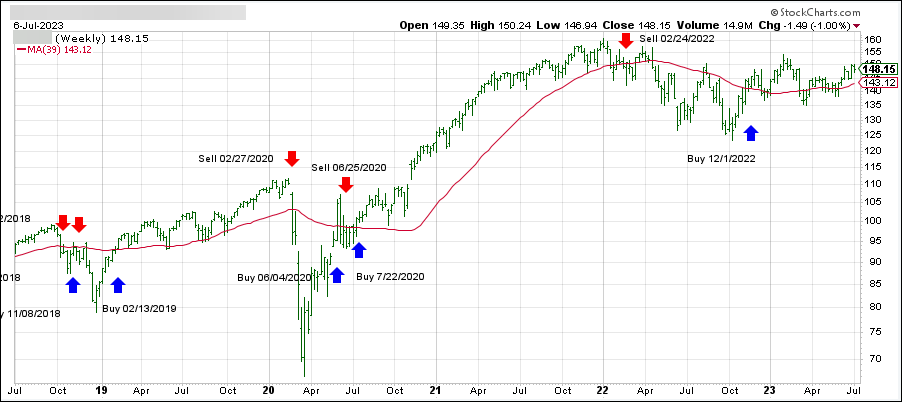

ETF Tracker StatSheet

You can view the latest version here.

JOBS, WAGES, AND REVISIONS: THE GOOD, THE BAD, AND THE UGLY

- Moving the markets

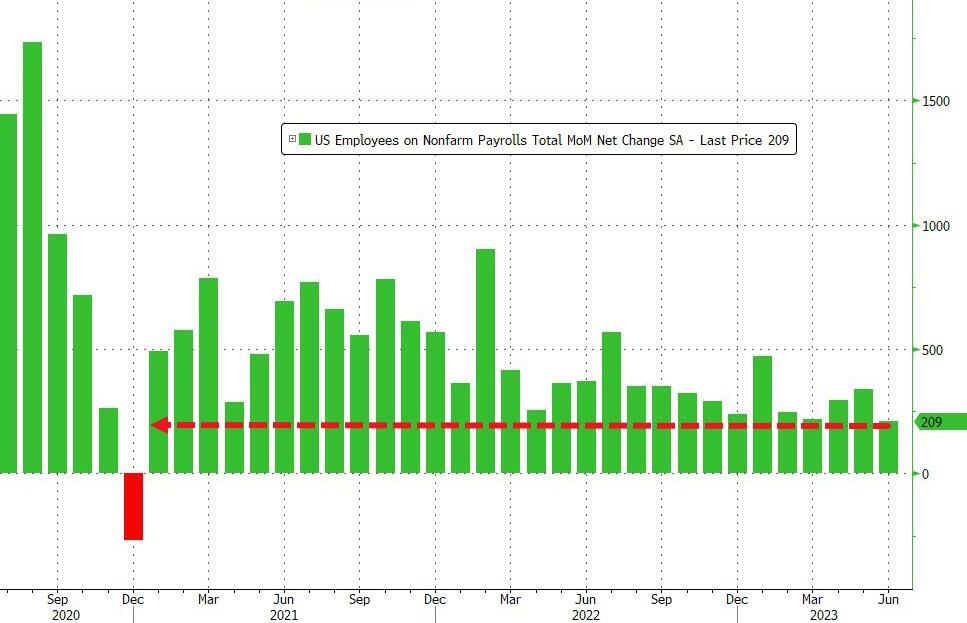

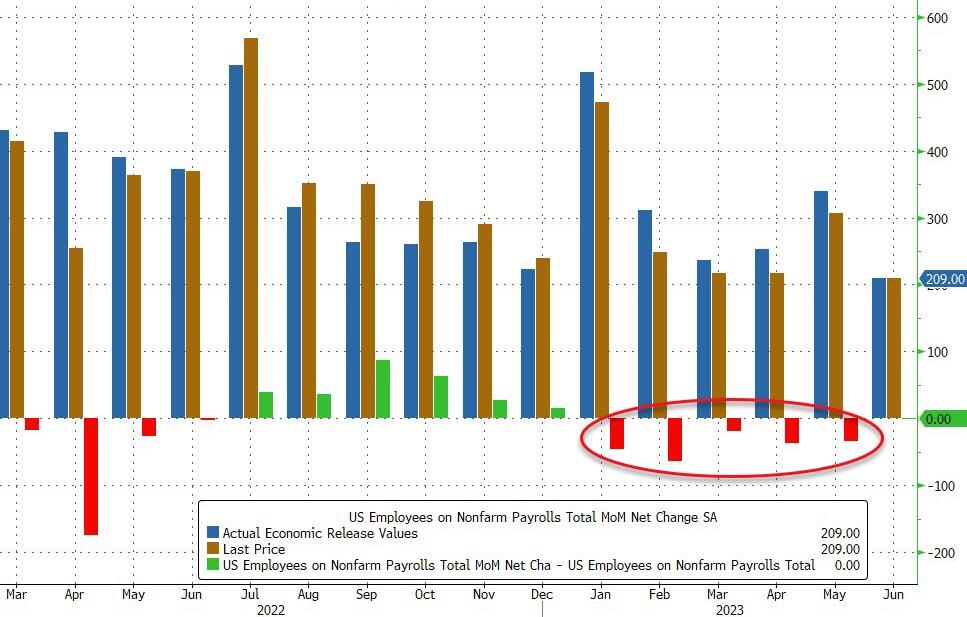

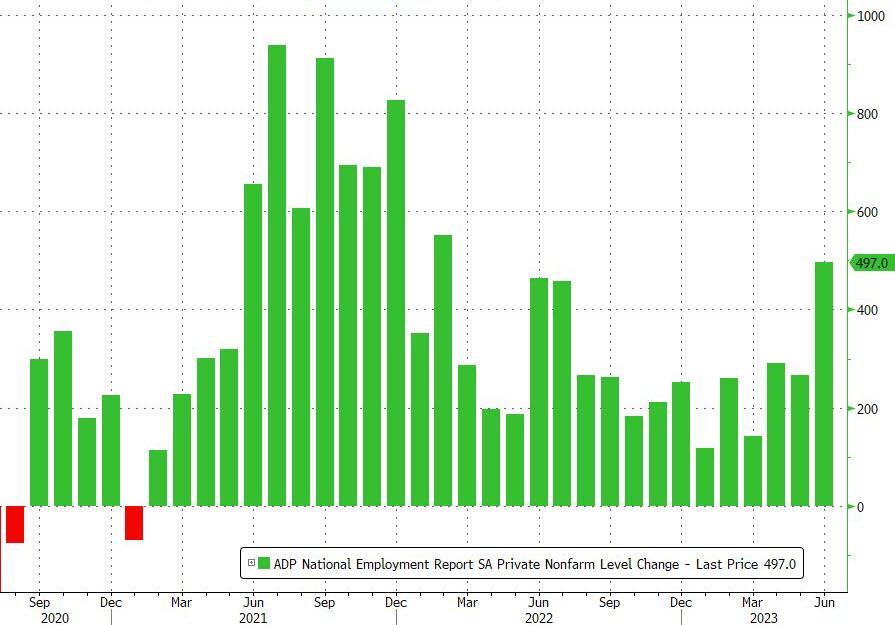

The June jobs report was a mixed bag for the markets. The economy added 209k jobs, less than the forecast of 240k, but wages grew faster than expected, raising fears of inflation and more Fed rate hikes. The unemployment rate stayed at 3.6%, the lowest since 1969.

But wait, there’s more. The previous two months’ job numbers were revised down by a whopping 110k, making 2023 the year of downward revisions. Every month this year has seen lower job growth than initially reported.

And here’s a curious fact. The government was the biggest employer in June, adding 60k jobs. That’s more than twice the average monthly increase in 2022. Maybe Uncle Sam is feeling generous, or maybe he’s preparing for something big. Wall Street didn’t know what to make of it.

The major indexes opened lower, then rallied briefly in the afternoon, only to plunge again before the closing bell. It was a roller coaster ride that left investors feeling queasy.

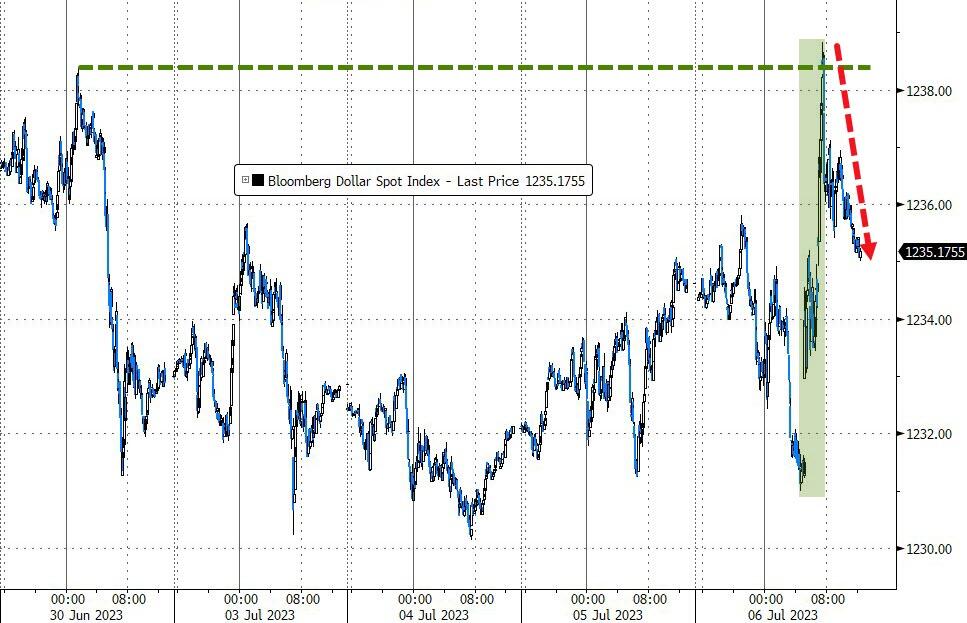

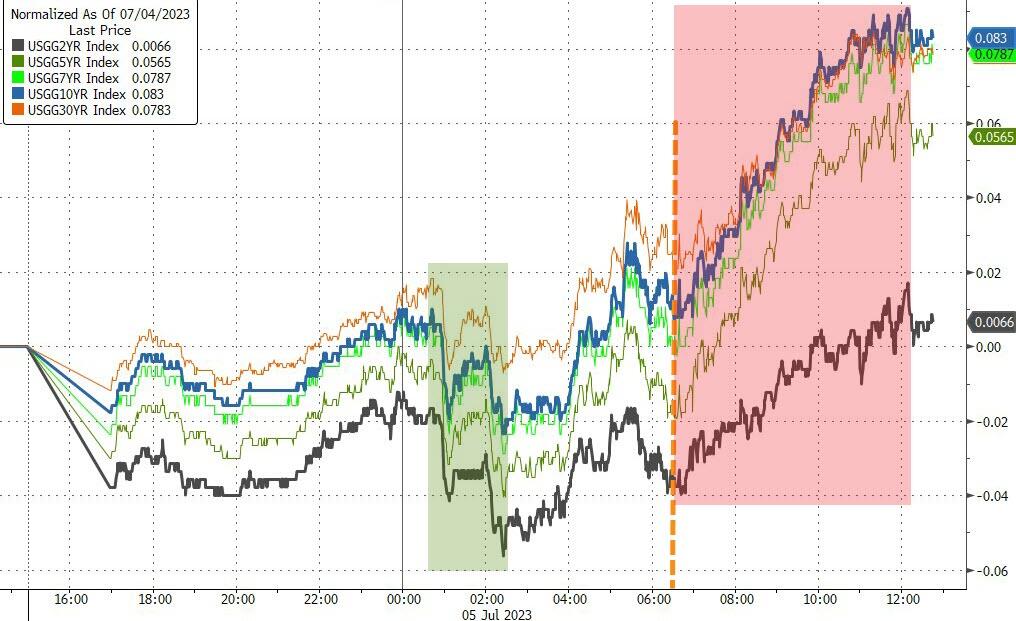

Bond yields spiked this week, but the short end of the curve fell back below 5%, the highest level since 2007. The dollar also took a dive, hitting a three-week low against other currencies. Gold had a wild day, swinging up and down before ending slightly higher.

The Fed is widely expected to raise rates by 0.25% later this month, but traders are still doubtful about two more hikes this year. Maybe they’re hoping for a miracle, or maybe they’re just in denial.

Read More

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}