ETF Tracker Newsletter For March 27, 2026

ETF Tracker StatSheet

You can view the latest version here.

DOMESTIC TTI BREAKS TREND LINE – GEOPOLITICS WEIGHS HEAVY

- Moving the market

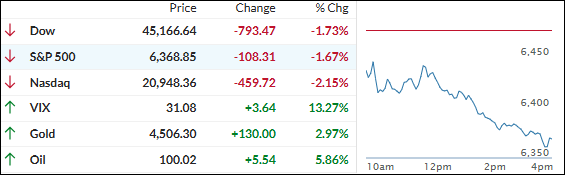

Stocks tumbled early and never really recovered, as fresh worries about the U.S.-Iran conflict and surging oil prices kept the bears firmly in control.

Brent crude traded above $110 a barrel after new incidents in the Strait of Hormuz, while President Trump’s latest comments failed to reassure traders enough to start buying.

The Nasdaq officially fell into correction territory (down more than 10% from its October record), and the Dow flirted with the same territory after dipping below it intraday. For the full week, the Nasdaq was the biggest loser (down over 3%), followed by the S&P 500.

Interestingly, small caps eked out a small gain thanks to two big short squeezes earlier in the week.

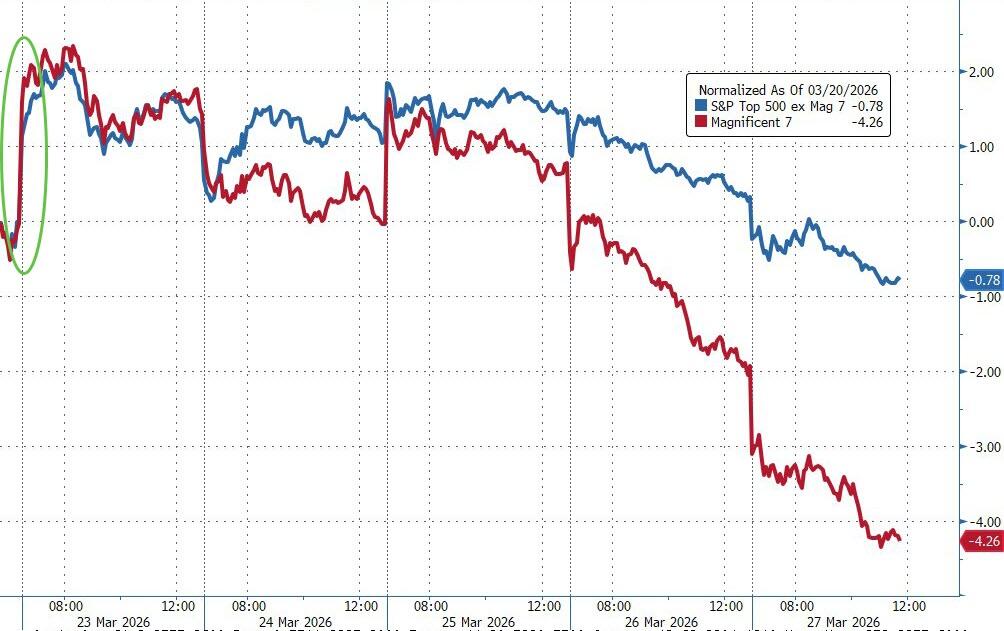

The Mag 7 continued to dramatically underperform the rest of the S&P 493. Bond yields rose across the curve (though they softened a bit today), the dollar surged for the third week in the last four, and gold finally acted like a safe haven again, pushing back above $4,500.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Silver and copper outperformed gold for the week, while Bitcoin retreated below $66K but remains roughly unchanged since the war began.

{kind=link}

{kind=link}

Today’s drop pushed our domestic TTI below its long-term trend line (more details in section 3). The international TTI held up better but is also under pressure.

At this point, it feels like traders are no longer falling for the occasional glimmer of hope being jawboned about. They’re becoming more demanding for real progress, and any absence of it could lead to even more negative market moves.

Read More