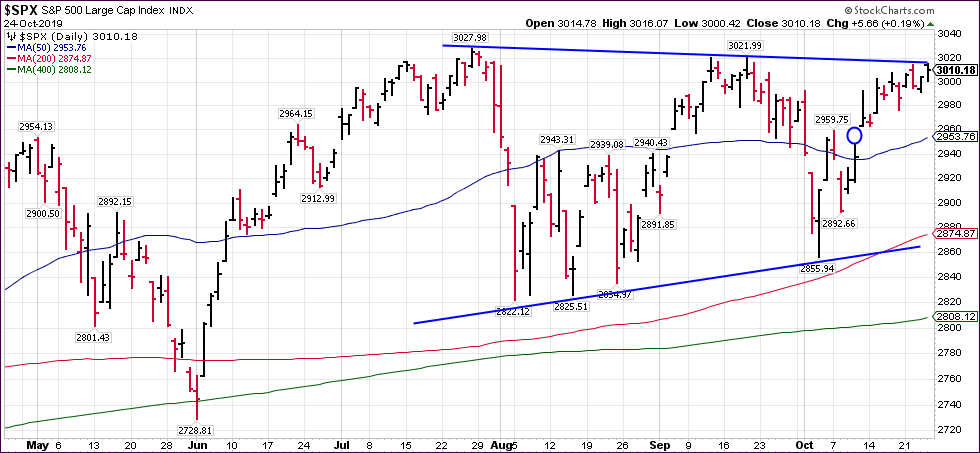

It worked, and the S&P 500 broke through

overhead resistance in pursuit of the all-time intra-day level of 3,027.98, which

it failed to conquer, but it managed to take out the previous closing high of 3,025.86

for a few minutes before pulling back. Giving an assist was the biggest

short-squeeze in 6 weeks, which has been helping markets without many interruptions

since the beginning of September.

For sure, any positive signs of either the existing

US-China tariffs being suddenly dropped, or the actual signing of the phase 1

trade deal, will send global stocks higher.

Today’s move only required the S&P to

gain less than 0.5% to touch new all-time highs. This happened in the face of rising

bond yields, which gave the S&P 500 (SPY) the edge (+0.41%) over its low volatility

cousin SPLV, which slid for the second day (-0.57%). Still, for this current ‘Buy’

cycle, SPLV remains the dominant force by having gained +12.76% vs. SPY’s 9.67%.

As far as market participants is concerned,

next week’s Fed meeting on interest rates is a shoo-in and already a foregone

conclusion. I only expect a strong market reaction, if they don’t cut

(negative), or if they cut more than expected (positive).

Never mind that the US budget deficit for

fiscal 2019 came in at almost $1 trillion ($984.4 billion to be exact), which

was a whopping increase of 26.4% over the prior year, nor that US

Economic Policy Uncertainty has soared to all-time record highs. Stocks are

in their own world and appear to be climbing a wall of worry.

ETF Data

updated through Thursday, October 24, 2019

Methodology/Use of this StatSheet:

1. From the universe of over 1,800 ETFs, I have selected only those with a

trading volume of over $5 million per day (HV ETFs), so that liquidity and a

small bid/ask spread are assured.

2. Trend Tracking Indexes (TTIs)

Buy or Sell decisions for Domestic and International ETFs (section 1 and

2), are made based on the respective TTI and its position either above or below

its long-term M/A (Moving Average). A crossing of the trend line from below

accompanied by some staying power above constitutes a “Buy” signal. Conversely,

a clear break below the line constitutes a “Sell” signal. Additionally, I use a

7.5% trailing stop loss on all positions in these categories to control

downside risk.

3. All other investment arenas do not have a TTI and should be traded

based on the position of the individual

ETF relative to its own respective trend line (%M/A). That’s why those signals

are referred to as a “Selective Buy.” In other words, if an ETF crosses its own

trendline to the upside, a “Buy” signal is generated. Since these areas tend to

be more volatile, I recommend a wider trailing sell stop of 7.5% -10% depending

on your risk tolerance.

If you are unfamiliar with some of the terminology, please see Glossary of Termsand new subscriber information in section 9.

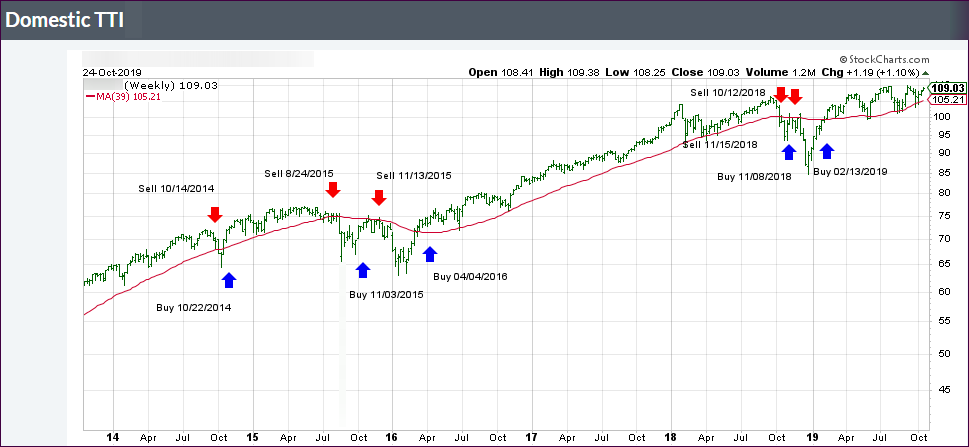

1. DOMESTIC EQUITY ETFs: BUY

— since 02/13/2019

Click on chart to enlarge

Our main directional indicator, the Domestic Trend Tracking Index (TTI-green line in the above chart) is now positioned above its long-term trend line (red) by +3.94% after having generated a new Domestic “Buy” signal effective 2/13/19 as posted.

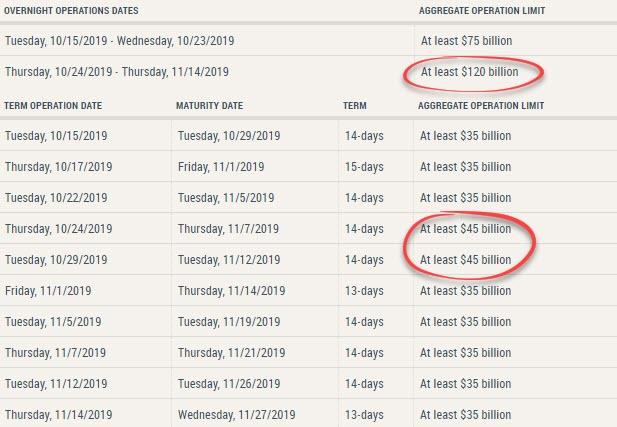

Yesterday’s last-minute pump,

to get the major indexes to a green close, finally made sense, when it became

known that the Fed had injected $134 billion in liquidity in the repo markets.

This event sparked a furious last hour rally, which ZH charted like this.

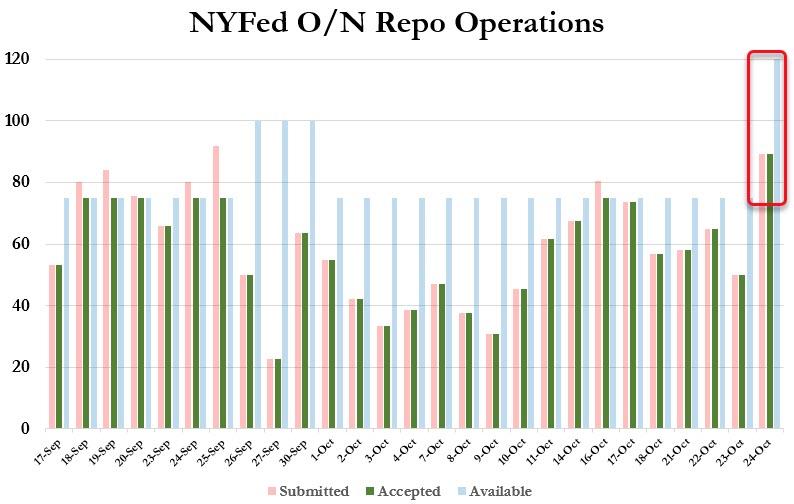

As the table shows, the

increase in liquidity

availability for overnight repos was increased from $75

billion to $120 billion, while term repos jumped from $35 billion to $45

billion. The overnight repo

was the biggest ever, which again begs the questions “what is broken?” and “will

it go exponential?”

Added ZH:

The only possible

explanation, is someone really needed to lock in cash for month end (the

maturity of the op is on Nov 7) which is when a “No Deal” Brexit may

go live, and as a result one or more banks are bracing for the worst. The

question, as before, remains why: just what is the source of this unprecedented

spike in liquidity needs in a system which already has $1.5 trillion in excess

reserves? And while we await the answer, expect stocks to close pleasantly in

the green as dealers transform their newly granted liquidity into bets on risk assets.

These are serious issues

with potentially significant repercussions for equity markets, which so far

have simply shrugged off this event. In my view, this will not end well…

However, for the time being,

the major indexes continued their aimless meandering around their respective unchanged

lines with a bullish bias, as headline earnings reports provided a mixed

picture.

MarketWatch featured these

highlights:

Microsoft’s stock surges as

big earnings beat prompts analysts to boost price targets

Twitter stock tumbles 20% after

company says advertising bugs weighing on earnings

Comcast’s stock surges after

profit, revenue rise above expectations

Nokia’s stock plummets toward

worst day in 19 years on heavy volume after profit warning

On the economic side, things

did not look encouraging with US New Home Sales slowing in September, as prices

plunged to their lowest since 2017. Not to be outdone, the Durable Goods report

showed that orders tumbled last month, while Business Investment contracted the

most since Trump’s election.

Still, it looks to me that

traders and computer algos are eagerly awaiting Amazon’s earnings, due out

after the close today. If expectations are solidly beat, this may provide

enough optimism/firepower to propel the indexes into all-time

high territory, which is not a big deal, since we have been

hovering within striking distance (around 1%) for a while.

Despite disappointing results

from Boeing and Caterpillar, the markets managed an early ramp higher but were

not able to sustain it, as a slow deterioration of upward momentum pulled the

major indexes back below the unchanged line.

Traders had one eye on the

Brexit developments, where the latest parliamentary vote eased concerns about

the UK busting out of the EU without a deal by October 31st.

Looking at the big picture,

this week is all about earnings with next week’s highlight being the Fed

meeting on interest rates. Even though 82.7% of S&P companies have delivered

results above expectations, let’s not forget that these expectations have been

sharply reduced.

Companies are further justifying

these numbers by elaborating that “how we did this quarter isn’t as

important as what we expect the future to hold.” Yeah, right.

With the Fed’s money printing

going into overdrive at the rate of some $60 billion a month, it’s no wonder that

Central Banks around the world have been accumulating gold at a record pace. Today,

we learned that my home country, Germany, has joined the party by openly buying

gold into its reserve holdings—for the first time in 21 years.

That is not surprising, as

Germany has more experience with the awful effects of too much money printing than

any other industrialized nation. If you are not familiar with that part of history,

please read more about the Weimar

Republic.

Combining the ECB policies along

with Deutsche Bank’s (one of the largest derivatives holders in the world) precipitous

demise, fears of a looming financial crises have become a possibility for the Germans

and have subsequently caused this renewed interest in gold.

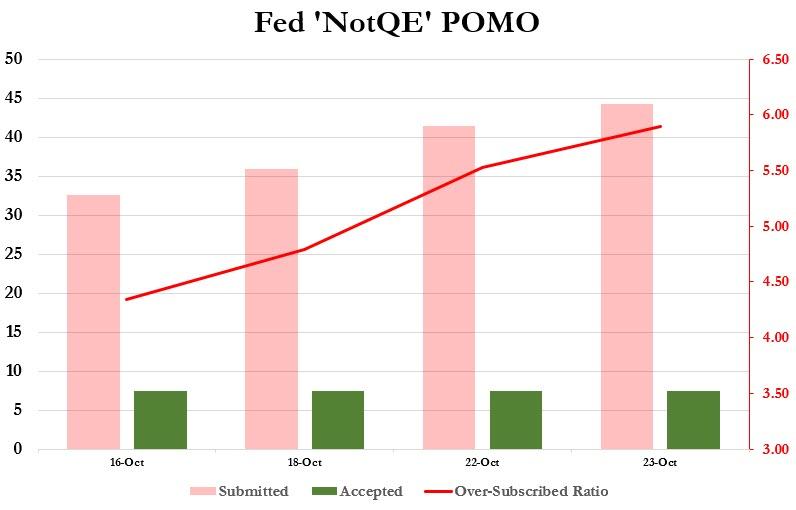

Here in the US, the liquidity

scramble in the overnight repo market continues, as the latest operation was oversubscribed

5.9 times. As ZH pointed out, it simply means that the demand for the Fed’s permanent

liquidity injection is increasing with every operation.

How long can that go on before

we go exponential? And just as important, how long can this go on before equity

markets realize that not all is well with the financial plumbing?

Be that as it may, at least

for today, the major indexes moved aimlessly and looked to end up at their

respective unchanged lines when a last-minute pump assured a green close.

It sure was a day consisting

of mixed reports and, as much as I searched, I could not find a reason that might

have supported the early rally. Of course, the latest earnings reports took

center stage, but it seemed the disappointing results from McDonalds, Travelers

and UPS were overpowering the positive ones.

With the markets failing to

break out, after having reached the upper limit

of their 3-month trading range, this may change when tech behemoth Amazon releases

its results on Thursday. Analysts are looking for “a solid beat” and a subsequent

move of the major indexes not just above the current glass ceiling but also into

new record-high territory.

With traders’ focus being on

a breakout, almost no one talks about far more concerning issues, namely the

continued stress, strain and funding squeeze in the overnight lending markets (repos).

It’s a very complex issue that boils down to the fact that banks have trouble

securing funds due to a shortage in liquidity.

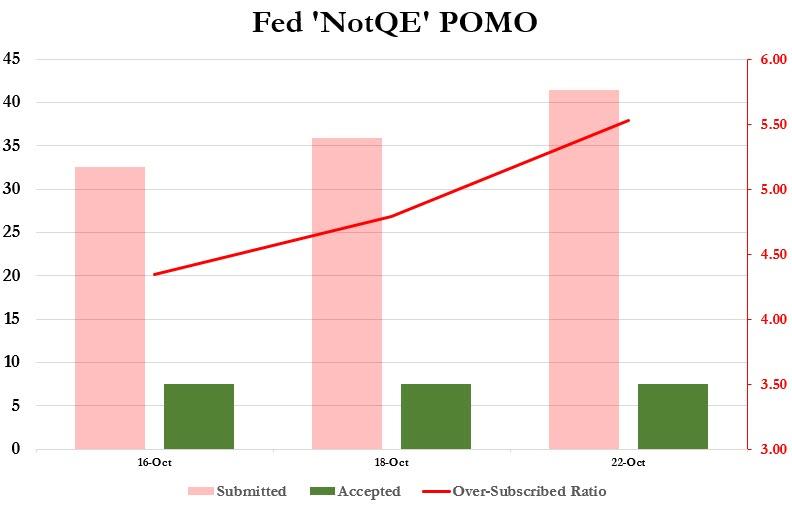

That makes me go hmmm… The

Fed announced last week that they will inject funds at a rate of $60 billion

per month (but they don’t call it QE) via the purchase of T-Bills, yet today’s

repo was oversubscribed

5.5 times. This confirms that participants are scrambling to convert their “safe”

assets into dollars as fast as possible, as ZH explains. That leaves this

question:

Why are banks still so

desperate for liquidity even though the Fed has now made clear the Fed’s

balance sheet will expand to accommodate all reserve needs, and why do they so

stubbornly refuse to approach the interbank market for their funding needs?

In short, what do they know

about the banking system that we don’t?

This monetary crunch, if it

continues, may very well get exponentially worse, at which time, there will be no

way that the sleepy equity bulls will not have a very rude awakening.

The “smart money” may have already

woken up to that fact, if this

chart from Bloomberg is any indication.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}